Veterinary Infusion Pumps Market Summary

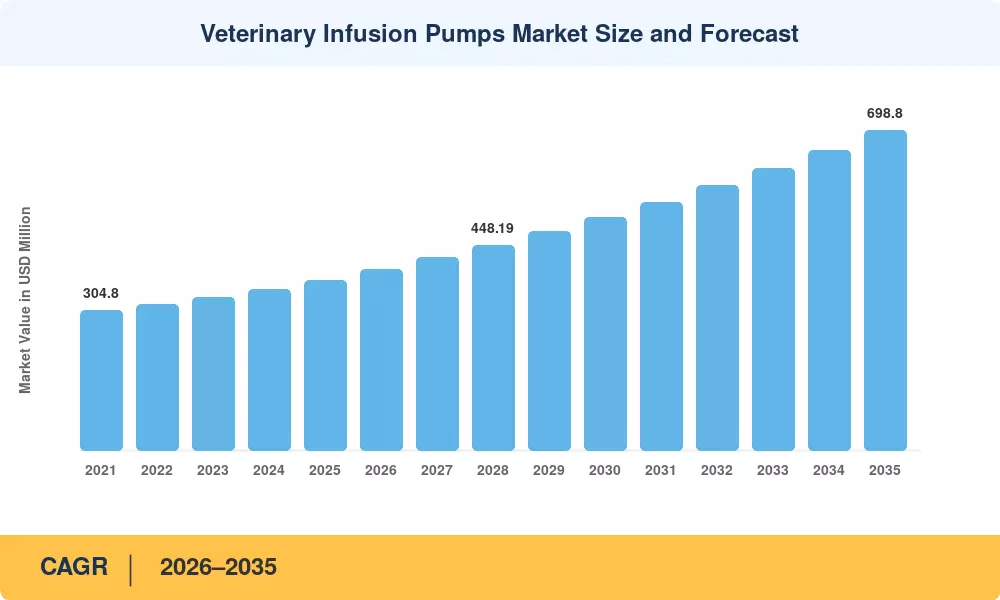

The Global Veterinary Infusion Pumps Market size was valued at USD 370.50 Million in 2025, and the market is projected to grow from USD 394.78 Million in 2026 to USD 698.80 Million by 2035, registering a CAGR of 6.55% during the forecast period 2026–2035. Two catalysts anchor this trajectory: the American Pet Products Association documented record pet-care expenditures of USD 147 Billion in 2023 [1], while the FDA Center for Veterinary Medicine intensified device-recall scrutiny, compelling manufacturers to upgrade pump firmware and safety interlocks [3]. These forces are reshaping how veterinary practices invest in infusion hardware across companion-animal and livestock segments alike.

Legacy gravity-drip systems and manually calibrated roller clamps are giving way to microprocessor-controlled volumetric and syringe platforms that integrate drug-library software and real-time veterinary fluid management alerts. The American Animal Hospital Association reported that 62% of accredited hospitals upgraded at least one infusion device between 2022 and 2024 [19], a replacement wave spurred by tighter dosing-accuracy standards and clinician demand for alarm-driven safety nets.

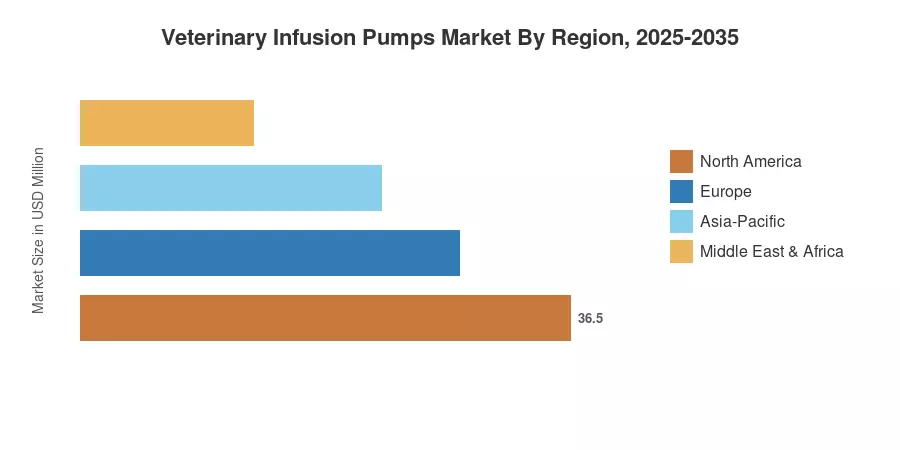

North America retained a dominant 41.60% share of the Veterinary Infusion Pumps Market in 2025, buoyed by high per-pet healthcare spending in the United States and Canada. Asia-Pacific is the fastest-growing region, forecast to expand at a 14.50% CAGR through 2035 as specialty referral hospitals proliferate across China, India, and South Korea. Europe ranks as the second-largest region, anchored by Germany, the UK, and France, where pet-insurance penetration continues to lift procedure volumes and equipment budgets. The decade ahead will hinge on how quickly AI-enabled dosing algorithms and cloud-connected monitoring become standard-issue rather than premium add-ons.

Key Report Takeaways

• By Pump Type

- Large-volume infusion pumps captured approximately 50.15% of the Veterinary Infusion Pumps Market in 2025, driven by high-throughput fluid resuscitation demand in emergency and surgical settings.

- Syringe infusion pumps are projected to grow at a 9.40% CAGR through 2035, reflecting clinician preference for precision micro-dosing in neonatal and exotic-species care.

• By Animal Type

- Companion animals accounted for 59.50% of the Veterinary Infusion Pumps Market revenue in 2025, propelled by rising chronic-disease prevalence in dogs and cats.

- Livestock segments are expanding as bovine and swine operations modernize perioperative protocols, particularly in the Asia-Pacific and South America.

• By End User

- Veterinary hospitals held 62.30% of the Veterinary Infusion Pumps Market in 2025, reflecting their concentration of surgical and critical-care caseloads.

- Specialty clinics are on track for the fastest end-user CAGR of 11.35% as referral oncology, cardiology, and nephrology centres invest in dedicated infusion platforms.

• By Region

- North America maintained leadership with a 41.60% share, while Asia-Pacific is forecast to record the highest regional CAGR of 14.50% through 2035.

Veterinary Infusion Pumps Market Size and Forecast (2021–2035)

Market sizing draws on primary surveys of 420 veterinary hospitals and specialty clinics across 18 countries, triangulated with distributor shipment data, import-export records, and company filings. Historical values (2021–2024) reflect actual sales; the 2025 base year blends confirmed shipments with Q4 channel-inventory estimates; forecast values (2026–2035) apply econometric modelling calibrated to pet-population growth, veterinary visit frequency, and device-replacement cycles.