Data Center Colocation Market Analysis

ID: MRFR/ICT/2688-HCR

100 Pages

October 2025

Data Center Colocation Market Research Report Information By Type (Retail Colocation, Wholesale Colocation), By Deployment Type (Cloud, On-Premises), By End-User (BFSI, IT and telecom, Government and Defense, Healthcare) And By Region (North America, Europe, Asia-Pacific, And Rest Of The World) –Market Forecast Till 2035.

Market Summary

As per Market Research Future Analysis, the Data Center Colocation Market is set to experience significant growth, driven by the increasing demand for data management solutions and the rise of cloud computing. The market is expected to expand from USD 68.44 Billion in 2024 to USD 249.83 Billion by 2035, reflecting a robust CAGR of 12.49% during the forecast period. The surge in data generated from social media and OTT platforms, coupled with the need for cost-effective IT solutions, is propelling this growth. Retail colocation is the dominant segment, catering primarily to small-scale organizations, while cloud deployment is leading in revenue generation. North America is anticipated to maintain its dominance in the market, supported by major cloud service providers and increasing e-commerce activities.

Key Market Trends & Highlights

Key trends driving the Data Center Colocation Market include the following:

- Market Size in 2024: USD 68.44 Billion. Projected Market Size by 2035: USD 249.83 Billion. CAGR from 2025 to 2035: 12.49%. Retail colocation segment dominated the market, benefiting small-scale organizations.

Market Size & Forecast

| 2024 Market Size | USD 68.44 Billion |

| 2035 Market Size | USD 249.83 Billion |

| CAGR (2025-2035) | 12.49% |

| Largest Regional Market Share in 2024 | North America |

Major Players

<p>Key players include Equinix Inc., Fibernet Inc., Keppel Data Center Pte Ltd., NTT Communications Corporation, AT&T Inc., and Digital Realty Trust Inc.</p>

Market Trends

The increasing volume of data coming from social media is driving the market growth

As a result, high ownership and maintenance costs for data centers, particularly for businesses that produce variable volumes of data, are anticipated to be a major factor in the market's growth. Data center colocation offers customers several advantages in addition to reducing capital expenditures. In addition to the price incurred for installing the necessary fiber cabling, research studies indicate that owning or building a data center facility may cost more than USD 300 per square foot. For SMEs, handling an entire data center facility in-house comes at a high cost, whereas large-scale organizations can easily cover this expense.

Data center colocation is one such solution which supports SMEs with a workable and affordable alternative of renting data center space, which is expected to drive the market CAGR over the forecast period.

The demand for data centers and colocation services has increased due to the increasing volume of data coming from social media and Over-The-Top (OTT) platforms. Social media users are becoming increasingly active, resulting in an exponential increase in the amount of data generated by these platforms. For instance, monthly active Facebook users increased to roughly 2.74 billion in 2020 from 2.38 billion in 2019. The number of people using social media is predicted to increase even more in the upcoming years, which will increase demand for colocation facilities.

The Covid-19 pandemic has also caused a rise in OTT and streaming service usage, which has increased data volumes and is expected to drive market growth.

There is a greater need for higher bandwidths and faster data processing due to the development of technologies like the Internet of Things (IoT), cloud computing, autonomous vehicles, and advanced robotics. Lower latency and faster network connectivity are necessary to use these technologies effectively. Colocation data centers are a good fit to meet these needs because the operators can place their facilities close to the users and thus provide better networking and storage services. Additionally, the development of 5G is anticipated to accelerate the deployment of colocation services because it will allow colocation providers to offer services in remote areas.

Because of their lower costs, cloud data centers are becoming increasingly popular, which is expected to restrain market expansion. Cloud services are becoming increasingly popular among smaller businesses because they are scalable, affordable, don't require an IT staff, and have lower overheads. Long-term cost savings and flexibility in terms of total server control are both provided by colocation facilities. Enterprises are choosing colocation services in large numbers because of these features. Thus, driving the data center colocation market revenue.

