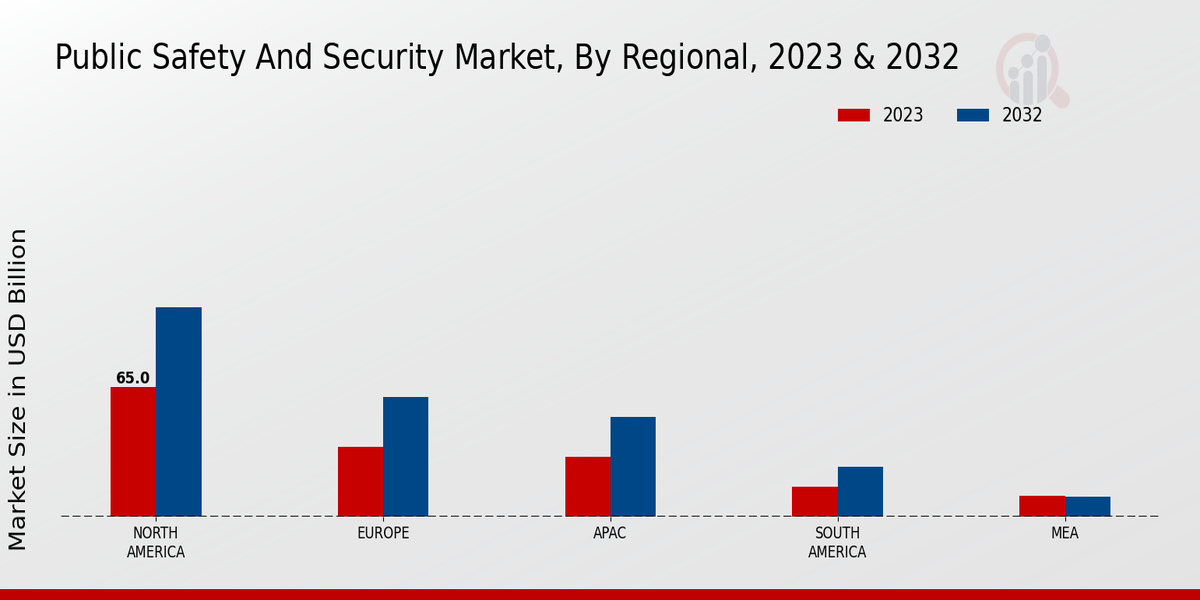

公共安全とセキュリティ市場 概要

MRFRの分析によると、公共の安全とセキュリティ市場は2024年に173.07億米ドルと推定されています。公共の安全とセキュリティ業界は、2025年に182.4億米ドルから2035年までに308.39億米ドルに成長すると予測されており、2025年から2035年の予測期間中に年平均成長率(CAGR)は5.39を示しています。

主要な市場動向とハイライト

公共の安全とセキュリティ市場は、技術の進歩と都市化の進展により、堅調な成長を遂げています。

- 技術の統合は公共の安全プロトコルを再構築し、応答時間と効率を向上させています。

- 協力的な安全イニシアチブが注目を集めており、政府と商業団体の間のパートナーシップを促進しています。

- サイバーセキュリティへの関心が高まっており、脅威が進化する中で高度な保護措置が必要とされています。

- 都市化の進展と犯罪率の上昇は、災害管理および監視・セキュリティセグメントの成長を促進する主要な要因です。

市場規模と予測

| 2024 Market Size | 173.07 (米ドル十億) |

| 2035 Market Size | 308.39 (USD十億) |

| CAGR (2025 - 2035) | 5.39% |

主要なプレーヤー

モトローラ・ソリューションズ(米国)、タレスグループ(フランス)、ヒューレット・パッカード・エンタープライズ(米国)、シーメンスAG(ドイツ)、ハネウェル・インターナショナル(米国)、シスコシステムズ(米国)、ジェネテック社(カナダ)、アクシス・コミュニケーションズ(スウェーデン)、ヴェリント・システムズ(米国)、パランティア・テクノロジーズ(米国)