Author

Aarti Dhapte

二维码支付市场研究报告,按应用(零售、交通、食品和饮料、医疗保健、娱乐)、按最终用户(消费者、商家、服务提供商)、按类型(静态二维码、动态二维码、加密二维码)、按技术(移动钱包、银行应用、电子商务平台)以及按地区(北美、欧洲、南美、亚太、中东和非洲)- 行业规模、份额及2035年预测。

根据MRFR分析,二维码支付市场规模在2024年估计为168.2亿美元。二维码支付行业预计将从2025年的190.4亿美元增长到2035年的656.7亿美元,预计在2025年至2035年的预测期内,年均增长率(CAGR)为13.18。

二维码支付市场正经历强劲增长,受到技术进步和消费者偏好变化的推动。

| 2024 Market Size | 168.2亿美元 |

| 2035 Market Size | 65.67(美元十亿) |

| CAGR (2025 - 2035) | 13.18% |

支付宝(中国),微信支付(中国),PayPal(美国),Square(美国),Google Pay(美国),Apple Pay(美国),Samsung Pay(韩国),Paytm(印度),Zelle(美国)

Our Impact

Enabled $4.3B Revenue Impact for Fortune 500 and Leading Multinationals

Partnering with 2000+ Global Organizations Each Year

30K+ Citations by Top-Tier Firms in the Industry

二维码支付市场目前正经历显著的转型,这一转型受到各个行业对数字支付解决方案日益采用的推动。这一变化似乎受到对无接触交易日益增长的需求的影响,这为消费者提供了便利和速度。随着企业寻求提升客户体验,二维码已成为促进无缝支付的实用工具。此外,二维码与移动应用程序和电子商务平台的整合表明,用户的更广泛接受潜力,从而扩大了市场的覆盖范围。此外,二维码支付市场似乎也受益于技术的进步,特别是在移动设备和互联网连接方面。增强的安全功能和用户友好的界面可能会鼓励更多个人参与二维码支付。随着市场的发展,它也可能会见证金融机构与技术提供商之间的更多合作,促进创新并改善服务交付。总体而言,二维码支付市场正处于增长的有利位置,反映出向更高效和可及的支付方式的转变。

消费者对无接触支付方式的倾向日益增强,而二维码有效地促进了这一点。这一趋势表明消费者行为的转变,个人在交易中越来越重视便利性和速度。

二维码支付市场正在见证一个趋势,即企业将二维码整合到他们的电子商务平台中。这一整合提升了购物体验,使客户能够通过移动设备快速安全地进行支付。

随着安全问题的持续上升,二维码支付市场正在通过引入先进的安全措施进行适应。这些增强措施旨在建立消费者信任,鼓励在各种交易中更广泛地采用二维码支付。

支付系统的技术进步正在重塑二维码支付市场。区块链技术和增强的加密方法等创新正在提高二维码交易的安全性和效率。截至2025年10月,人工智能在支付处理中的集成也在获得关注,使个性化客户体验和欺诈检测成为可能。这些进步不仅增强了二维码支付的可靠性,还增强了消费者对数字交易的信心。此外,移动钱包和支付应用程序的持续发展正在促进二维码在日常交易中的无缝集成。随着技术的不断进步,二维码支付市场可能会见证持续增长,推动这一增长的是对安全和高效支付解决方案的需求。

智能手机的普及是二维码支付市场的一个关键驱动力。到2025年10月,预计发达地区超过80%的人口拥有智能手机,这促进了二维码支付系统的采用。这一趋势在年轻人群体中尤为明显,他们更倾向于使用移动支付解决方案。扫描二维码进行交易的便利性与当今消费者的快节奏生活方式相契合。此外,智能手机中先进的摄像头技术的整合提升了用户体验,使二维码支付更加便捷。随着智能手机普及率的持续上升,二维码支付市场可能会经历显著增长,推动这一增长的是越来越多对移动技术感到舒适的用户。