<p>The ongoing evolution of digital infrastructure is driving a robust demand for data center colocation services, as organizations increasingly seek to enhance operational efficiency and scalability in a competitive landscape.</p>

U.S. Department of Commerce

Data Center Colocation Market Market Drivers

Market Growth Projections

The Global Data Center Colocation Market Industry is poised for remarkable growth, with projections indicating a market size of 68.4 USD Billion in 2024 and an anticipated increase to 249.8 USD Billion by 2035. This represents a compound annual growth rate (CAGR) of 12.49% from 2025 to 2035. Such growth is driven by various factors, including the rising demand for cloud services, increased focus on data security, and the expansion of IoT technologies. The market dynamics suggest that colocation services will remain integral to the evolving digital landscape, as businesses increasingly rely on external data centers for their operational needs.

Increased Focus on Data Security

Data security remains a paramount concern for organizations worldwide, propelling the Global Data Center Colocation Market Industry forward. As cyber threats evolve, businesses are compelled to adopt robust security measures, often turning to colocation providers that offer advanced security protocols. These facilities typically feature redundant power supplies, fire suppression systems, and physical security measures, which are crucial for safeguarding sensitive information. The emphasis on compliance with regulations such as GDPR and HIPAA further underscores the necessity for secure colocation services, indicating a sustained growth trajectory for this market segment.

Rising Demand for Cloud Services

The Global Data Center Colocation Market Industry experiences a notable increase in demand for cloud services, driven by businesses seeking scalable and flexible IT solutions. As organizations migrate to cloud-based infrastructures, colocation facilities become essential for housing critical hardware. In 2024, the market is projected to reach 68.4 USD Billion, reflecting the growing reliance on cloud technologies. This trend is likely to continue as companies prioritize efficiency and cost-effectiveness, suggesting that the colocation sector will play a pivotal role in supporting cloud service providers and enterprises alike.

Emerging Markets and Urbanization

Emerging markets and urbanization contribute to the expansion of the Global Data Center Colocation Market Industry. As developing regions experience rapid urban growth, the demand for reliable data infrastructure intensifies. Countries in Asia-Pacific and Latin America are witnessing significant investments in colocation facilities to support their burgeoning digital economies. This trend is expected to drive the market's growth, with projections indicating a rise to 249.8 USD Billion by 2035. The increasing urban population necessitates enhanced connectivity and data management solutions, further solidifying the role of colocation providers in these regions.

Expansion of Internet of Things (IoT)

The proliferation of Internet of Things (IoT) devices significantly influences the Global Data Center Colocation Market Industry. With billions of devices generating vast amounts of data, the need for efficient data processing and storage solutions becomes increasingly critical. Colocation facilities provide the necessary infrastructure to handle this influx of data, enabling businesses to leverage IoT technologies effectively. As the number of connected devices is expected to reach 30 billion by 2035, the demand for colocation services is likely to surge, positioning the industry for substantial growth in the coming years.

Sustainability Initiatives and Energy Efficiency

Sustainability initiatives and energy efficiency are becoming critical drivers in the Global Data Center Colocation Market Industry. As environmental concerns gain prominence, colocation providers are adopting green practices to reduce their carbon footprints. This includes utilizing renewable energy sources and implementing energy-efficient technologies. Companies are increasingly seeking colocation partners that align with their sustainability goals, which may enhance their corporate social responsibility profiles. The shift towards sustainable operations not only meets regulatory requirements but also appeals to environmentally conscious consumers, suggesting a potential competitive advantage for providers who prioritize eco-friendly practices.

