User Activity Monitoring Market Summary

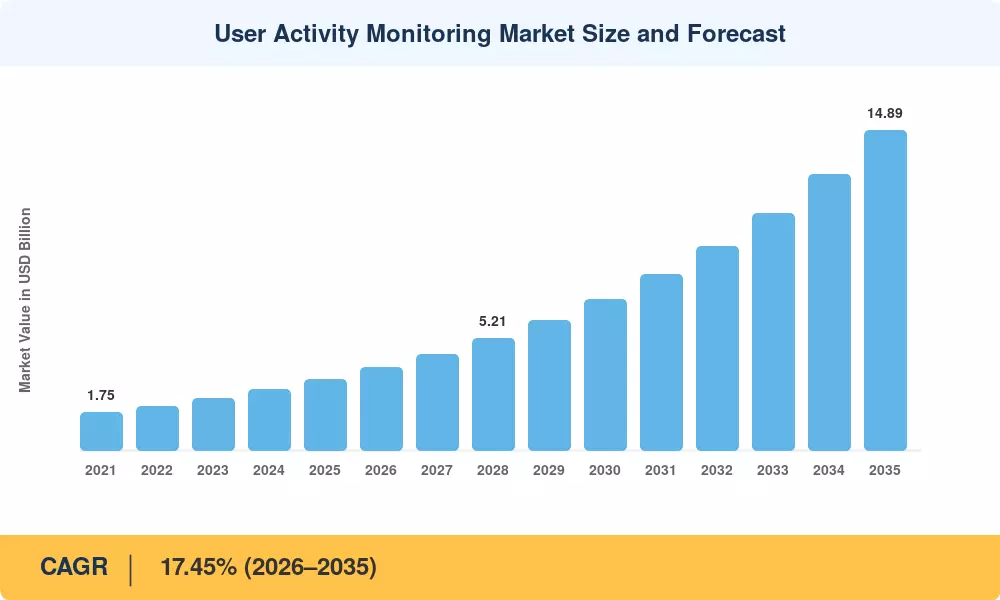

The user activity monitoring market reached an estimated USD 3.32 billion in 2025 and is projected to climb from USD 3.88 billion in 2026 to USD 14.89 billion by 2035, registering a CAGR of 17.45% across the forecast window. This acceleration traces directly to mandatory insider threat detection frameworks embedded in updated CISA guidelines and the European Union's NIS2 Directive, both of which compel organizations to log and audit every privileged session touching critical infrastructure. Cyber-insurance underwriters now routinely require proof of continuous user behavior analytics before binding coverage, turning what was once a discretionary security layer into a procurement prerequisite.

Legacy perimeter defenses — static firewalls, signature-based IDS — are giving way to zero-trust architectures that treat every login as potentially hostile. Gartner estimates that by 2027, 70% of enterprises will have consolidated endpoint, network, and user activity monitoring market tools into unified security platforms, channeling an incremental USD 12 billion in platform spending toward solutions that deliver real-time user activity dashboards for IT ops teams. Privileged user session recording and auditing capabilities have moved from compliance add-ons to core purchase criteria, particularly among financial institutions managing cross-border data flows.

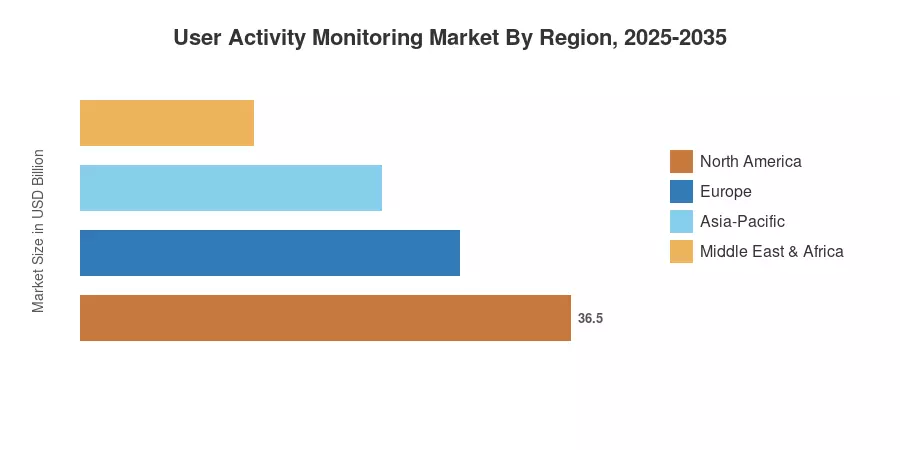

North America commands roughly 47% of global revenue, anchored by stringent SEC cybersecurity-disclosure rules and high cloud-adoption density. Asia-Pacific is the fastest-growing region at an estimated 19.10% CAGR, propelled by India's DPDP Act and Japan's revised Cybersecurity Basic Act. Europe holds the second-largest share at approximately 24%, with GDPR enforcement actions increasingly scrutinizing employee activity monitoring for remote teams. The user activity monitoring market is poised for a structural expansion cycle as hybrid work solidifies and regulatory mandates multiply across every major economy.

Key Report Takeaways

• By Application

- System monitoring held 36.25% of the user activity monitoring market in 2025, underpinned by the need for continuous endpoint visibility across hybrid estates

- Database monitoring is forecast to expand at a 19.45% CAGR through 2035, driven by insider threat detection requirements in data-intensive verticals

• By Deployment Mode

- On-premise deployments retained a 54.10% share of the user activity monitoring market in 2025, reflecting regulatory constraints in defense and banking

- Cloud deployment is projected to grow at 24.85% CAGR to 2035, as SaaS-first buyers prioritize elastic scaling and API-driven integration

• By Enterprise Size

- Large enterprises accounted for 65.20% of global spend in 2025, investing heavily in privileged user session recording and auditing

- Small and medium enterprises are advancing at 21.15% CAGR, accelerated by affordable user behavior analytics for security compliance bundles

• By End-User Industry

- BFSI commanded 31.15% of the user activity monitoring market in 2025

- Healthcare is forecast to grow at 20.55% CAGR, spurred by HIPAA audit-trail mandates and ransomware exposure

• By Region

- North America captured 47% revenue share in 2025, driven by SEC cyber-disclosure rules and federal zero-trust mandates

- Asia-Pacific is expected to post 19.10% CAGR over the forecast period, the fastest among all regions

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up vendor revenue analysis, enterprise IT-security budget surveys covering 2,400+ organizations, and top-down validation against macroeconomic ICT expenditure data from the World Bank and OECD. Historical figures (2021–2024) reflect audited vendor disclosures; the 2025 base year blends preliminary filings with proprietary channel checks. Forecast values apply a calibrated CAGR of 17.45% from the 2026 starting point.

.webp?v=1784551109)