政府旨在促进数字支付的举措在二维码支付市场中发挥着至关重要的作用。各国已实施政策以鼓励无现金交易,认识到数字支付对经济增长和效率的好处。截至2025年10月,多个政府已启动活动,以教育消费者关于二维码支付的优势,包括便利性和安全性。这些举措通常包括与金融机构和技术提供商的合作,以增强基础设施和可及性。政府机构的支持不仅促进了消费者信任,还激励企业采用二维码支付系统。因此,二维码支付市场可能会蓬勃发展,受益于有利的监管环境和消费者意识的提高。

零售和电子商务领域的快速扩张显著影响了二维码支付市场。近年来,零售格局发生了变化,许多企业采用数字支付解决方案以提升客户体验。截至2025年10月,电子商务销售激增,估计年增长率超过15%。这种向在线购物的转变迫使实施高效的支付方式,包括二维码。零售商越来越多地利用二维码进行促销、忠诚度计划和无缝结账流程。这一趋势不仅简化了交易,还鼓励了消费者的参与。因此,随着越来越多的零售商和电子商务平台将二维码支付解决方案整合到其运营中,二维码支付市场有望实现增长。

对无接触支付解决方案的日益增长的需求是二维码支付市场的重要驱动力。消费者越来越倾向于选择能够减少身体接触的支付方式,这与当代对卫生和便利的偏好相一致。截至2025年10月,调查显示近70%的消费者更喜欢无接触支付而非传统支付方式。二维码提供了独特的优势,使用户能够在无需与支付终端进行物理互动的情况下完成交易。这一趋势在食品服务和零售等行业尤为明显,这些行业对速度和效率的要求至关重要。随着企业适应以满足消费者期望,二维码支付市场预计将扩大,推动这一市场增长的是无接触支付技术的日益普及。

二维码支付市场在各个应用领域竞争激烈,零售占据了最大的市场份额。零售行业对二维码支付的采用受到易用性和无接触交易日益增长的趋势的推动。紧随其后,食品和饮料领域由于移动食品订购和配送服务的增加而迅速获得关注,这些服务优化了客户体验。

零售:主导与食品和饮料:新兴

在二维码支付市场中,零售是主导的应用细分市场,主要特点是广泛的采用和与销售点系统的集成。零售商利用二维码来简化交易、提高客户参与度和增强运营效率。另一方面,食品和饮料细分市场正在迅速崛起,受到消费者对便利和无接触订单偏好的变化的推动。餐厅和咖啡馆越来越多地将二维码纳入菜单和支付系统,从而实现无缝的用餐体验,同时减少等待时间。

在二维码支付市场中,终端使用细分市场的市场份额分布具有重要意义。消费者细分市场占据最大份额,主要是由于个人对移动支付解决方案的日益采用。消费者更喜欢二维码支付在日常购物中的便利性,这使得其变得突出。相比之下,尽管商户细分市场的份额较消费者小,但由于企业越来越多地采用二维码技术以满足科技敏感型客户的需求,它被认为是快速增长的。

最终用途:消费者(主导)与商家(新兴)

消费者细分市场的特点是其在寻求便捷支付方式的日常用户中广泛采用,使得二维码支付成为零售到餐饮等各种交易的首选选项。相比之下,尽管商家细分市场仍在发展中,但由于支付流程的数字化进程和降低交易费用的好处,显示出强大的潜力。商家们越来越多地利用二维码来简化支付机制并提升客户体验,从而在竞争激烈的市场中占据一席之地。随着越来越多的商家整合二维码支付,他们的角色将继续演变,可能使他们在未来成为主导细分市场。

二维码支付市场在“类型”类别中显示出明显的细分。动态二维码占据了最大的市场份额,主要由于其多功能性和提供实时更新的能力,这吸引了广泛的企业。静态二维码虽然有价值,但在市场分布上落后,因为它们提供的互动性和适应性有限,使其在不断变化的支付需求中不太受欢迎。

静态二维码(主流)与加密二维码(新兴)

在二维码支付市场中,静态二维码因其简单易用而常被视为主导。它们主要被小型企业用于固定支付,这使得它们在各种交易中成为常见选择。相反,加密二维码作为一个关键参与者正在崛起,因其附加的安全特性而获得关注,这在当今数据隐私问题突出的数字环境中愈发受到重视。随着消费者和企业对更安全支付选项的需求增加,加密二维码预计将见证显著增长,从而在市场偏好中创造动态转变。