Market Segment Insights

Data Center Colocation Type Insights

<p>Based on type, the data center colocation market segmentation includes retail colocation and wholesale colocation. The retail colocation segment dominated the market, Businesses can rent a portion of a data center's space through retail colocation. Managing small amounts of data or when infrastructure is only required temporarily gives businesses flexibility. Due to their lower need for data storage than large organizations, small-scale organizations can benefit the most from it. Additionally, businesses that want to take advantage of colocation services but are on a tight budget should look into the retail type.</p>

Data Center Colocation Deployment Type Insights

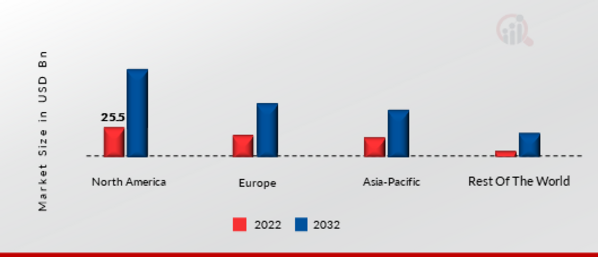

<p>Based on deployment type, the data center colocation market segmentation includes cloud and on-premises. The cloud category generated the most income. Cloud deployment refers to using <a href="https://www.marketresearchfuture.com/reports/cloud-computing-market-1013">cloud computing services</a> to manage and store data and applications. Cloud service providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP) provide various services that can be accessed and managed online, including computing power, storage, and database services.</p>

<p>Figure 2: Data Center Colocation Market, by Deployment Type, 2022 & 2032 (USD billion)</p>

<p>Source: Secondary Research, Primary Research, Market Research Future Database and Analyst Review</p>

Data Center Colocation End-User Insights

<p>Based on End-User, the data center colocation market segmentation includes BFSI, IT and telecom, government and defense, and healthcare. The IT and telecom categories generated the most income. The growing number of mobile internet users and the industry's ongoing development of new software are responsible for this segment's high market share. The GSM Association (GSMA) estimates that 3.8 people connected to the mobile internet in 2019, an increase of 250 million users from 2018. Due to the growing use of smartphones with advanced features, this number will inevitably increase.</p>

<p>In the meantime, the development of 5G is anticipated to further support the growth of the IT and telecom industries, generating significant amounts of data and propelling market expansion.</p>

Get more detailed insights about Data Center Colocation Market Research Report- Forecast 2032

Regional Insights

By region, the study provides market insights into North America, Europe, Asia-Pacific and the Rest of the World. The North American data center colocation market area will dominate this market, Due to the significant presence of several major cloud service providers and the deployment of colocation data centers by SMEs throughout the region, the regional market is predicted to grow further at a significant CAGR from 2021 to 2028. Furthermore, rising e-commerce sales in the U.S. assist in expanding the local market.

Retailers are heavily investing in their IT infrastructure for storing customer data, which can be used to identify customer buying patterns and product demands based on various categories, such as region, gender, and age group.

Further, the major countries studied in the market report are The U.S., Canada, German, France, the UK, Italy, Spain, China, Japan, India, Australia, South Korea, and Brazil.

Figure 3: DATA COLOCATION CENTER MARKET SHARE BY REGION 2022 (%)

Source: Secondary Research, Primary Research, Market Research Future Database and Analyst Review

Europe’s data center colocation market accounts for the second-largest market share. The rising adoption of connected technologies, thanks to a cloud-friendly infrastructure and stringent data compliance regulations, is driving the need for interconnection hubs. Data centers are in high demand in the region to protect data and stop it from being shared across borders, which is good news for the market. Further, the German data center colocation market held the largest market share, and the UK data center colocation market was the fastest-growing market in the European region.

The Asia-Pacific Data Center Colocation Market is expected to grow at the fastest CAGR from 2023 to 2032 due to the growing number of internet users in the area. The market’s growth is also aided by some of the area's biggest software companies and IT BPO outsourcing service providers. Additionally, as smart technology and appliances become more widely used, the volume of data generated has increased, forcing businesses from various industries to set up data centers.

Moreover, China’s data center colocation market held the largest market share, and the Indian data center colocation market was the fastest-growing market in the Asia-Pacific region.

Key Players and Competitive Insights

Leading market players are investing heavily in research and development in order to expand their product lines, which will help the data center colocation market grow even more. Market participants are also undertaking various strategic activities to expand their footprint, with important market developments including new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaboration with other organizations. The data center colocation industry must offer cost-effective items to expand and survive in a more competitive and rising market climate.

