Urinary Catheters Market Summary

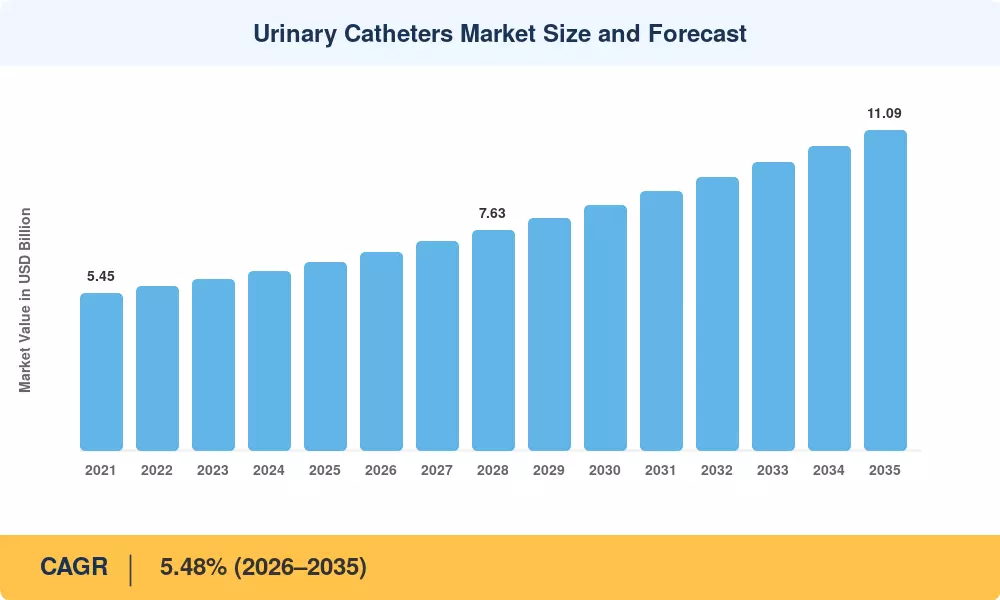

The Global Urinary Catheters Market size was valued at USD 6.50 Billion in 2025, and the market is projected to grow from USD 6.86 Billion in 2026 to USD 11.09 Billion by 2035, registering a CAGR of 5.48% during the forecast period 2026–2035. Two converging forces are propelling this trajectory: aging demographics — the WHO estimates over 1.4 billion people will be aged 60-plus by 2030 [1] — and value-based reimbursement policies that reward lower infection rates, which channel procurement budgets toward premium catheter designs [2]. The Urinary Catheters Market is entering a decade where the purchasing decision centers on clinical outcomes rather than unit price alone.

There’s a technical makeover occurring. Traditional latex devices are being gradually replaced by silicone designs that use antimicrobial coatings and, increasingly, built-in sensor modules that can continuously monitor urine flow. The U.S. Centers for Medicare & Medicaid Services’ Hospital-Acquired Condition Reduction Program penalizes facilities with higher rates of catheter-related infection, essentially forcing next-generation product use [3]. The Medical Device Regulation (MDR 2017/745) has increased the bar for conformity assessment across the EU, shortening clearance delays for legacy goods and rewarding innovation with quicker market access [4].

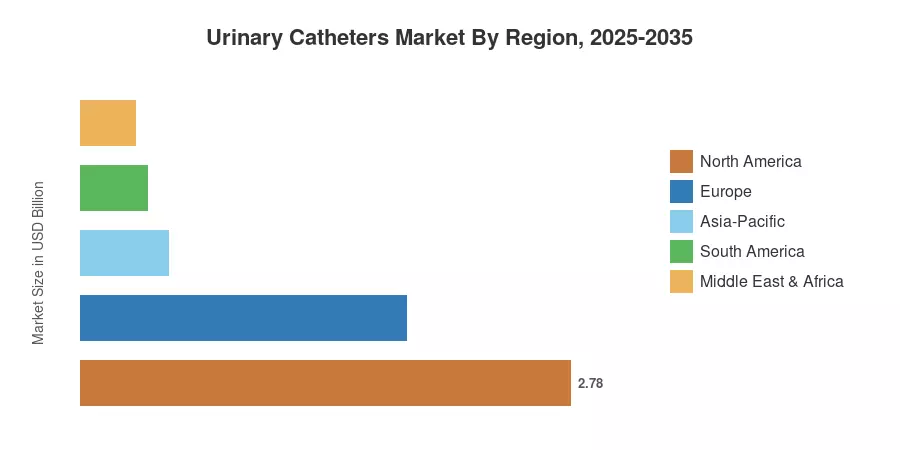

The Urinary Catheters Market in North America is dominated with a share of ~42.8% due to the well-established hospital infrastructure and extensive insurance coverage. Asia-Pacific is the fastest-growing area with a 7.62% CAGR attributable to government-led hospital-capacity expansions in China and India. Europe accounts for the second-largest proportion at 28.5% due to strict infection-control standards. In the coming decade, producers that combine improvements in material science with digital health platforms that enable remote catheter monitoring will be rewarded.

Key Report Takeaways

• By Product Type

- Indwelling (Foley) Catheters held 55.2% of the Urinary Catheters Market in 2025, reflecting their entrenched role in acute-care settings.

- Intermittent Catheters are forecast to post the fastest CAGR of 6.18% through 2035, supported by self-catheterization training programs and favorable reimbursement.

• By Application

- Urinary Incontinence represented 44.9% of the Urinary Catheters Market in 2025, making it the single largest clinical indication.

- Home-Care Settings are projected to expand at a 7.27% CAGR to 2035, outpacing hospital procurement growth as payer models shift toward outpatient management.

• By Geography

- North America generated 42.8% of 2025 revenue, led by the United States' reimbursement depth and high surgical volumes.

- Asia-Pacific is expected to record the strongest growth at 7.62% CAGR, fueled by India's Ayushman Bharat expansion and China's county-level hospital build-out.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) projections are based on primary interviews with procurement directors of more than 120 hospital systems, published clinical registries, customs trade-flow databases and annual reports of 15 publicly listed catheter manufacturers. Historical numbers (2021–2024) represent actual shipment revenues adjusted for channel markups; future values (2026–2035) are derived from a constant-growth model validated against demographic forecasts and analysis of reimbursement trends.