Aircraft Heat Exchanger Market Summary

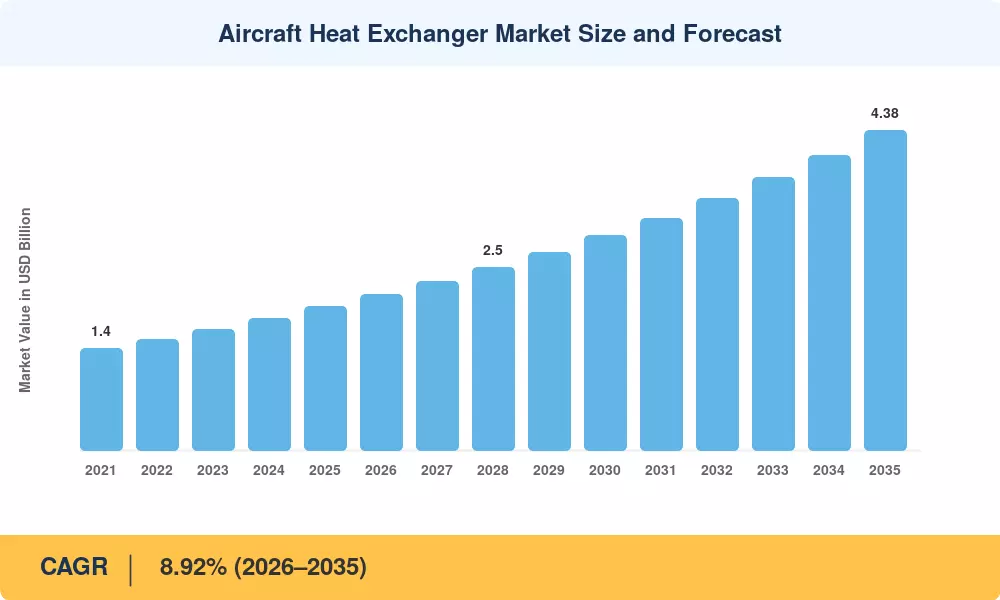

The aircraft heat exchanger market was valued at USD 1.97 billion in 2025 and is projected to reach USD 2.19 billion in 2026 before climbing to USD 4.38 billion by 2035, registering a CAGR of 8.92% during the 2026–2035 forecast window. Two catalysts anchor this trajectory: the global push to normalize widebody and narrowbody production after pandemic-era backlogs, and ICAO's 2024 resolution mandating net-zero aviation emissions by 2050, which has accelerated investment in next-generation aviation thermal management systems across OEM and aftermarket channels[2].

There is a technology inflection going on. The legacy brazed-aluminum cores that have been the workhorse of cabin environmental management for decades are being displaced by additively created microchannel shapes and topology-optimized plate-fin designs. For example, Boeing’s investment of USD 450 million in 2024 in enhanced thermal architecture for electrified subsystems is an example of how fuel-cooled aircraft heat exchangers and avionics cooling plate heat exchangers are moving from commodity hardware to performance-critical enablers [3]. Additive manufacturing enables engineers to pack 30-40% more heat-rejection surface into the same envelope, shaving drag penalties and enabling the megawatt-scale thermal loads of hybrid-electric powertrains.

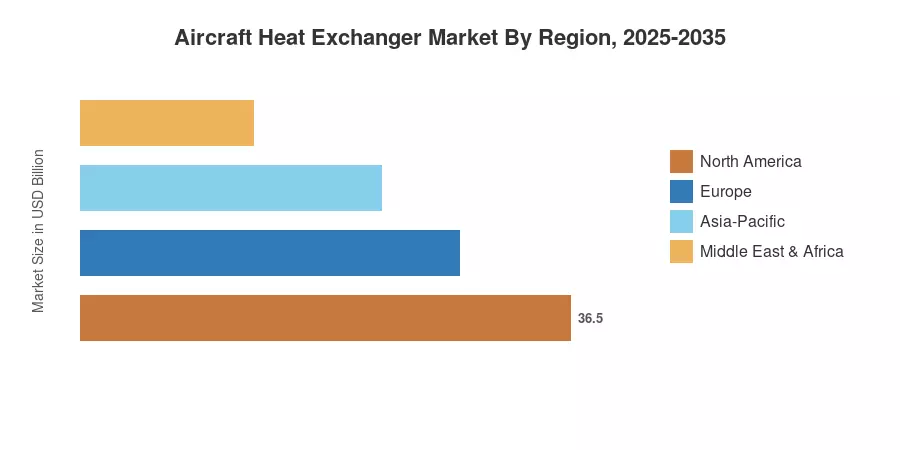

North America holds around 42% share of the aviation heat exchanger market revenue, backed by US defense procurement and the presence of tier-one OEM plants in the region. North America is also the fastest rising region, with a 9.87% CAGR through 2035, driven by F-35 sustainment investment and Part 25 retrofit obligations. Europe has the second-largest share of around 28%, supported by Airbus ramp-ups and Clean Aviation Joint Undertaking funding. The Asia-Pacific area is moving fast as India and China are ramping up indigenous fighter and regional-jet programs, making the aircraft heat exchangers industry an internationally competitive battleground throughout the next decade[5].

Key Report Takeaways

• By Type

- Flat-tube heat exchangers captured the leading position in the aircraft heat exchanger market in 2025 with an estimated 68% share, supported by their superior pressure-drop performance in narrowbody environmental control systems

- Plate-fin heat exchangers are advancing at a 9.52% CAGR through 2035, driven by demand for aircraft oil cooling heat exchangers in next-generation turbofan platforms

• By Platform

- Fixed-wing aircraft represented approximately 74% of the aircraft heat exchanger market in 2025, reflecting fleet size dominance in commercial and military aviation

- Unmanned aerial vehicles posted the fastest CAGR of 10.14% through 2035 as fuel-cell propulsion expands thermal loads beyond legacy design envelopes

• By Application

- Engine systems retained a dominant share in 2025, reflecting the sheer volume of aircraft oil cooling heat exchanger units across turbofan fleets

- Environmental control systems are projected to grow at 9.41% CAGR through 2035, the fastest among applications, as cabin air-quality standards tighten globally

• By Region

- North America led the aircraft heat exchanger market in 2025 and registered the highest regional CAGR through 2035

- Asia-Pacific is forecast to reach USD 1.05 billion by 2035, propelled by indigenous aircraft manufacturing in China and India

Market Size and Forecast (2021–2035)

MRFR estimations are based on primary OEM interviews, aftermarket channel surveys, and fleet-level regression modeling using published order books. Historical data (2021-2024) is drawn from certified financial filings from Tier 1 suppliers, while forecast estimates are based on a calibrated CAGR, aligned to delivery timetables and electrification roadmaps.