Manufacturing locally to minimize operational costs is one of the key business tactics manufacturers use in the data center colocation industry to benefit clients and increase the market sector. The data center colocation industry has offered some of the most significant advantages in recent years.

Major data center colocation market players, including Equinix Inc. (US), Fibernet Inc. (US), Keppel Data Center Pte Ltd. (Singapore), NTT Communications Corporation (Japan), AT&T Inc. (US), Cogent Communications (US), CoreSite Realty Corporation (US), Cyxtera Technologies Inc. (US), Digital Realty Trust Inc. (US), DuPont Fabros Technology Inc. (US), PhoenixNAP (US), Rahi Systems Inc (US) and others, are attempting to increase market demand by investing in research and development operations.

DuPont Fabros Technology Inc. (US), Often abbreviated as DuPont, the French-American industrialist and chemist Éleuthère Irénée du Pont de Nemours founded the multinational chemical company in 1802. The business began as a significant supplier of gunpowder and later played a significant role in the growth of Delaware. In the 20th century, DuPont produced a variety of polymers, including Vespel, neoprene, nylon, Corian, Teflon, Mylar, Kapton, Kevlar, Zemdrain, M5 fiber, Nomex, Tyvek, Sorona, Corfam, and Lycra. Its scientists also produced a variety of chemicals, most notably Freon (chlorofluorocarbons), for the refriger. Additionally, it produced synthetic paints and pigments like ChromaFlair.

Equinix is the world’s digital infrastructure company. We interconnect industry-leading organizations such as finance, manufacturing, retail, transportation, government, healthcare and education across a digital-first world. Business leaders harness our trusted platform to unite and interconnect sustainably and securely the foundational infrastructure that powers their success.

Founded in Silicon Valley in 1998 as a vendor-neutral multitenant data center provider where competing networks could securely connect and share data traffic, we chose a name that reflected our company’s focus on EQUality, Neutrality and Internet eXchange—Equinix. Through Platform Equinix® and our ecosystem of leading service providers, digital leaders fast-track competitive advantage across clouds, networking, storage, computing and software.

Key Companies in the Data Center Colocation Market market include

Industry Developments

- Q2 2025: Digital Realty to Acquire Data Center Portfolio in India for $1.5 Billion Digital Realty announced the acquisition of a major data center portfolio in India for $1.5 billion, expanding its colocation footprint in the rapidly growing APAC market.

- Q2 2025: Equinix Opens New $200 Million Data Center in Singapore Equinix launched a new $200 million colocation facility in Singapore, aiming to meet surging demand for cloud and AI workloads in Southeast Asia.

- Q2 2025: NTT and Schneider Electric Announce Strategic Partnership for Sustainable Data Centers NTT and Schneider Electric entered a strategic partnership to develop and operate sustainable colocation data centers, focusing on energy efficiency and renewable integration.

- Q1 2025: Iron Mountain Completes Acquisition of XData’s European Colocation Assets Iron Mountain completed its acquisition of XData’s European colocation assets, strengthening its presence in the region’s data center market.

- Q1 2025: CyrusOne Appoints New CEO to Lead Global Expansion CyrusOne announced the appointment of a new CEO, effective immediately, to drive the company’s next phase of global colocation expansion.

- Q4 2024: EdgeConneX Raises $1 Billion in Green Financing for Data Center Expansion EdgeConneX secured $1 billion in green financing to fund the expansion of its global colocation data center portfolio, with a focus on sustainability.

- Q4 2024: STACK Infrastructure Announces Opening of New 80MW Data Center Campus in Frankfurt STACK Infrastructure opened a new 80MW colocation data center campus in Frankfurt, Germany, to support hyperscale and enterprise clients.

- Q4 2024: DigitalBridge Closes $500 Million Investment in Latin American Data Center Platform DigitalBridge completed a $500 million investment in a Latin American data center platform, expanding its colocation services in the region.