在二维码支付市场中,移动钱包目前占据最大的市场份额,这得益于消费者对便捷和无接触支付解决方案的偏好。紧随其后的是银行应用程序,随着金融机构增强其数字产品并推广二维码交易,银行应用程序也在逐渐获得关注。电子商务平台在这一领域也发挥着关键作用,通过二维码集成支持无缝的购物体验。目前,移动钱包主导市场,而银行应用程序和电子商务平台正吸引越来越多用户的关注。

技术:移动钱包(主导)与银行应用(新兴)

移动钱包已成为二维码支付市场的主导力量,为用户提供了一种快速安全的方式,通过智能手机进行交易。它们的广泛采用得益于创新功能,如忠诚度计划、易用性以及与各种支付方式的整合。相比之下,银行应用程序由于在优先考虑安全性和与银行账户直接整合的消费者中迅速普及,正逐渐成为一个重要参与者。这一向银行应用程序的转变反映了消费者对数字银行日益增长的信任,以及对更可控支付方式的渴望,展示了支付技术不断演变的格局。

获取关于二维码支付市场的更多详细见解 申请免费样本

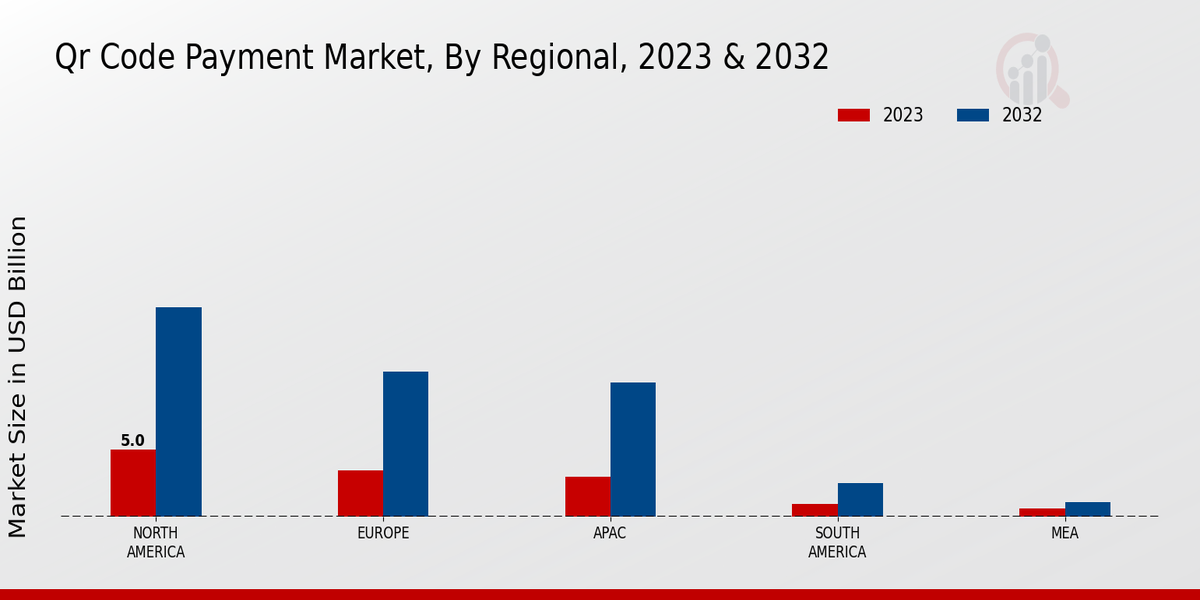

二维码支付市场的收入在各个地区反映出强劲的增长轨迹,市场在2023年的估值为131.3亿美元。北美在这一领域占据主导地位,2023年市场份额为50亿美元,预计到2032年将达到156亿美元。这一显著增长得益于智能手机的高普及率和无接触支付解决方案的采用。

