Adaptive Security Market Summary

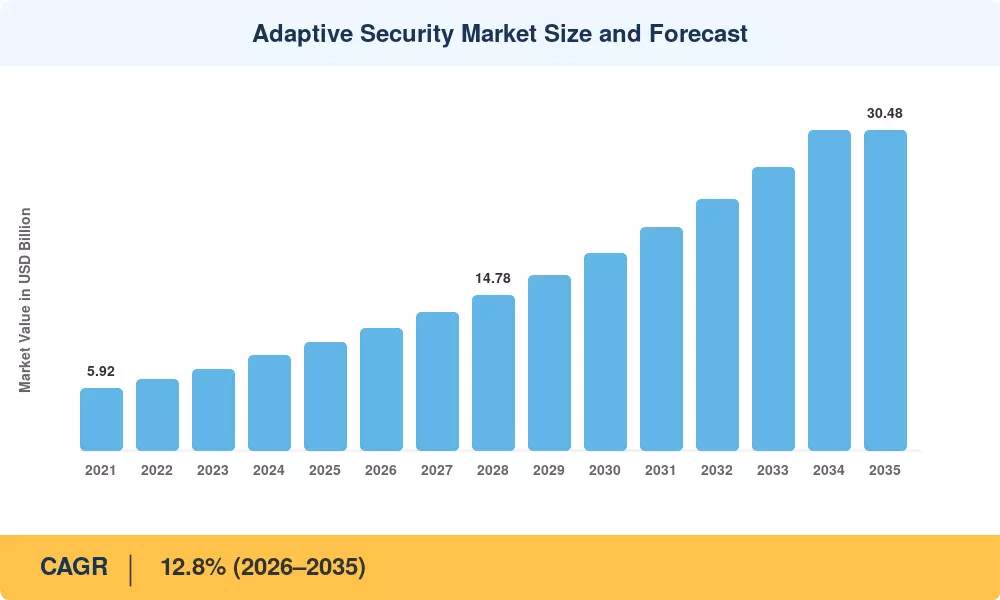

The global adaptive security market reached an estimated USD 10.30 billion in 2025 and is projected to grow from USD 11.62 billion in 2026 to USD 30.48 billion by 2035, registering a CAGR of 12.8% during the forecast period (2026–2035). This expansion is driven by a sharp escalation in sophisticated cyberattacks — ransomware losses alone exceeded USD 20 billion globally in 2024 [2] — and by regulatory mandates like the U.S. Executive Order 14028 on zero-trust architecture and the EU's NIS2 Directive, both of which compel enterprises to replace static perimeter defenses with AI-driven continuous security risk assessment frameworks [3].

The technology shift at the core of this market is decisive. Legacy rule-based firewalls and signature-dependent intrusion detection systems are giving way to zero-trust adaptive security architecture platforms that continuously evaluate risk posture across users, devices, and workloads. Estimates that by 2026, over 60% of enterprises will have adopted at least one form of continuous adaptive risk and trust assessment (CARTA), up from roughly 25% in 2022. Global cybersecurity spending surpassed USD 188 billion in 2024, and a growing slice of that budget — nearly 14% — now flows toward adaptive and behavior-analytics platforms [5].

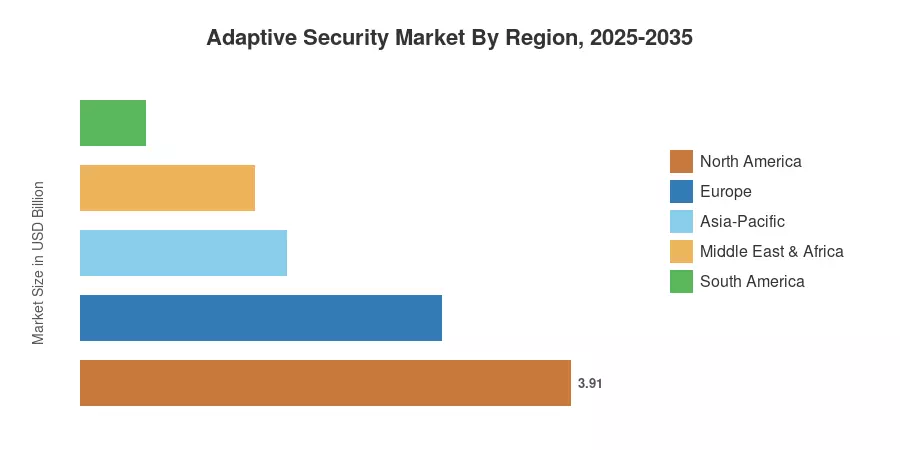

North America commands approximately 38% of global market revenue, anchored by heavy federal cybersecurity spending and a dense ecosystem of security vendors headquartered in the region Asia-Pacific is the fastest-growing region at a projected CAGR of roughly 15.9%, fueled by rapid digital transformation across India, China, and Southeast Asia. Europe holds the second-largest share at around 28%, propelled by GDPR enforcement costs and the NIS2 compliance wave. As self-healing security systems for enterprises mature and real-time threat intelligence for adaptive defense becomes table stakes, the adaptive security market is entering its most transformative decade.

Key Report Takeaways

• By Technology

- Zero-trust adaptive security architecture platforms captured the largest technology share in 2025, accounting for approximately 34% of total market revenue

- AI-driven continuous security risk assessment solutions are the fastest-growing technology segment, projected to expand at a CAGR of roughly 15.4% through 2035

- Dynamic access control based on user behavior solutions reached an estimated USD 1.85 billion in 2025

• By Sector

- The BFSI vertical dominates end-user demand with approximately 26% market share, driven by regulatory compliance and transaction-volume growth

- Healthcare is projected to grow at a CAGR of ~14.6%, the fastest among verticals, as connected medical devices proliferate

• By Geography

- North America generated roughly USD 3.91 billion in 2025, maintaining its lead through sustained federal and private-sector cybersecurity investment

- Asia-Pacific is forecast to nearly quadruple its market value between 2025 and 2035, driven by digital-economy initiatives across emerging economies

- Europe accounted for about 28% of the global market in 2025, with the NIS2 Directive accelerating procurement cycles

Market Size and Forecast (2021–2035)

MRFR's market-sizing model triangulates primary interviews with CISOs and IT procurement leaders, vendor revenue disclosures, and secondary data from industry bodies including NIST, ENISA, and the Cybersecurity & Infrastructure Security Agency (CISA). Historical figures (2021–2024) are validated against public filings and third-party analyst benchmarks; forecast projections (2026–2035) apply a bottom-up build from segment-level adoption curves calibrated to macroeconomic and threat-landscape variables.