- Q3 2024: QTS Realty Trust Breaks Ground on New 200MW Data Center Campus in Phoenix QTS Realty Trust began construction on a new 200MW colocation data center campus in Phoenix, Arizona, to meet growing demand from cloud and enterprise customers.

- Q3 2024: Colt Data Centre Services Launches New Facility in Osaka, Japan Colt Data Centre Services launched a new colocation facility in Osaka, Japan, expanding its APAC presence and supporting regional digital transformation.

- Q2 2024: Aligned Data Centers Secures $400 Million in Debt Financing for U.S. Expansion Aligned Data Centers secured $400 million in debt financing to accelerate the expansion of its U.S. colocation data center footprint.

- Q2 2024: Vantage Data Centers Announces $900 Million Investment to Expand European Operations Vantage Data Centers announced a $900 million investment to expand its colocation operations across key European markets, including Germany and the UK.

Future Outlook

Data Center Colocation Market Future Outlook

<p>The Data Center Colocation Market is poised for growth at 12.49% CAGR from 2025 to 2035, driven by increasing demand for cloud services, edge computing, and sustainability initiatives.</p>

New opportunities lie in:

- <p>Invest in green energy solutions to enhance sustainability and attract eco-conscious clients. Develop hybrid colocation services integrating on-premises and cloud solutions for flexibility. Expand into emerging markets with tailored services to capture new customer segments.</p>

<p>By 2035, the Data Center Colocation Market is expected to be robust, reflecting substantial growth and innovation.</p>

Market Segmentation

Data Center Colocation Type Outlook

- Retail Colocation

- Wholesale Colocation

Data Center Colocation End-User Outlook

- BFSI

- IT and telecom

- Government and defense

- Healthcare

Data Center Colocation Regional Outlook

- {""=>["US"

- "Canada"]}

- {""=>["Germany"

- "France"

- "UK"

- "Italy"

- "Spain"

- "Rest of Europe"]}

- {""=>["China"

- "Japan"

- "India"

- "Australia"

- "South Korea"

- "Rest of Asia-Pacific"]}

- {""=>["Middle East"

- "Africa"

- "Latin America"]}

Data Center Colocation Deployment Type Outlook

- Cloud

- On-Premises

Report Scope

| Attribute/Metric | Details |

| Market Size 2024 | USD 68.44 Billion |

| Market Size 2035 | 249.83 (Value (USD Billion)) |

| Compound Annual Growth Rate (CAGR) | 12.49% (2025 - 2035) |

| Base Year | 2024 |

| Market Forecast Period | 2025 - 2035 |

| Historical Data | 2018- 2022 |

| Market Forecast Units | Value (USD Billion) |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered | Type, Deployment Type, End-User, and Region |

| Geographies Covered | North America, Europe, Asia Pacific, and the Rest of the World |

| Countries Covered | The U.S., Canada, German, France, UK, Italy, Spain, China, Japan, India, Australia, South Korea, and Brazil |

| Key Companies Profiled | Equinix Inc. (US), Fibernet Inc. (US), Keppel Data Center Pte Ltd. (Singapore), NTT Communications Corporation (Japan), AT&T Inc. (US), Cogent Communications (US), CoreSite Realty Corporation (US), Cyxtera Technologies Inc. (US), Digital Realty Trust Inc. (US), DuPont Fabros Technology Inc. (US), PhoenixNAP (US), Rahi Systems Inc (US) |

| Key Market Opportunities | The increasing volume of data from social media and Over-The-Top (OTT) platforms and because of their lower costs, |

| Key Market Dynamics | Cloud data centers are becoming increasingly popular |

| Market Size 2025 | 76.99 (Value (USD Billion)) |

Market Highlights

Author

Latest Comments

John Doe

john@example.com

This is a great article! Really helped me understand the topic better.

Posted on July 23, 2025, 10:15

AM

Jane Smith

jane@domain.com

Thanks for sharing this. I’ve bookmarked it for later reference.

Posted on July 22, 2025, 7:45

PM

FAQs

How much is the data center colocation market?

The data center colocation market size was valued at USD 59.83 Billion in 2023.

