Windows and Doors Market Summary

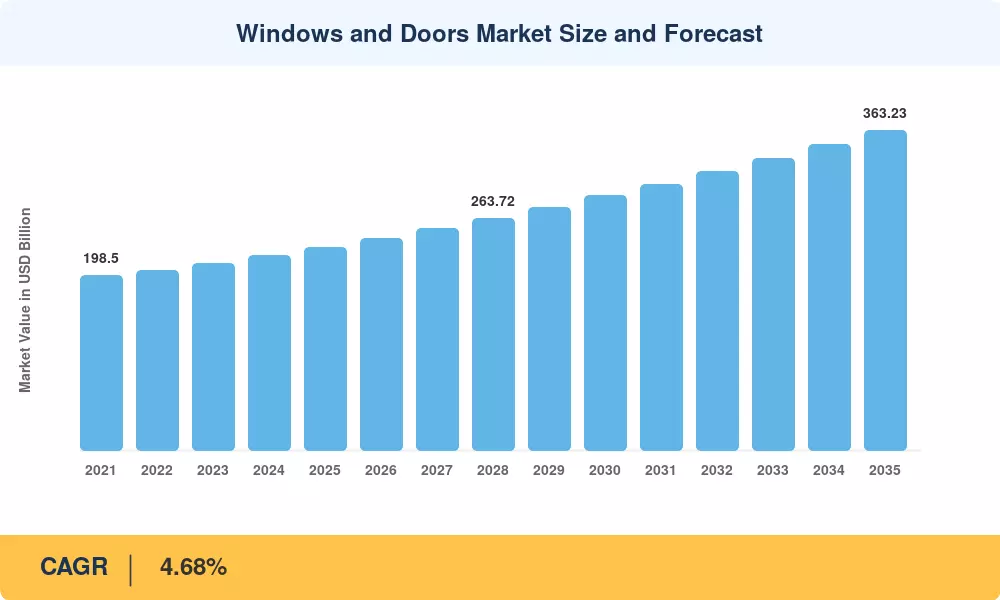

The Windows and Doors Market was valued at USD 229.90 Billion in 2025 and is projected to grow from USD 240.66 Billion in 2026 to USD 363.23 Billion by 2035, registering a CAGR of 4.68% during the forecast period (2026–2035). Tighter building-envelope performance codes and sustained renovation spending across mature economies are the two principal catalysts behind this expansion. The U.S. ENERGY STAR Version 7.0 standard, which tightens U-factor thresholds toward 0.22 in northern climate zones, is already redirecting specification activity toward triple-pane glazing and thermally broken frames [1]. In the EU, the revised Energy Performance of Buildings Directive (EPBD) targets zero-emission new construction by 2030, compelling developers to specify higher-performance fenestration from the design stage [2].

A technology shift is reshaping the Windows and Doors Market from the supply side. Traditional single-pane and basic double-pane units are giving way to vacuum-insulated glazing, electrochromic smart glass, and composite framing systems that cut thermal bridging by up to 60% [3]. Automated fabrication lines—some capable of producing 1,200 insulated glass units per shift—are compressing lead times and enabling mass customization, a trend particularly visible in European and East Asian manufacturing hubs [4].

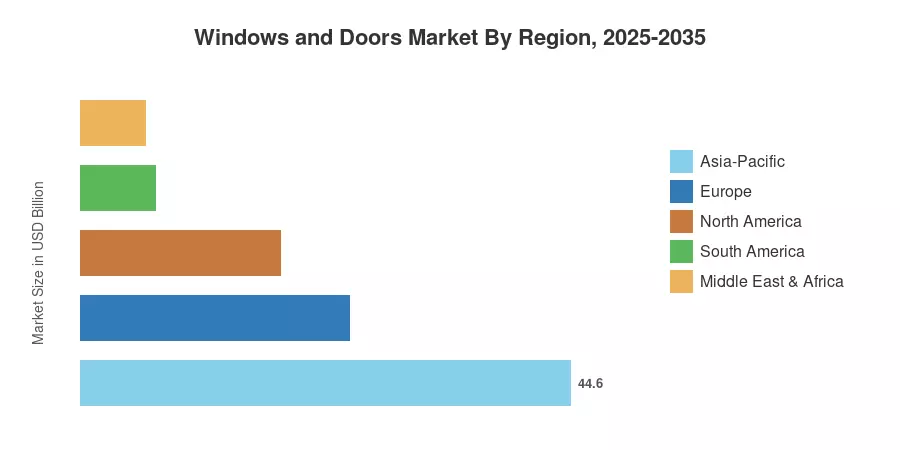

Asia-Pacific commands roughly 44.6% of the Windows and Doors Market, underpinned by large-scale residential construction in China and India. The Middle East & Africa region is the fastest-growing at a projected CAGR of 7.55%, driven by mega-project pipelines such as Saudi Arabia's NEOM and Egypt's New Administrative Capital [5]. Europe holds the second-largest share at approximately 24.5%, where deep-energy retrofit mandates continue to fuel replacement demand. As urbanization accelerates across developing economies and retrofit cycles intensify in mature ones, the Windows and Doors Market is positioned for sustained mid-single-digit growth through 2035.

Key Report Takeaways

• By Product Type

- Doors captured the dominant revenue position in 2025, holding an estimated 62.0% share of the Windows and Doors Market.

- Windows are forecast to register a CAGR of 7.90% through 2035, driven by triple-pane and vacuum-glazing adoption in colder climate zones.

• By Material & Application

- Metal framing (aluminum and steel) accounted for roughly 49.3% of the Windows and Doors Market in 2025, reflecting commercial-project specification dominance.

- Folding-mechanism products are projected to achieve a CAGR of 10.15%, the fastest among all application types.

• By End User

- Residential end users represented approximately 62.5% of global demand in 2025.

• By Region

- Asia-Pacific contributed the largest regional revenue share at 44.6%, while the Middle East & Africa is anticipated to grow at a 7.55% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on primary interviews with fenestration manufacturers, trade-body data from AAMA and Eurowindoor, building-permit databases, and proprietary demand models calibrated against national construction output indices. Historical figures reflect actual shipment revenues; forecast values apply the calibrated CAGR with adjustments for identified spike and contraction periods.