Telecom Cloud Market Summary

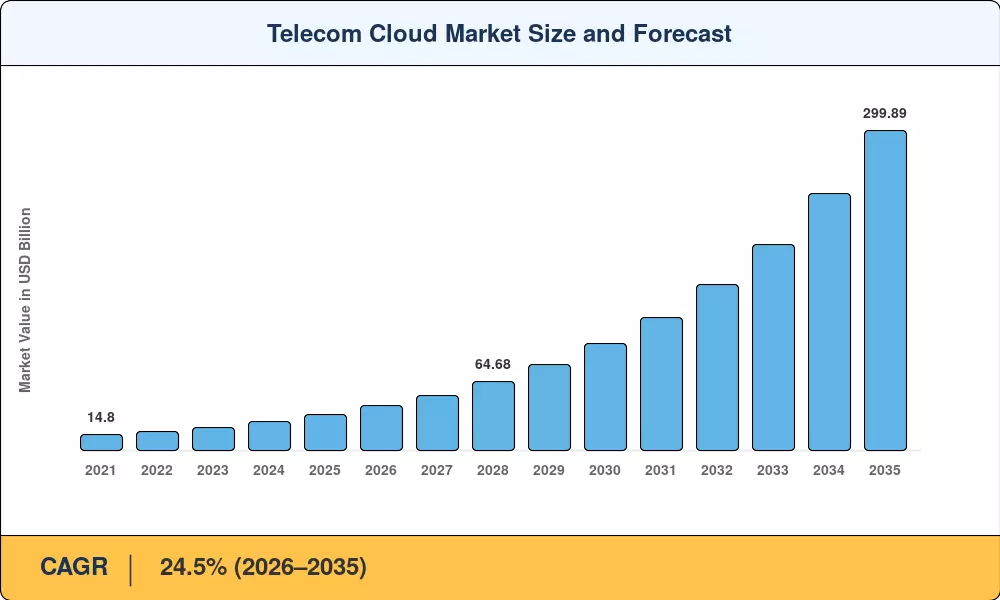

通信クラウド市場は2025年に335億2,000万米ドルと評価され、2026年の417億3,000万米ドルから2035年までに2,998億9,000万米ドルに成長すると予測されており、予測期間(2026年から2035年)中に24.5%のCAGRを記録します。 5G スタンドアロン導入が加速し、エッジ コンピューティングのユースケースが急増する中、世界中の通信事業者が資本をクラウドネイティブ ネットワーク コアに向けています。 AT&Tの140億ドルオープンRANエリクソンとの合意は、インフラレベルでテレコムクラウド市場を再形成する資本集中を示唆している[1].

独自のハードウェア スタックを中心に構築された従来のモノリシック ネットワーク アーキテクチャは、市販の既製サーバー上で実行されるソフトウェア定義のコンテナ化されたプラットフォームに取って代わられています。 Vodafone と Microsoft との 15 億米ドルのマルチクラウド パートナーシップは、通信事業者がコアとエッジのワークロードを再プラットフォーム化し、パフォーマンス、主権、コンプライアンスの義務を同時に満たす方法を示しています。[2]。この移行により、運用支出サイクルが数年から数か月に圧縮され、通信事業者はソフトウェアのスピードで新たな収益を生み出すサービスを開始できるようになります。

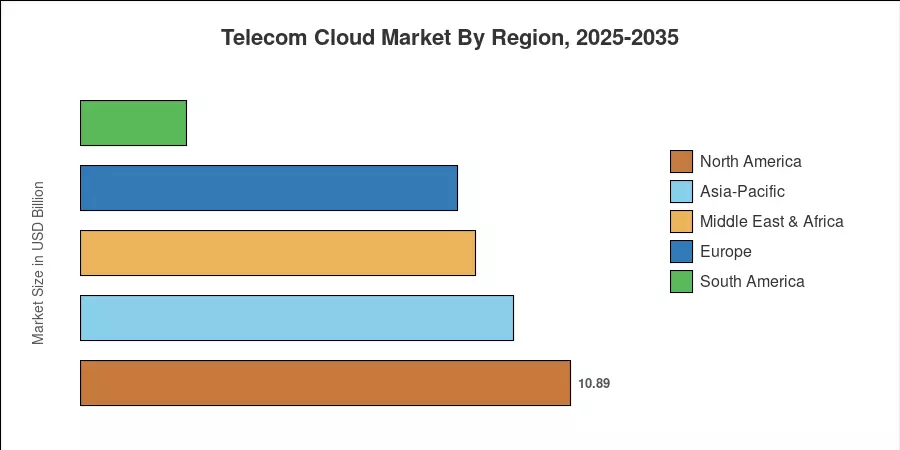

北米は通信クラウド市場の収益の約 32.5% を占めており、これはハイパースケーラーの近接性と初期段階に支えられています。5Gコア移住。アジア太平洋地域は、インドの Jio 規模の投資と中国の国家支援によるクラウドネイティブ展開によって推進され、CAGR 28.7% で最も急成長している地域です。ヨーロッパは、EU のデジタル 10 年の目標と複数の国内通信事業者にわたるオープン RAN パイロットによって推進され、25.0% 近くで 2 番目に大きなシェアを保持しています。[3]。通信事業者がネットワーク機能をクラウドネイティブのマイクロサービスに変換することで、通信クラウド市場は 2035 年まで接続経済を再構築する態勢が整っています。

レポートの重要なポイント

• ソリューションの種類別

- ソリューション製品は、Tier 1 通信事業者の間でのターンキーのクラウドネイティブ ネットワーク プラットフォームに対する需要を反映して、2025 年のテレコム クラウド市場収益の 48.9% を獲得しました。

- 管理された移行、統合、最適化の取り組みが拡大するにつれて、サービスは 2035 年まで 29.2% の CAGR で拡大すると予測されています。

• プラットフォーム別

- サービスとしてのインフラストラクチャは、仮想化されたネットワーク機能のためのコンピューティングとストレージのアウトソーシングによって支えられ、2025 年のテレコム クラウド市場シェアの 45.4% を占めました。

- Platform-as-a-Service は、通信アプリケーション開発用の DevOps ツールチェーンによって促進され、2035 年まで 30.4% の CAGR で上昇すると予測されています。

• アプリケーション別

- 請求とプロビジョニングは、2025 年の通信クラウド市場の 41.5% を占めており、ほとんどの通信事業者がクラウドに移行する最初のワークロードです。

- リアルタイム分析の需要が高まる中、トラフィック管理は 2035 年までに 29.8% の CAGR を達成する予定です。

• エンドユーザーによる

- BFSI は、低レイテンシの取引と安全な接続のニーズに牽引され、2025 年のテレコム クラウド市場シェアの 34.4% を占めました。

- ヘルスケアは、2035 年まで 26.1% の CAGR で最速のエンドユーザー拡大を示しています。

• 地域別

- 2025 年の通信クラウド市場収益の 32.5% を北米が占めました。

- アジア太平洋地域は、2026 年から 2035 年にかけて 28.7% の CAGR で成長すると予測されています。

市場規模と予測 (2021 ~ 2035 年)

Market Research Future の推定値は、通信会社の CIO および CTO への一次インタビュー、通信事業者の設備投資の開示、ハイパースケーラーの収益の内訳を組み合わせて導き出され、サードパーティのベンチマークと比較して検証されています。過去の数字は実際に報告された支出を反映しています。予測値には、マクロ経済サイクルを調整して調整された 24.5% CAGR が適用されます。

.webp?v=1785876044)