Acute Wound Care Market Summary

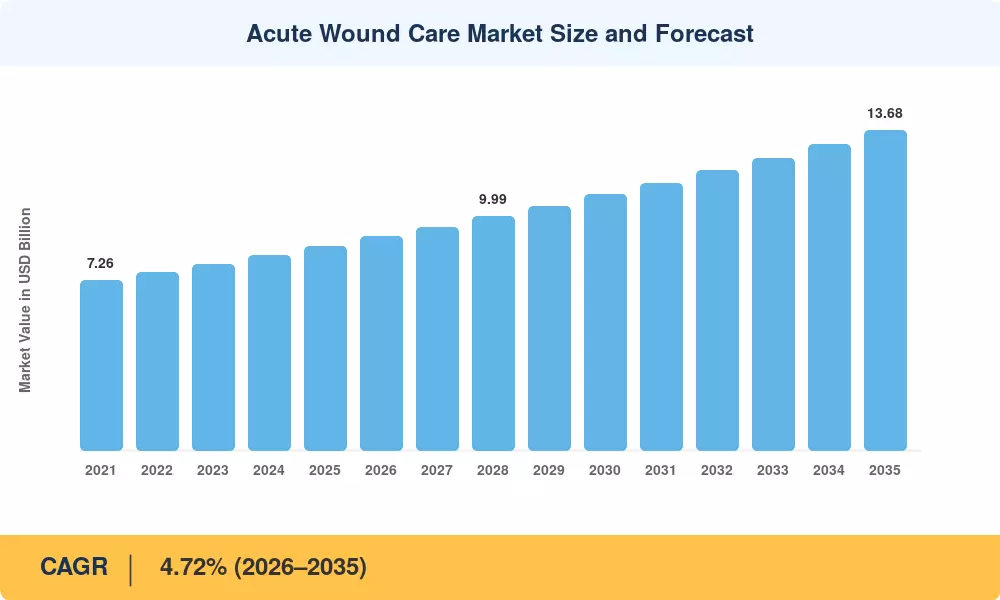

The acute wound care market reached an estimated USD 8.73 billion in 2025 and is projected to grow from USD 9.14 billion in 2026 to USD 13.68 billion by 2035, registering a CAGR of 4.72% during 2026–2035. This expansion is anchored in rising global surgical volumes — the WHO recorded over 310 million major procedures annually as of 2024 — and the growing adoption of closed-incision negative pressure wound therapy across ambulatory surgical centers [2]. Government reimbursement reforms in the United States and the European Union now incentivize home-based wound follow-up, shifting demand patterns and creating new revenue pools for wound healing dressings manufacturers.

The acute wound care market is undergoing a technical change as classic gauze-and-tape regimens are replaced by hybrid wound healing dressings that combine antibacterial wound therapy with suction-based exudate control. The U.S. Centers for Medicare & Medicaid Services (CMS) paid more than USD 1.2 billion for bundled payment modifications for management of post-surgical wounds in FY 2024, which is driving the adoption of advanced skin tissue regeneration platforms by hospitals [3]. Manufacturers are making significant investments in silver-ion and polyhexamethylene biguanide (PHMB) formulations that cut bioburden and enable quicker debridement methods at the point of treatment.

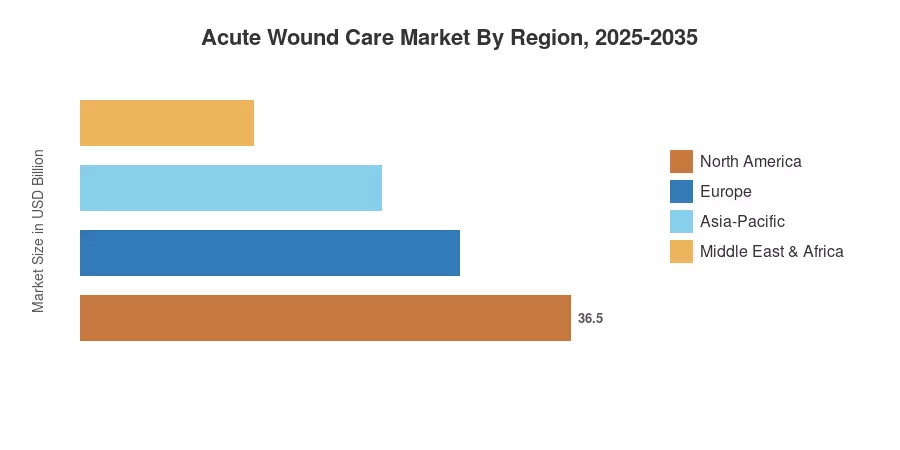

North America accounted for the largest share of the acute wound care market owing to high procedure volume and favorable insurance coverage. Asia-Pacific is the fastest-growing area, with a predicted CAGR of 6.52%, driven by the developing hospital infrastructure in India and China. Europe is the second biggest market share with about 28%. The increasing EU MDR evidence requirements are forcing producers towards clinically proven wound healing dressings The next decade will reward companies that bring innovative antimicrobial wound care and scalable digital health platforms for remote patient monitoring together.

Key Report Takeaways

• By Product Type

- Advanced wound care captured approximately 47% of the acute wound care market in 2025, reflecting strong clinician preference for foam, hydrocolloid, and alginate-based wound healing dressings over traditional products

- Surgical wound care is positioned as the fastest-expanding product category, projected at a 6.08% CAGR through 2035, driven by rising elective procedure volumes and adoption of antimicrobial wound therapy in operating theaters

• By Wound Type

- Surgical and traumatic wounds accounted for USD 5.88 billion in 2025, reflecting their dominance in acute care settings where debridement techniques and rapid closure are critical

- Burn treatment is forecast to register the strongest CAGR of 5.78% through 2035, supported by rising incidence rates and specialized antimicrobial wound therapy protocols in burn centers

• By Region

- North America led the acute wound care market with a 41% revenue share in 2025, underpinned by Medicare reimbursement expansion for negative pressure wound therapy

- Asia-Pacific is projected to reach USD 2.18 billion by 2035, as government health spending in China and India broadens access to advanced wound healing dressings

Acute Wound Care Market Size and Forecast (2021–2035)

MARKET RESEARCH FUTURE’s market size is based on a combination of manufacturer revenue disclosures, hospital procurement databases, import-export trade data, and proprietary demand modeling calibrated to CMS claims records and EU MDR product registrations. Historical figures are based on reported sales, whereas projection values are based on a calibrated CAGR, adjusted for legislative and demographic inflection points.

.webp?v=1783335258)