AI in Video Surveillance Market Summary

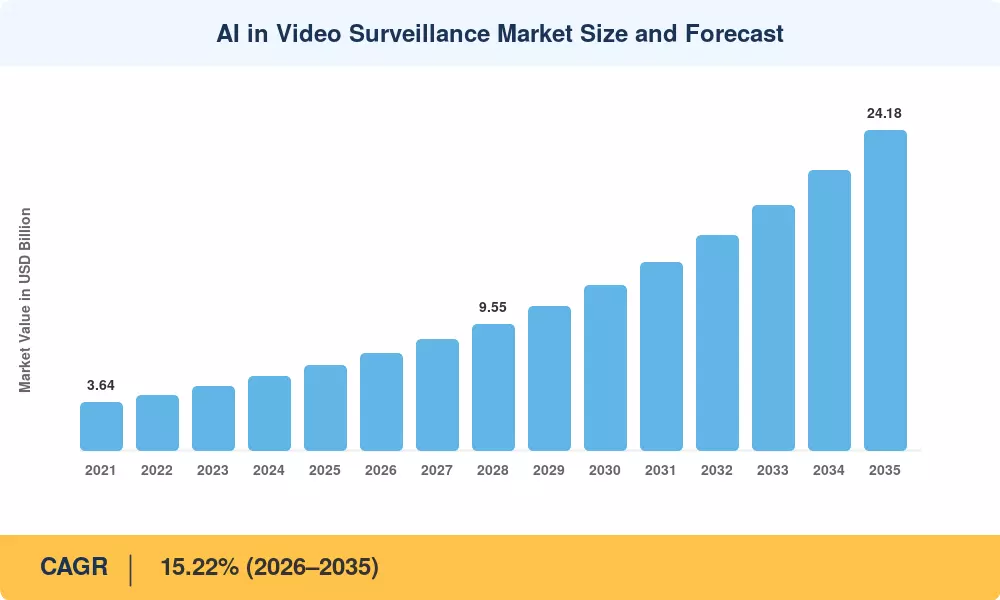

The AI in Video Surveillance Market stood at USD 6.41 billion in 2025 and is projected to reach USD 7.32 billion in 2026 before climbing to USD 24.18 billion by 2035, registering a CAGR of 15.22% during the forecast period. Government-led smart-city programs — India's Smart Cities Mission alone has earmarked over USD 7.5 billion across 100 cities [2] — and sweeping public-safety mandates in the U.S. and EU are injecting sustained capital into AI-powered CCTV systems and intelligent video analytics platforms.

A fundamental shift is underway as legacy analog and basic IP camera networks give way to deep learning video monitoring architectures capable of real-time object classification, anomaly detection, and predictive alerting. Edge-AI chipset costs have fallen roughly 40% since 2021 [3], making it economically viable to embed neural-network inference directly inside smart surveillance cameras. Cloud-based video-surveillance-as-a-service (VSaaS) subscriptions are further lowering the barrier, enabling mid-market retailers, logistics hubs, and municipal agencies to deploy facial recognition surveillance without heavy upfront infrastructure spend.

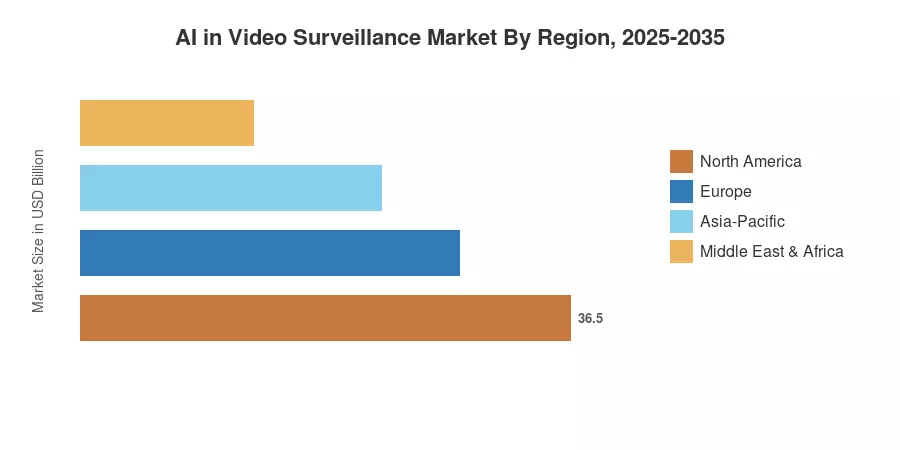

Asia-Pacific commands approximately 39.15% of global revenue in the AI in Video Surveillance Market, driven by China's Skynet and Sharp Eyes programs alongside Japan's pre-Olympic security investments [4]. The Middle East & Africa region is the fastest-growing geography at a projected 14.55% CAGR, fueled by mega-project construction in Saudi Arabia and the UAE. North America holds the second-largest share, near 28.5%, anchored by federal DHS grant programs and a mature commercial security ecosystem. These regional dynamics point toward a market where intelligent video analytics will become standard infrastructure rather than a premium add-on within the next decade.

Key Report Takeaways

• By Component

- Hardware retained 60.10% of the AI in Video Surveillance Market share in 2025, led by AI-enabled camera modules and edge processors

- Software is forecast to expand at a 19.15% CAGR through 2035 as deep learning video monitoring analytics overtake basic motion detection

• By Deployment Model

- On-premises systems held 68.75% revenue share in 2025, preferred by military, defense, and critical-infrastructure operators requiring data sovereignty

- Cloud-deployed solutions within the AI in Video Surveillance Market are projected to grow at a 23.65% CAGR, propelled by VSaaS subscription economics

• By End-User & Application

- Commercial facilities led with USD 2.82 billion in 2025, with retail loss-prevention and smart-building integration as primary drivers

- Facial recognition surveillance and biometric applications are forecast to advance at a 25.55% CAGR, the fastest application segment

• By Geography

- Asia-Pacific commanded 39.15% of the AI in Video Surveillance Market revenue in 2025, anchored by China's national surveillance programs

- The Middle East is expected to register the highest regional CAGR at 14.55% through 2035

Market Size and Forecast (2021–2035)

MRFR's sizing methodology triangulates vendor-reported revenues, national procurement databases, and bottom-up installation counts across 45 countries, cross-validated against import/export data for AI-powered CCTV systems and intelligent video analytics software licenses.

.webp?v=1783335277)