Data Center Colocation Market Summary

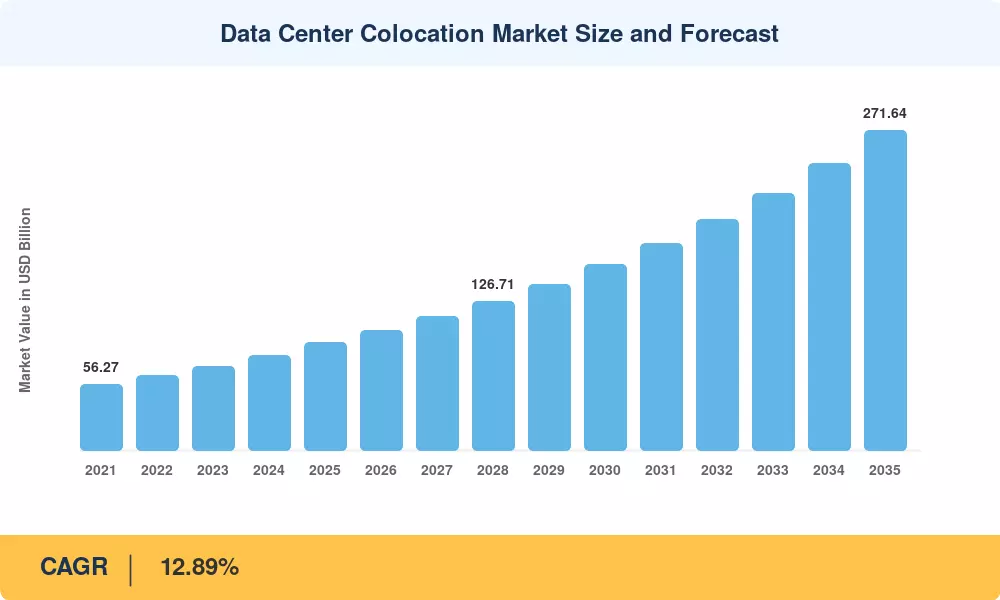

The Data Center Colocation Market stood at an estimated USD 91.38 billion in 2025, with the forecast period launching from USD 101.04 billion in 2026 and climbing to USD 271.64 billion by 2035 at a CAGR of 12.89%. Enterprises across finance, healthcare, and media are accelerating their exit from captive server rooms, driven by the sheer capital intensity of building AI-ready infrastructure in-house. Government-led data-sovereignty mandates in the European Union, India, and the Gulf Cooperation Council states have simultaneously compelled regulated workloads to remain within national borders, locking in multi-year colocation hosting for enterprise IT contracts that underpin predictable revenue for operators [2][3].

A structural technology shift is reshaping facility design. Legacy air-cooled racks rated at 5–8 kW are giving way to power density colocation solutions exceeding 40 kW per cabinet, a transformation fueled by GPU-dense AI training clusters and high-performance computing deployments. Operators that pre-install rear-door heat exchangers and direct-to-chip liquid-cooling loops can command 20–30% price premiums on long-term leases [4]. Global capital expenditure on colocation campus builds surpassed USD 45 billion in 2024, with hyperscalers pre-leasing capacity two to three years before facilities reach commercial operation [5].

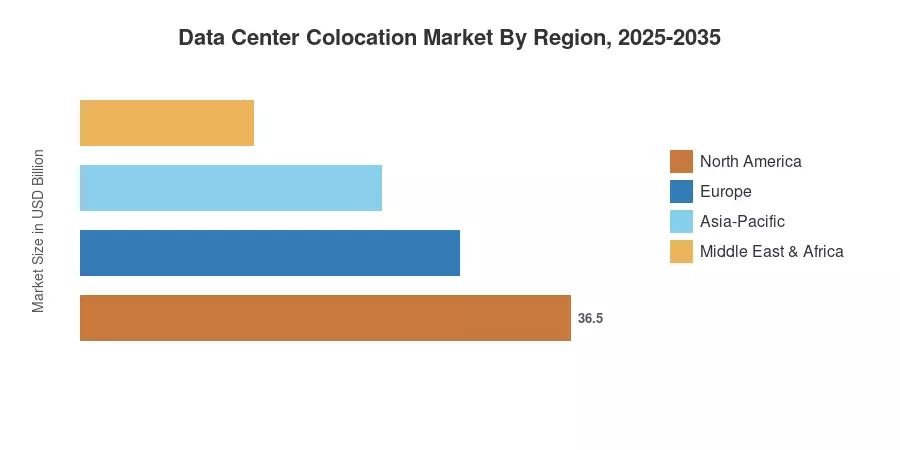

North America commanded roughly 43.8% of the Data Center Colocation Market in 2025, anchored by Northern Virginia's dense fiber ecosystem and carrier-neutral colocation facilities in Dallas, Chicago, and Phoenix. Asia-Pacific is set to register the fastest CAGR of 13.72% through 2035 as cloud adoption in India, Southeast Asia, and Japan accelerates. Europe held the second-largest share at approximately 26%, buoyed by Frankfurt, London, Amsterdam, and Paris — the so-called FLAP corridor — where cross-connect services in colo data centers remain a critical differentiator for financial-services tenants [6][7].

Key Report Takeaways

• By Solution Type

- Retail multi-tenant halls captured an estimated 67.5% of the Data Center Colocation Market revenue in 2025, driven by SME and mid-enterprise demand for fractional-rack deployments

- Wholesale multi-tenant suites are forecast to expand at a 13.35% CAGR through 2035, as hyperscaler pre-leasing fuels large-block absorption

• By Tier Classification

- Tier 3 facilities accounted for roughly 49.8% of the Data Center Colocation Market share in 2025, reflecting the enterprise preference for concurrent maintainability without full fault tolerance costs

- Tier 4 halls are projected to grow at a 13.58% CAGR, propelled by mission-critical financial and healthcare workloads requiring 99.995% uptime and robust data center colo pricing and SLA models

• By Region

- North America generated approximately USD 40.03 billion in 2025, underpinned by the highest density of carrier-neutral colocation facilities globally

- Asia-Pacific is expected to record the fastest regional CAGR of 13.72% to 2035, led by India's Digital India infrastructure push and Japan's AI-focused subsidy programs

Market Research Future (MRFR)'s sizing model triangulates bottom-up operator revenue data, top-down enterprise IT outsourcing spend surveys, and cross-referencing against hyperscaler capex disclosures. Historical figures draw on audited financial filings from the 15 largest publicly listed colocation providers, while forecast projections incorporate planned campus pipelines, utility interconnection queues, and contracted but uncommissioned capacity.