Air Traffic Control Equipment Market Summary

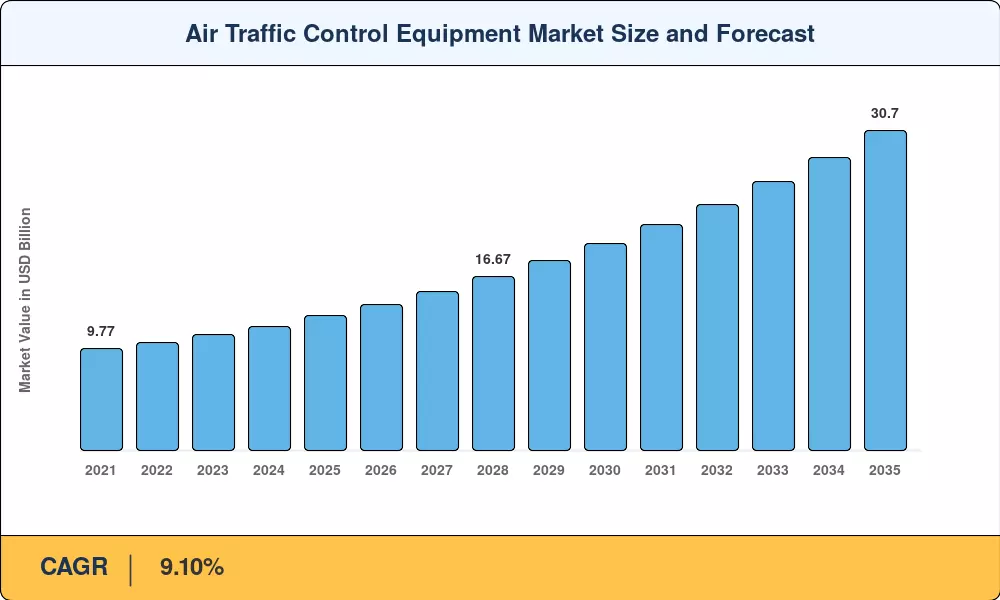

The Air Traffic Control Equipment Market was valued at USD 12.93 billion in 2025 and is projected to grow from USD 14.01 billion in 2026 to USD 30.70 billion by 2035, registering a CAGR of 9.10% during the forecast period (2026–2035). This expansion is anchored in large-scale government modernization programs that aim to replace legacy infrastructure with digital, software-defined systems. The FAA's commitment of roughly USD 16 billion toward next-generation airspace networks in the United States has set a benchmark, and parallel programs across the European Union, India, and China are intensifying capital flows into the Air Traffic Control Equipment Market at an unprecedented pace [1][2].

We are at a technology inflection point that is changing the sector. Remote digital towers, satellite-based navigation overlays and AI-assisted conflict-detection engines are replacing legacy analog radar consoles and voice-oriented communications stacks. One Airspace is India’s attempt to merge civil and military management into one digital backbone, and China’s 14th Five-Year Plan funnels more funds toward advanced automation and flight-data integration. Combined, these projects funnel billions into integrated monitoring platforms that enhance situational awareness and throughput capacity [3][4].

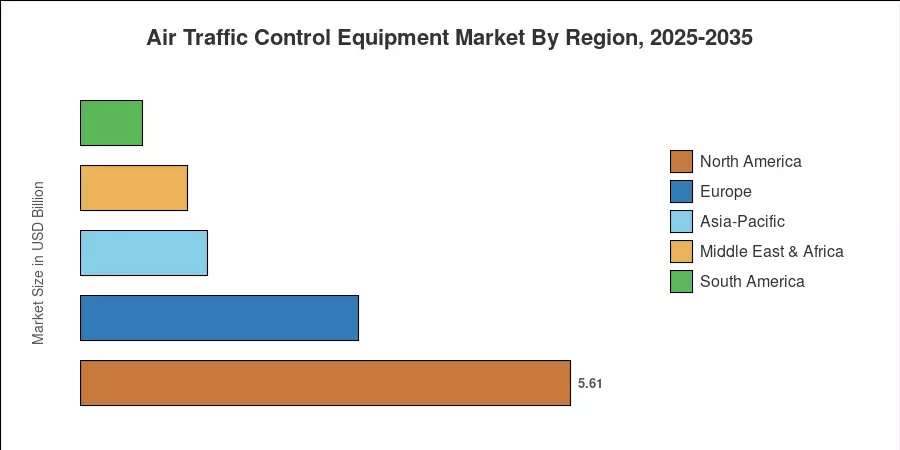

North America accounts for around 43.4% of the Air Traffic Control Equipment Market, due to the region’s heavy traffic loads and the continuous spending on NextGen. The Asia-Pacific region is the fastest-growing region with a CAGR of 11.20% throughout the forecast period till 2035 due to the airport construction pipeline in India, China and Southeast Asia. Europe contributes 24.6% of 2025 revenue and takes second place, fueled by the SESAR program and Single European Sky mandates. These three power centers will push the Air Traffic Control Equipment Market towards a fully digital, data-rich operational paradigm in the next decade.

Key Report Takeaways

• By Equipment Type

- Communication equipment captured approximately 45.5% of the Air Traffic Control Equipment Market share in 2025, driven by VHF data-link and controller-pilot data-link upgrades across major hubs.

- Remote and digital tower modules are projected to register the fastest equipment-type CAGR of 11.80% through 2035, as low-traffic airports adopt camera-sensor solutions to replace physical towers.

• By End User

- Commercial aviation accounted for roughly 71.3% of the Air Traffic Control Equipment Market in 2025, underpinned by fleet expansion and air-passenger traffic recovery.

- Military end-user spending is forecast to grow at a 10.50% CAGR through 2035, reflecting defense-grade ADS-B and multilateration demand.

• By Geography

- North America held 43.4% of the 2025 Air Traffic Control Equipment Market revenue, led by FAA NextGen procurement cycles.

- Asia-Pacific is forecast to log the highest regional CAGR of 11.20% through 2035, supported by greenfield airport construction in India and China.

Market Size and Forecast (2021–2035)

The projections below were developed using Market Research Future (MRFR)’s proprietary sizing framework that triangulates bottom-up OEM shipment data, top-down government procurement disclosures and confirmed ANSP budget submissions. Historical data are based on actual releases, and predicted values are based on a calibrated compound growth model.