What is the projected market valuation of the Synchronous Condenser Market by 2035?

The projected market valuation for the Synchronous Condenser Market is expected to reach 1.083 USD Billion by 2035.

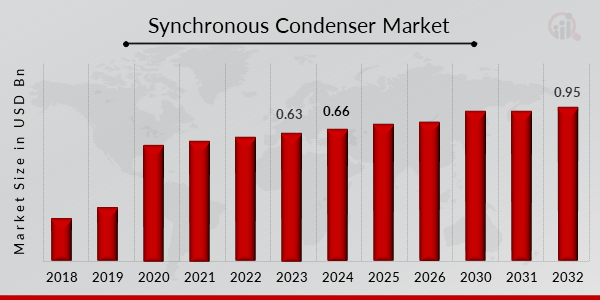

What was the market valuation of the Synchronous Condenser Market in 2024?

The overall market valuation of the Synchronous Condenser Market was 0.66 USD Billion in 2024.

What is the expected CAGR for the Synchronous Condenser Market during the forecast period 2025 - 2035?

The expected CAGR for the Synchronous Condenser Market during the forecast period 2025 - 2035 is 4.6%.

Which companies are considered key players in the Synchronous Condenser Market?

Key players in the Synchronous Condenser Market include General Electric, Siemens, Schneider Electric, Mitsubishi Electric, ABB, Eaton, Hitachi Energy, Toshiba, and S&C Electric Company.

What are the projected valuations for different cooling types in the Synchronous Condenser Market?

Projected valuations for cooling types include Hydrogen at 0.15 to 0.25 USD Billion, Air at 0.25 to 0.4 USD Billion, and Water at 0.26 to 0.43 USD Billion.

How does the reactive power rating segment perform in the Synchronous Condenser Market?

The reactive power rating segment shows projected valuations of 0.2 to 0.32 USD Billion for 'Up to 100 MVAr', 0.25 to 0.4 USD Billion for 'Between 100 MVAr-200 MVAr', and 0.21 to 0.35 USD Billion for 'Above 200 MVAr'.

What is the market outlook for new versus refurbished synchronous condensers?

The market outlook indicates that new synchronous condensers are projected to reach 0.396 to 0.649 USD Billion, while refurbished units are expected to achieve 0.264 to 0.434 USD Billion.

What starting methods are utilized in the Synchronous Condenser Market?

Starting methods in the Synchronous Condenser Market include Static Frequency Converters projected at 0.25 to 0.4 USD Billion, Pony Motors at 0.2 to 0.3 USD Billion, and Others at 0.21 to 0.383 USD Billion.

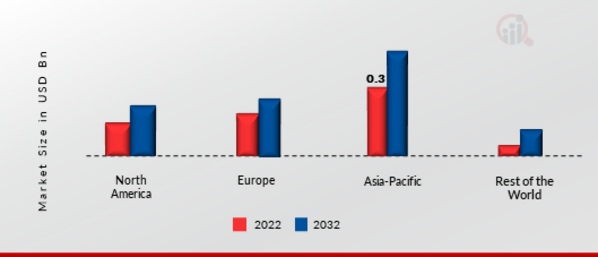

Which end-use sectors are driving the Synchronous Condenser Market?

The end-use sectors driving the market include Electric Utilities, projected at 0.396 to 0.634 USD Billion, and Industries, expected to reach 0.264 to 0.449 USD Billion.

What trends are influencing the growth of the Synchronous Condenser Market?

Trends influencing growth include increasing demand for reactive power support and advancements in synchronous condenser technology, contributing to the overall market expansion.