What is the growth rate of the data center colocation market?

The market is projected to grow at a CAGR of 12.49% during 2024-2032.

Which region held the largest data center colocation market share?

North America had the largest share of the market

Who are the key players in the data center colocation market?

The key players in the market are Equinix Inc. (US), Fibernet Inc. (US), Keppel Data Center Pte Ltd. (Singapore), NTT Communications Corporation (Japan), AT&T Inc. (US), Cogent Communications (US), CoreSite Realty Corporation (US), Cyxtera Technologies Inc. (US), Digital Realty Trust Inc. (US), DuPont Fabros Technology Inc. (US), PhoenixNAP (US), Rahi Systems Inc (US).

Which type led the data center colocation market?

The retail colocation category dominated the market in 2022.

Which deployment type had the largest data center colocation market share?

The cloud had the largest share in the market.

-

Table of Contents 1 MARKET INTRODUCTION

-

1.1 INTRODUCTION

-

1.2 SCOPE OF STUDY

-

1.2.1 RESEARCH OBJECTIVE

-

1.2.2 ASSUMPTIONS

-

1.2.3 LIMITATIONS

-

1.3 MARKET STRUCTURE:

-

1.3.1 GLOBAL DATA CENTER COLOCATION MARKET: BY TYPE

-

1.3.2 GLOBAL DATA CENTER COLOCATION MARKET: BY DEPLOYMENT TYPE

-

1.3.3 GLOBAL DATA CENTER COLOCATION MARKET: BY END USER

-

1.3.4 GLOBAL DATA CENTER COLOCATION MARKET: BY REGION 2 Research Methodology

-

2.1 RESEARCH DEPLOYMENT TYPE

-

2.2 PRIMARY RESEARCH

-

2.3 SECONDARY RESEARCH

-

2.4 FORECAST MODEL 3 MARKET DYNAMICS

-

3.1 INTRODUCTION

-

3.2 MARKET DRIVERS

-

3.3 MARKET CHALLENGES

-

3.4 MARKET OPPORTUNITIES 4 Executive Summary 5. MARKET FACTOR ANALYSIS

-

5.1 PORTER’S FIVE FORCES ANALYSIS

-

5.2 SUPPLY CHAIN ANALYSIS 6 DATA CENTER COLOCATION MARKET

-

6.1 INTRODUCTION

-

6.2 MARKET STATISTICS

-

6.2.1 BY TYPE

-

6.2.1.1 RETAIL COLOCATION

-

6.2.1.2 WHOLESALE COLOCATION

-

6.2.1.3 OTHERS

-

6.2.2 BY DEPLOYMENT TYPE

-

6.2.2.1 CLOUD

-

6.2.2.2 ON PREMISES

-

6.2.2.3 OTHERS

-

6.2.3 BY END-USER

-

6.2.3.1 HEALTHCARE

-

6.2.3.2 BFSI

-

6.2.3.3 GOVERNMENT AND DEFENSE

-

6.2.3.4 IT AND TELECOM

-

6.2.3.5 OTHERS

-

6.2.4 BY REGION

-

6.2.4.1 NORTH AMERICA

-

6.2.4.2 EUROPE

-

6.2.4.3 ASIA PACIFIC

-

6.2.4.4 REST OF THE WORLD 7 COMPANY PROFILES

-

7.1 EQUINIX, INC. (U.S.)

-

7.2 FIBERNET INC. (U.S.)

-

7.3 NTT COMMUNICATIONS CORPORATION (JAPAN)

-

7.4 AT&T INC. (U.S.)

-

7.5 CORESITE REALTY CORPORATION (U.S.)

-

7.6 COGENT COMMUNICATIONS (U.S.)

-

7.7 KEPPEL DATA CENTER PTE LTD. (SINGAPORE)

-

7.8 CYXTERA TECHNOLOGIES, INC. (U.S.)

-

