前臨床CRO市場 概要

MRFRの分析によると、前臨床CRO市場の規模は2024年に65.7億米ドルと推定されています。前臨床CRO業界は、2025年に69.39億米ドルから2035年には119.9億米ドルに成長すると予測されており、2025年から2035年の予測期間中に年平均成長率(CAGR)は5.62を示します。

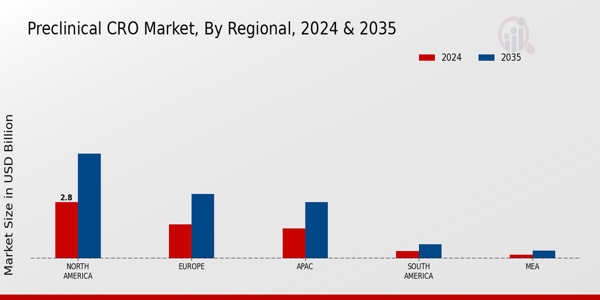

主要な市場動向とハイライト

前臨床CRO市場は、技術の進歩と薬剤開発の需要の増加により、堅調な成長を遂げています。

- 技術統合は前臨床CRO市場の風景を再形成し、研究プロセスの効率と精度を向上させています。北米は依然として最大の市場であり、アジア太平洋地域は前臨床サービスの最も成長が早い地域として浮上しています。バイオロジクス試験は市場を支配し続けており、一方で毒性試験は安全性への懸念の高まりにより急速に成長しています。薬剤開発の需要の高まりとバイオテクノロジーの進展が市場拡大を促進する主要な要因です。

市場規模と予測

| 2024 Market Size | 65.7億米ドル |

| 2035 Market Size | 119.9億ドル |

| CAGR (2025 - 2035) | 5.62% |

主要なプレーヤー

チャールズリバーラボラトリーズ(米国)、コバンス(米国)、PRAヘルスサイエンス(米国)、エンビゴ(米国)、ウーシーアプテック(中国)、メドペース(米国)、ユーロフィン・サイエンティフィック(ルクセンブルク)、シニオスヘルス(米国)、KCR(ポーランド)