欧洲紧随其后,2023年贡献35亿美元,预计将增长至108亿美元,因为企业越来越多地将二维码支付集成到他们的系统中。亚太地区的市场估值为30亿美元,预计将上升至100亿美元,主要受益于技术娴熟的人口和日益增长的电子商务活动。南美在2023年的价值为10亿美元,预计将增长至25亿美元,表明对数字支付方式的认识和接受度在不断提高。

最后,中东和非洲地区在2023年的估值为6.3亿美元,预计将增长至11亿美元,由于移动支付的快速普及和数字基础设施的蓬勃发展,显示出潜力。这些统计数据展示了二维码支付市场细分中的不同动态,强调了区域市场趋势及其在促进市场增长中的重要性。

来源:初步研究,二次研究,MRFR数据库和分析师评审

二维码支付市场近年来经历了显著增长,主要受到消费者和商家对数字支付解决方案日益接受的推动。该市场的特点是服务提供商种类繁多,各自竞争以提升其产品并占据不断演变的支付市场的更大份额。市场中的主要参与者专注于技术进步、战略合作伙伴关系和创新营销策略,以使自己与众不同。新进入者提供的颠覆性解决方案专门针对细分市场,进一步加剧了竞争。

随着消费者越来越倾向于二维码支付的便利性和安全性,各公司正在投资扩大其全球影响力,改善用户体验,并确保遵守监管标准。Square在二维码支付市场中建立了强大的存在,利用其广泛的支付生态系统为商家和客户提供无缝的支付体验。其用户友好的界面和具有竞争力的交易费用使其成为中小型企业采用现代支付解决方案的一个有吸引力的选择。Square的集成工具,如销售点系统和分析服务,使商家能够更高效地跟踪销售和管理库存。

该公司致力于增强安全功能,包括加密和欺诈检测,使用户感到安心,并有助于提高对二维码交易的信任。此外,Square在扩展其服务套件方面的持续创新使其在竞争对手中处于有利地位,使其能够保持现有客户的忠诚度,同时吸引新客户。Adyen已成为二维码支付市场的主要参与者,提供全面的支付平台,支持各类企业管理其数字支付需求。

凭借其强大的全球支付基础设施,Adyen使商家能够在各种渠道(包括店内、在线和移动)无缝处理二维码支付。该公司因其提供统一商业方法的能力而受到认可,这使企业能够简化其支付流程并获得有关消费者行为的宝贵见解。Adyen强调定价透明,并实施了尖端技术以促进快速和安全的交易。

其战略重点是与各种金融机构建立合作伙伴关系,并具备适应不同市场条件的能力,使Adyen在二维码支付领域继续扩展其影响力时具备竞争优势,以满足对高效和灵活支付解决方案日益增长的需求。

二维码支付市场预计将在2024年至2035年间以13.18%的年复合增长率增长,推动因素包括数字交易的增加、消费者对无接触支付的偏好以及技术进步。

新机遇在于:

