Adhesives Sealants Handheld Devices Market Summary

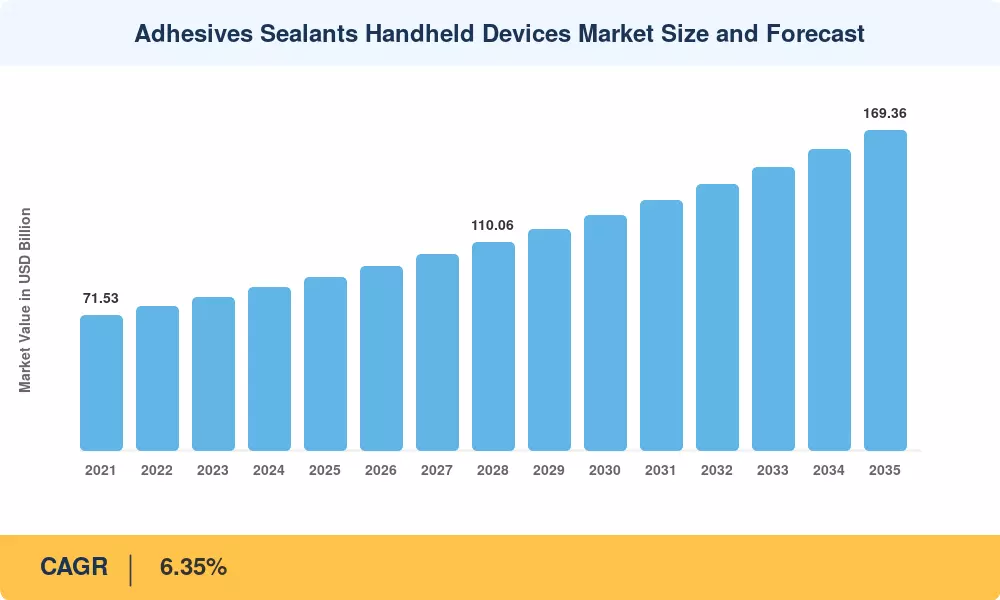

The Adhesives & Sealants Market reached an estimated USD 91.50 billion in 2025 and is projected to grow from USD 97.31 Billion in 2026 to USD 169.36 billion by 2035, registering a CAGR of 6.35% during the forecast period. Two forces anchor this trajectory: the EU Green Deal's mandate for low-VOC formulations across industrial applications, and a global wave of infrastructure spending exceeding USD 3.2 trillion through 2030 that is pulling bonding and sealing demand sharply upward [1]. Packaging automation for e-commerce fulfillment centers and the vehicle light-weighting push under CAFE and Euro 7 emission standards continue to expand addressable volumes across both adhesive and sealant categories.

The market for adhesives and sealants is fundamentally changing due to a shift in technology. Once predominant in industrial assembly, solvent-borne formulations are gradually being replaced by water-based and reactive chemistries that provide reduced emissions, quicker cure times, and better bond endurance. Major producers pledged to invest more than USD 4.8 billion in UV-cure production lines and bio-based feedstock facilities between 2023 and 2025 alone [2]. This change is being accelerated by regulatory pressure under the Toxic Substances Control Act and REACH, which is turning compliance from a cost burden into a competitive differentiator.

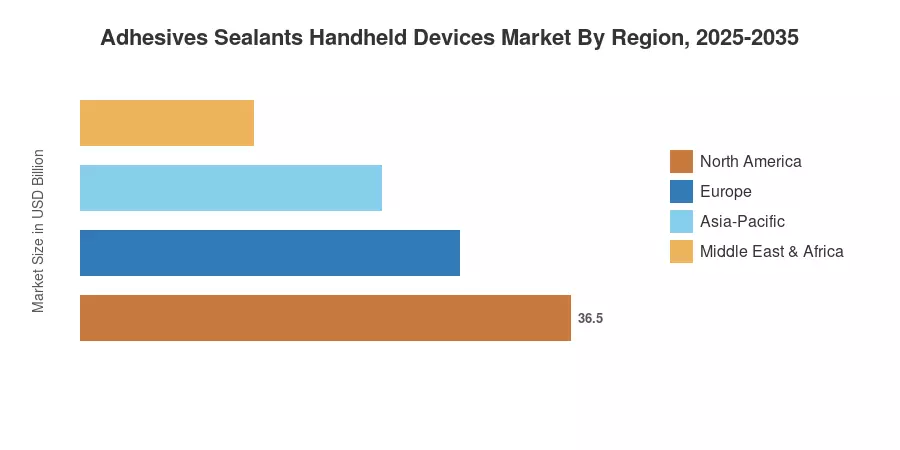

With 39.3% of 2025 revenue, Asia-Pacific holds the greatest share of the Adhesives & Sealants Market thanks to strong electronics manufacturing in ASEAN and infrastructure growth in China and India. Additionally, the region is expanding at the greatest rate, with a 6.90% CAGR until 2035. Thanks to reshoring trends in defense procurement and automobile production, North America now maintains a 24.8% stake. The adoption of sustainable adhesive chemistries is dominated by Germany and France, accounting for 22.4% of the European market. The market for adhesives and sealants stands to gain from the quick replacement of mechanical fasteners and welding in a variety of end-use industries as worldwide decarbonization targets tighten.

Key Report Takeaways

• By Adhesive Resin

- Acrylics accounted for 25.1% of the Adhesives & Sealants Market in 2025, led by demand in pressure-sensitive tape and label applications.

- Silicone resins are poised to expand at an 8.82% CAGR through 2035, the fastest among resin types, driven by electronics and high-temperature industrial uses.

- Polyurethane adhesives generated approximately USD 16.2 billion in 2025 revenue, reflecting strong uptake in automotive structural bonding.

• By Technology

- Water-based solutions captured 38.8% revenue share in 2025, supported by regulatory preference for low-emission chemistries.

- Reactive systems are forecast to post the fastest technology-segment CAGR of 8.58% over 2026–2035, favored for structural and high-performance assemblies.

• By End-User Industry

- Packaging led the Adhesives & Sealants Market with 45.2% share in 2025, propelled by e-commerce logistics and flexible packaging growth.

- Building and construction is projected to grow at a 6.78% CAGR through 2035, supported by modular construction and green building codes.

• By Region

- Asia-Pacific commanded 39.3% of the Adhesives & Sealants Market share in 2025, with China contributing the single largest country-level demand pool.

- North America represented 24.8% share, anchored by reshoring investments and defense manufacturing.

Adhesives & Sealants Market Size and Forecast (2021–2035)

Market Research Future derives its sizing from a triangulated methodology combining bottom-up revenue aggregation across resin types, technology platforms, and end-user verticals with top-down validation against trade association production volumes and customs data. Historical estimates (2021–2024) reflect actual shipment data from producer filings; the base year (2025) integrates interim results and channel checks. Forecast values (2026–2035) apply a calibrated CAGR of 6.35%, consistent with macroeconomic growth assumptions from the IMF and sector-specific demand models.