Zika Virus Testing Market Summary

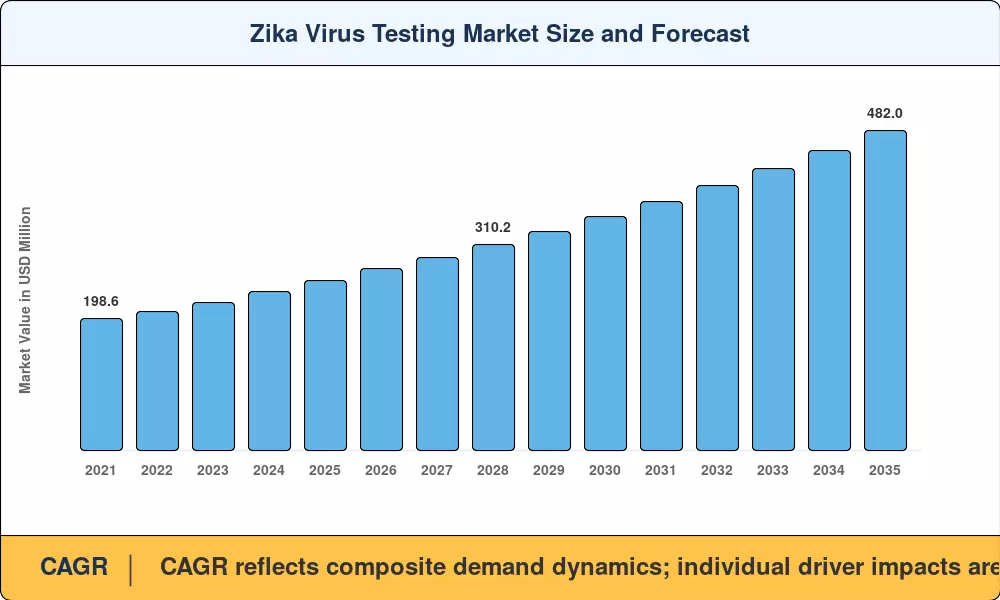

The Global Zika Virus Testing Market size was valued at USD 255.50 Million in 2025, and the market is projected to grow from USD 273.50 Million in 2026 to USD 482.00 Million by 2035, registering a CAGR of 6.50% during the forecast period 2026–2035. Two structural catalysts anchor this expansion: the WHO's updated arboviral surveillance guidelines mandating nucleic-acid confirmation in travel-associated cases [1], and sustained CDC appropriations exceeding USD 45 million annually for mosquito-borne diagnostic infrastructure [6]. Climate-driven vector migration into previously temperate zones has transformed Zika testing from an episodic outbreak expense into a standing budget line for public-health systems across four continents.

Multiplex molecular platforms that can distinguish between dengue, chikungunya, and Zika in a single cartridge are taking the place of single-analyte immunoassays in laboratories. This convergence reduces turnaround time from 48 hours to less than 90 minutes and reduces the cost of each test reagent by an estimated 30–35% [2]. In addition to reducing development periods from 18 months to about 10 months for CE-IVD-marked products, artificial intelligence-assisted assay design is simultaneously tackling the persistent cross-reactivity issue that besets first-generation serological kits [3].

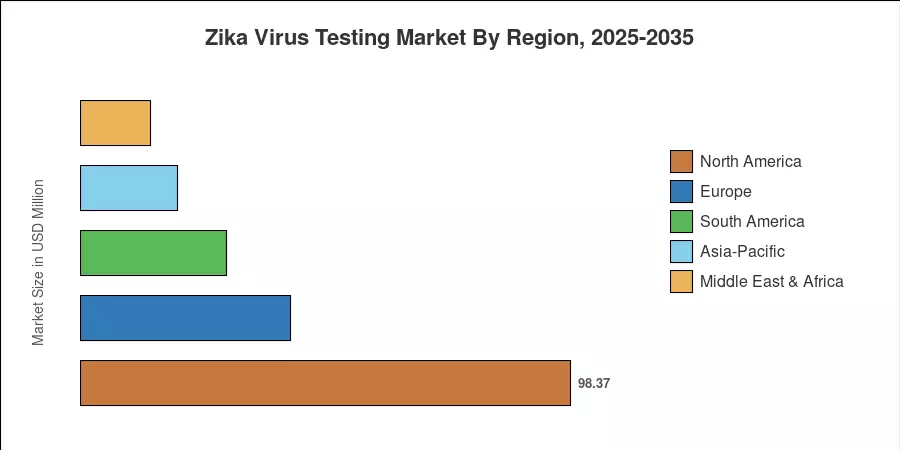

Due to mandates for blood bank screening and entrenched monitoring procurement from state public health laboratories, North America holds the highest share of the Zika virus testing market, accounting for 38.5% of 2025 revenue. The fastest-growing region is Asia-Pacific, which is expanding at a 7.60% CAGR as countries like the Philippines, Indonesia, and India expand their vector-borne illness laboratory networks [4]. With a 16.5% stake, Europe is in second place thanks to returning-traveler screening initiatives implemented throughout the Schengen region. Manufacturers who combine regulatory flexibility with decentralized testing formats appropriate for resource-constrained field circumstances will benefit in the upcoming ten years.

Key Report Takeaways

• By Test Type

- Molecular tests captured 62.5% of the 2025 Zika Virus Testing Market revenue, reflecting the shift toward nucleic-acid confirmation as the diagnostic gold standard.

- Point-of-care molecular assays are on track for a 9.10% CAGR through 2035, the fastest expansion across all test-type segments.

• By Sample Type

- Blood and serum specimens held a dominant 76.0% share of the Zika Virus Testing Market in 2025.

- Saliva-based protocols are advancing at an 8.55% CAGR, propelled by non-invasive self-collection acceptance.

• By Region

- North America accounted for 38.5% of global spending, underpinned by FDA-cleared assay portfolios and automated high-throughput platforms.

- Asia-Pacific is projected to grow at 7.60% CAGR through 2035, fueled by upgraded national reference laboratories and rising outbreak vulnerability.

- South America contributed 11.5% of the 2025 value, sustained by PAHO-coordinated procurement channels across Brazil and Argentina.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from published WHO case-notification data, national tender records, and manufacturer revenue disclosures. Forecast projections apply a bottom-up methodology calibrated to installed laboratory capacity, regulatory pipeline milestones, and climate-adjusted vector-risk models [1][5].

.webp?v=1782120130)