到2035年,二维码支付市场预计将成为数字交易的主导力量。

| 2024年市场规模 | 168.2(十亿美元) |

| 2025年市场规模 | 190.4(十亿美元) |

| 2035年市场规模 | 656.7(十亿美元) |

| 年复合增长率(CAGR) | 13.18%(2024 - 2035) |

| 报告覆盖范围 | 收入预测、竞争格局、增长因素和趋势 |

| 基准年 | 2024 |

| 市场预测期 | 2025 - 2035 |

| 历史数据 | 2019 - 2024 |

| 市场预测单位 | 十亿美元 |

| 主要公司简介 | 市场分析进行中 |

| 覆盖的细分市场 | 市场细分分析进行中 |

| 主要市场机会 | 二维码支付系统与移动钱包的集成提升了消费者便利性和交易速度。 |

| 主要市场动态 | 消费者对无接触交易的偏好上升,推动二维码支付解决方案在各个行业的快速采用。 |

| 覆盖的国家 | 北美、欧洲、亚太、南美、中东和非洲 |

The secondary research process involved comprehensive analysis of regulatory databases, fintech publications, banking industry reports, and authoritative digital payment organizations. Key sources included the Bank for International Settlements (BIS), International Monetary Fund (IMF) Financial Sector Reports, World Bank Global Findex Database, Payment Card Industry Security Standards Council (PCI SSC), European Central Bank (ECB) Statistical Data Warehouse, Federal Reserve Payment Systems Research, Bank of England Payment and Settlement Statistics, Reserve Bank of India (RBI) Digital Payment Indicators, People's Bank of China (PBOC) Financial Statistics, Monetary Authority of Singapore (MAS) Payment Systems Oversight, International Telecommunication Union (ITU) ICT Statistics, GSM Association (GSMA) Mobile Money Reports, National Bureau of Statistics of China, US Bureau of Economic Analysis (BEA) Digital Economy Reports, Eurostat Digital Economy and Society Statistics, Asian Development Bank (ADB) Financial Inclusion Data, Central Banks of key markets (Federal Reserve, ECB, Bank of Japan, Bank of England), and national financial regulatory authorities. These sources were used to collect transaction volume statistics, regulatory compliance data, security standard frameworks, digital adoption trends, and market landscape analysis for static QR codes, dynamic QR codes, encrypted QR codes, mobile wallets, banking applications, and e-commerce payment integrations.

Qualitative and quantitative insights were obtained by interviewing supply-side and demand-side stakeholders during the primary research process. The supply-side sources consist of CEOs, CTOs, VPs of Product Development, chiefs of Digital Payments Innovation, regulatory compliance officers, and commercial directors from QR code payment solution providers, mobile wallet operators, banking technology vendors, and fintech infrastructure companies. Demand-side sources included chief digital officers at retail chains, heads of payments at transportation authorities, F&B operations directors, healthcare administration executives, merchant acquisition managers, and procurement leads from enterprise merchants, SMB aggregators, and payment service providers. Market segmentation was verified, product development roadmaps were confirmed, and insights regarding technology adoption patterns, transaction fee structures, and interoperability frameworks were obtained through primary research.

Primary Respondent Breakdown:

By Designation: C-level Primaries (32%), Director Level (31%), Others (37%)

By Region: North America (32%), Europe (30%), Asia-Pacific (33%), Rest of World (5%)

Global market valuation was derived through transaction volume mapping and revenue analysis across the value chain. The methodology included:

Identification of 50+ key stakeholders across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa

Product mapping across static QR codes, dynamic QR codes, encrypted QR codes, and integrated payment technologies

Analysis of reported and modeled annual transaction values specific to QR code payment portfolios

Coverage of stakeholders representing 75-80% of global market share in 2024

Extrapolation using bottom-up (transaction volume × average transaction value by country/segment) and top-down (payment provider revenue validation) approaches to derive segment-specific valuations across retail, transportation, food and beverage, healthcare, and entertainment applications

请填写以下表格以获取本报告的免费样本

“This is really good guys. Excellent work on a tight deadline. I will continue to use you going forward and recommend you to others. Nice job”

“Thanks. It’s been a pleasure working with you, please use me as reference with any other Intel employees.”

“Thanks for sending the report it gives us a good global view of the Betaïne market.”

“Thank you, this will be very helpful for OQS.”

“We found the report very insightful! we found your research firm very helpful. I'm sending this email to secure our future business.”

“I am very pleased with how market segments have been defined in a relevant way for my purposes (such as "Portable Freezers & refrigerators" and "last-mile"). In general the report is well structured. Thanks very much for your efforts.”

“I have been reading the first document or the study, ,the Global HVAC and FP market report 2021 till 2026. Must say, good info! I have not gone in depth at all parts, but got a good indication of the data inside!”

“We got the report in time, we really thank you for your support in this process. I also thank to all of your team as they did a great job.”

“The Automotive 48V ECU Components Procurement Intelligence Study” was a complex project, but the Market Research Future (MRFR) team handled it with quality, agility, and customer-centricity. They delivered all requested data on time and within the agreed scope. The team, including Shubhendra Anand and Rahul Gotadki, was always readily available to clarify questions and swiftly implement necessary adjustments, driving the project to a successful conclusion within a very demanding timeframe.

I would also like to specifically commend Akshay Agarwal for his responsiveness and support at every stage—from our initial inquiry on May 6th through to final delivery on June 18th. His dedication made the entire process seamless.”