Wearable Sensors Market Summary

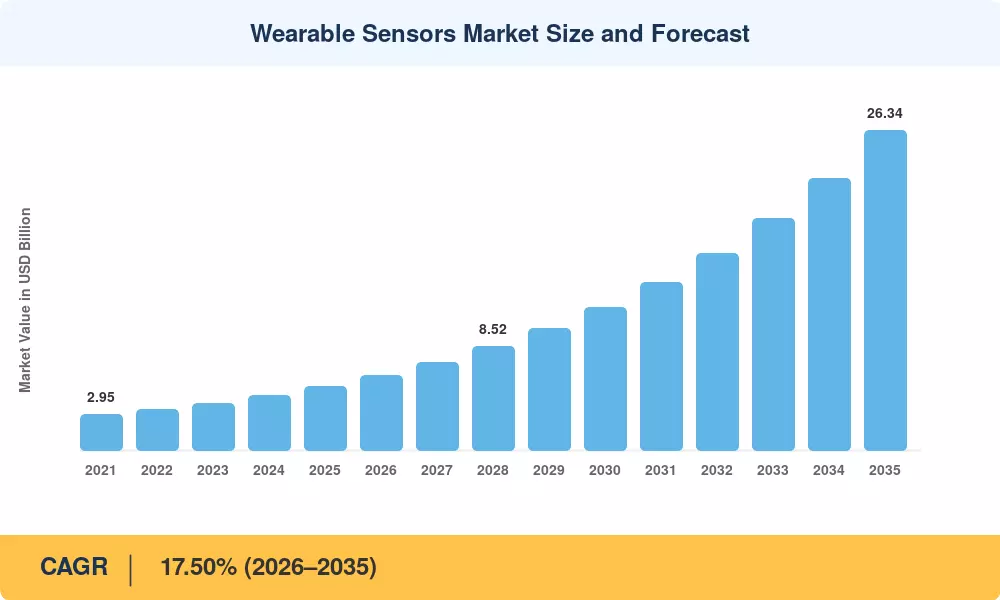

The Global Wearable Sensors Market size was valued at USD 5.25 Billion in 2025, and the market is projected to grow from USD 6.17 Billion in 2026 to USD 26.34 Billion by 2035, registering a CAGR of 17.50% during the forecast period 2026–2035. This trajectory reflects accelerating adoption of physiological monitoring across healthcare, fitness, and industrial safety verticals. The U.S. FDA's expanded De Novo pathway for software-as-a-medical-device cleared 47 wearable-class submissions in 2024 alone, while CMS reimbursement codes for remote patient monitoring now cover over 130 million Medicare beneficiaries [1]. These regulatory tailwinds have unlocked billions in payer-funded demand that did not exist five years ago.

A structural technology shift is redefining the Wearable Sensors Market. Legacy clip-on pulse oximeters and bulky Holter monitors are giving way to ultra-thin, skin-conformal sensor arrays powered by advances in flexible substrates and system-on-chip integration. STMicroelectronics reported that its latest MEMS inertial modules consume 40% less power than 2022 equivalents while embedding on-device machine-learning inference cores [2]. Semiconductor R&D investment in wearable-grade sensors exceeded USD 3.8 billion globally in 2024, with over 60% directed at sub-milliwatt analog front-ends and multi-modal sensor fusion [3].

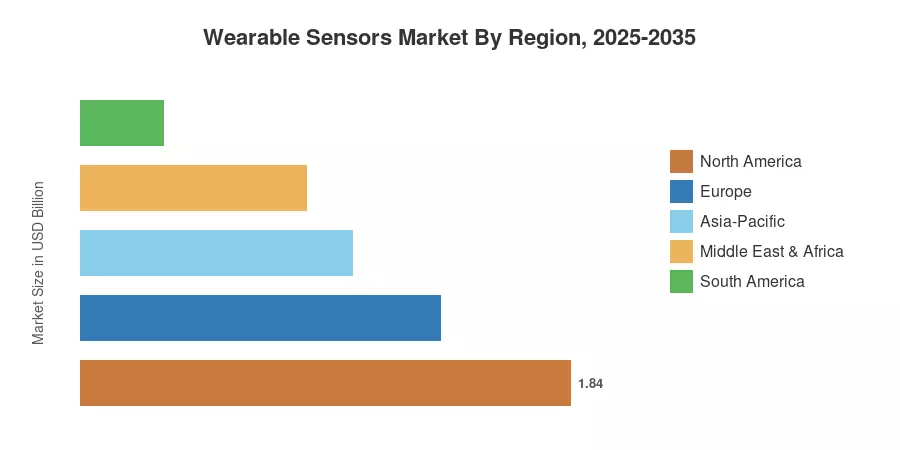

North America leads the Wearable Sensors Market with an estimated 35.1% revenue share in 2025, driven by robust insurance reimbursement frameworks and a dense digital-health startup ecosystem. Asia-Pacific is the fastest-growing region, anticipated to expand at a 19.40% CAGR through 2035, propelled by government-backed smart-city health initiatives in China, India, and South Korea. Europe holds the second-largest share at roughly 25.8%, anchored by the EU Medical Device Regulation (MDR 2017/745) and aging-population demographics. As 5G infrastructure matures globally, the Wearable Sensors Market is positioned for sustained double-digit growth well into the next decade.

Key Report Takeaways

• By Sensor Type

- Motion sensors commanded 36.0% of the Wearable Sensors Market share in 2025, underpinned by universal integration across smartwatches, fitness bands, and industrial wearables.

- Biosensors represent the fastest-expanding category, projected to grow at a 20.20% CAGR through 2035, fueled by clinical-grade biomarker detection and chronic disease management applications.

• By Application

- Health and wellness accounted for 48.8% of Wearable Sensors Market revenue in 2025, reflecting consumer demand for preventive care and real-time biometric dashboards.

- Remote patient monitoring is forecast to register a 20.80% CAGR to 2035, as telehealth reimbursement policies expand globally.

• By Region

- North America maintained the dominant position in the Wearable Sensors Market with 35.1% share in 2025.

- Asia-Pacific is projected to deliver the highest CAGR of 19.40% to 2035, led by China and India.

Wearable Sensors Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates bottom-up sensor shipment volumes from leading semiconductor fabs, top-down healthcare spending allocations, and enterprise procurement datasets. Historical figures draw on verified company filings and customs trade data, while forecast projections apply demand-curve modeling calibrated to regulatory release schedules and consumer adoption S-curves.