7.9 DIGITAL REALTY TRUST, INC. (U.S.)

-

7.10 DUPONT FABROS TECHNOLOGY, INC. (U.S.)

-

7.11 VERIZON COMMUNICATIONS, INC. (U.S.)

-

7.12 OTHERS

-

List of Tables and Figures

- LIST OF TABLES

- TABLE 1 DATA CENTER COLOCATION MARKET, BY TYPE

- TABLE 2 DATA CENTER COLOCATION MARKET, BY DEPLOYMENT TYPE

- TABLE 3 DATA CENTER COLOCATION MARKET, BY END-USER

- TABLE 4 DATA CENTER COLOCATION MARKET, BY REGIONS

- TABLE 5 NORTH AMERICA DATA CENTER COLOCATION MARKET, BY TYPE

- TABLE 6 NORTH AMERICA DATA CENTER COLOCATION MARKET, BY DEPLOYMENT TYPE

- TABLE 7 NORTH AMERICA DATA CENTER COLOCATION MARKET, BY END USER

- TABLE 8 NORTH AMERICA DATA CENTER COLOCATION MARKET, BY REGION

- TABLE 9 EUROPE DATA CENTER COLOCATION MARKET, BY TYPE

- TABLE 10 EUROPE DATA CENTER COLOCATION MARKET, BY DEPLOYMENT TYPE

- TABLE 11 EUROPE DATA CENTER COLOCATION MARKET, BY END-USER

- TABLE 12 EUROPE DATA CENTER COLOCATION MARKET, BY REGION

- TABLE 13 U.K. DATA CENTER COLOCATION MARKET, BY TYPE

- TABLE 14 U.K. DATA CENTER COLOCATION MARKET, BY DEPLOYMENT TYPE

- TABLE 15 U.K. DATA CENTER COLOCATION MARKET, BY END-USER

- TABLE 16 U.K. DATA CENTER COLOCATION MARKET, BY REGION

- TABLE 17 ASIA-PACIFIC DATA CENTER COLOCATION MARKET, BY TYPE

- TABLE 18 ASIA-PACIFIC DATA CENTER COLOCATION MARKET, BY DEPLOYMENT TYPE

- TABLE 19 ASIA-PACIFIC DATA CENTER COLOCATION MARKET, BY END-USER

- TABLE 20 ASIA-PACIFIC DATA CENTER COLOCATION MARKET, BY REGION

- TABLE 21 REST OF WORLD DATA CENTER COLOCATION MARKET, BY TYPE

- TABLE 22 REST OF WORLD DATA CENTER COLOCATION MARKET, BY DEPLOYMENT TYPE

- TABLE 23 REST OF WORLD DATA CENTER COLOCATION MARKET, BY END-USER

- TABLE 24 REST OF WORLD DATA CENTER COLOCATION MARKET, BY REGION LIST OF FIGURES

- FIGURE 1 Research Methodology

- FIGURE 2 DATA CENTER COLOCATION MARKET: BY TYPE (%)

- FIGURE 3 DATA CENTER COLOCATION MARKET: BY DEPLOYMENT TYPE (%)

- FIGURE 4 DATA CENTER COLOCATION MARKET: BY END-USER (%)

- FIGURE 5 DATA CENTER COLOCATION MARKET: BY REGION (%)

- FIGURE 6 NORTH AMERICA DATA CENTER COLOCATION MARKET, BY TYPE (%)

- FIGURE 7 NORTH AMERICA DATA CENTER COLOCATION MARKET, BY DEPLOYMENT TYPE (%)

- FIGURE 8 NORTH AMERICA DATA CENTER COLOCATION MARKET, BY END-USER (%)

- FIGURE 9 NORTH AMERICA DATA CENTER COLOCATION MARKET, BY REGION (%)

- FIGURE 10 EUROPE DATA CENTER COLOCATION MARKET, BY TYPE (%)

- FIGURE 11 EUROPE DATA CENTER COLOCATION MARKET, BY DEPLOYMENT TYPE (%)

- FIGURE 12 EUROPE DATA CENTER COLOCATION MARKET, BY END-USER (%)

- FIGURE 13 EUROPE DATA CENTER COLOCATION MARKET, BY REGION (%)

