Aerial Imaging Market Summary

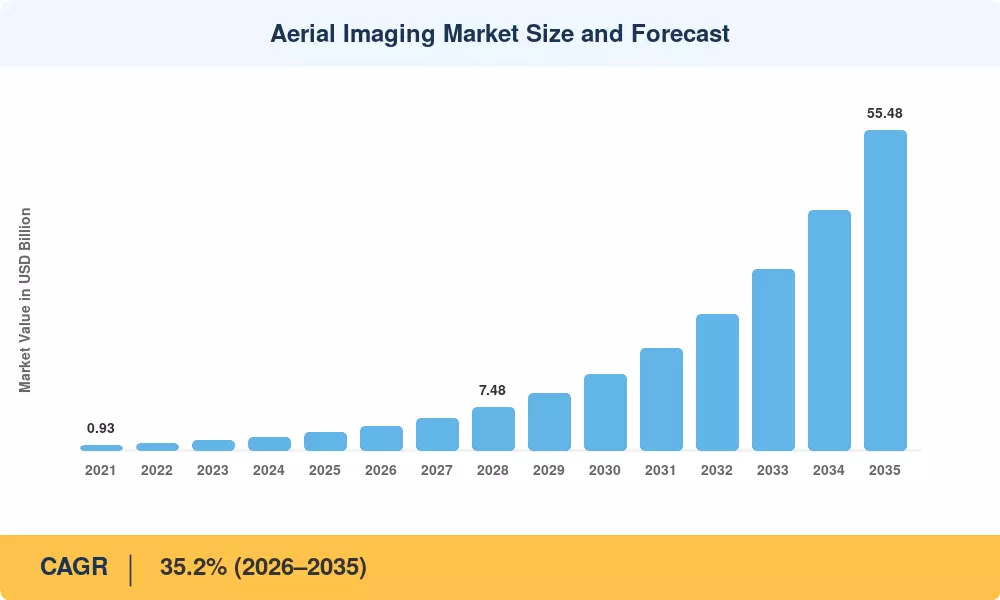

The Aerial Imaging Market stood at USD 2.76 billion in 2025 and is projected to reach USD 4.22 billion in 2026 before climbing to USD 55.48 billion by 2035, reflecting a 35.2% CAGR across the 2026–2035 forecast window. Government digital-twin mandates, including the US Infrastructure Investment and Jobs Act's USD 1.2 billion allocation for geospatial modernization, and aggressive energy-sector inspection budgets are the twin catalysts anchoring this trajectory [2][3]. The Aerial Imaging Market is rewriting how industries collect spatial intelligence at scale.

Legacy manned aerial survey fleets, once the backbone of orthomosaic aerial mapping, are rapidly giving way to hybrid-VTOL platforms equipped with on-device AI chips and real-time 5G streaming. High-resolution aerial survey workflows that previously required 72-hour processing turnarounds now complete in under four hours, a shift underscored by the European Space Agency's EUR 340 million Earth Observation Envelope Program investing heavily in sub-decimetre geodata standards [4]. Aerial photogrammetry software vendors have responded by embedding edge-AI inference directly into flight controllers, collapsing the data-to-decision pipeline.

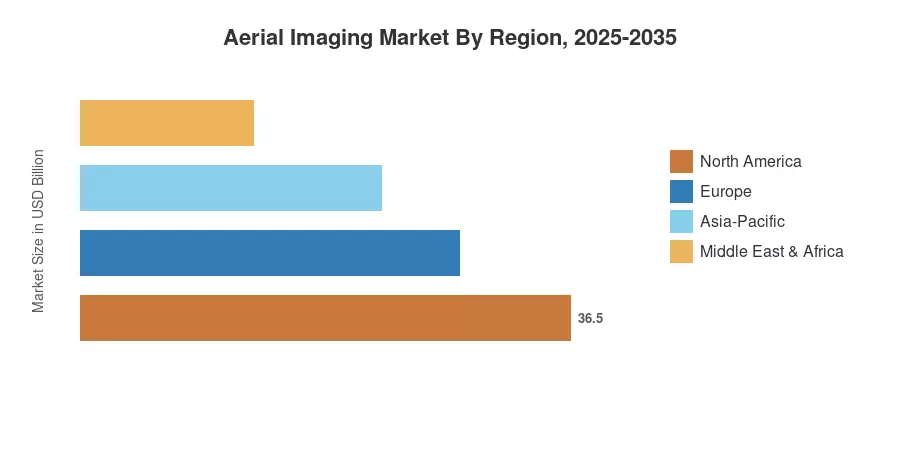

North America commands roughly 36% of the Aerial Imaging Market, driven by FAA Part 107 waiver expansions and utility corridor inspection demand. Asia-Pacific is the fastest-growing region at a projected 37.1% CAGR, fueled by India's SVAMITVA drone-mapping program and China's smart-city sensor mandates. Europe holds the second-largest share, near 27%, anchored by EU Digital Twin initiatives and offshore wind farm thermal aerial imaging inspection requirements The decade ahead will reward operators who pair platform versatility with analytics depth.

Key Report Takeaways

• By Platform

- UAVs and drones captured 52.1% of the Aerial Imaging Market revenue in 2025, reinforcing their dominance in aerial photography drone services and short-range survey missions

- LiDAR-based imaging techniques are forecast to grow at a 36.2% CAGR through 2035, overtaking vertical imaging's incumbent position as canopy-penetration and 3D point-cloud demand accelerate

- Hybrid-VTOL platforms are the fastest-growing sub-segment, driven by declining airframe costs and certifications enabling 80+ km survey missions that previously required manned fixed-wing aircraft.

• By Imaging Technology

- LiDAR-based imaging techniques are forecast to grow at a 36.2% CAGR through 2035, overtaking vertical imaging's incumbent position as canopy-penetration and 3D point-cloud demand accelerate

• By Delivery Mode

- Subscription libraries accounted for 57.3% of the Aerial Imaging Market in 2025, while on-demand tasking is expanding at a 36.8% CAGR as project-based procurement gains favor

- Geospatial mapping and land survey held 34.0% of 2025 revenue, yet disaster and emergency management is advancing fastest at a 36.6% CAGR

• By Application

- Geospatial mapping and land survey held 34.0% of 2025 revenue, yet disaster and emergency management is advancing fastest at a 36.6% CAGR

• By Region

- North America retained the largest regional share at approximately 36%, supported by federal infrastructure spending and utility-sector mandates

- Asia-Pacific is forecast to register a 37.1% CAGR, propelled by national drone-mapping campaigns and smart-city investment across India, China, and South Korea

Market Size and Forecast (2021–2035)

The figures below combine MRFR primary surveys of over 120 aerial imaging operators, payload OEMs, and software vendors with secondary triangulation from public procurement databases, regulatory filings, and trade association data[5].

.webp?v=1782888034)