- FIGURE 14 ASIA-PACIFIC DATA CENTER COLOCATION MARKET, BY TYPE (%)

- FIGURE 15 ASIA-PACIFIC DATA CENTER COLOCATION MARKET, BY DEPLOYMENT TYPE (%)

- FIGURE 16 ASIA-PACIFIC DATA CENTER COLOCATION MARKET, BY END-USER (%)

- FIGURE 17 ASIA-PACIFIC DATA CENTER COLOCATION MARKET, BY REGION (%)

- FIGURE 18 ROW DATA CENTER COLOCATION MARKET, BY TYPE (%)

- FIGURE 19 ROW DATA CENTER COLOCATION MARKET, BY DEPLOYMENT TYPE (%)

- FIGURE 20 ROW DATA CENTER COLOCATION MARKET, BY END-USER (%)

- FIGURE 21 ROW DATA CENTER COLOCATION MARKET, BY REGION (%)

Data Center Market Segmentation

Data Center Colocation Type Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

Data Center Colocation Deployment Type Outlook (USD Billion, 2018-2032)

Cloud

On-Premises

Data Center Colocation End-User Outlook (USD Billion, 2018-2032)

BFSI

IT and telecom

Government and defense

Healthcare

Data Center Colocation Regional Outlook (USD Billion, 2018-2032)

North America Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

North America Data Center Colocation by Deployment TypeCloud

On-Premises

North America Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

US Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

US Data Center Colocation by Deployment TypeCloud

On-Premises

US Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

CANADA Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

CANADA Data Center Colocation by Deployment TypeCloud

On-Premises

CANADA Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Europe Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

Europe Data Center Colocation by Deployment TypeCloud

On-Premise

Europe Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Germany Outlook (USD Billion, 2018-2032)

Germany Data Center Colocation by TypeRetail Colocation

Wholesale Colocation

Germany Data Center Colocation by Deployment TypeCloud

On-Premises

Germany Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

France Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

France Data Center Colocation by Deployment TypeCloud

On-Premises

France Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

UK Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

UK Data Center Colocation by Deployment TypeCloud

On-Premises

UK Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

ITALY Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

ITALY Data Center Colocation by Deployment TypeCloud

On-Premises

ITALY Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

SPAIN Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

Spain Data Center Colocation by Deployment TypeCloud

On-Premises

Spain Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Rest Of Europe Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

REST OF EUROPE Data Center Colocation by Deployment TypeCloud

On-Premises

REST OF EUROPE Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Asia-Pacific Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

Asia-Pacific Data Center Colocation by Deployment TypeCloud

On-Premises

Asia-Pacific Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

China Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

China Data Center Colocation by Deployment TypeCloud

On-Premises

China Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Japan Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

Japan Data Center Colocation by Deployment TypeCloud

On-Premises

Japan Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

India Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

India Data Center Colocation by Deployment TypeCloud

On-Premises

India Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Australia Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

Australia Data Center Colocation by Deployment TypeCloud

On-Premises

Australia Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Rest of Asia-Pacific Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

Rest of Asia-Pacific Data Center Colocation by Deployment TypeCloud

On-Premises

Rest of Asia-Pacific Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Rest of the World Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

Rest of the World Data Center Colocation by Deployment TypeCloud

On-Premises

Rest of the World Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Middle East Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

Middle East Data Center Colocation by Deployment TypeCloud

On-Premises

Middle East Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Africa Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

Africa Data Center Colocation by Deployment TypeCloud

On-Premises

Africa Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Latin America Outlook (USD Billion, 2018-2032)

Retail Colocation

Wholesale Colocation

Latin America Data Center Colocation by Deployment TypeCloud

On-Premises

Latin America Data Center Colocation by End-UserBFSI

IT and telecom

Government and defense

Healthcare

Free Sample Request

Kindly complete the form below to receive a free sample of this Report

Customer Strories

“I am very pleased with how market segments have been defined in a relevant way for my purposes (such as "Portable Freezers & refrigerators" and "last-mile"). In general the report is well structured. Thanks very much for your efforts.”

Leave a Comment