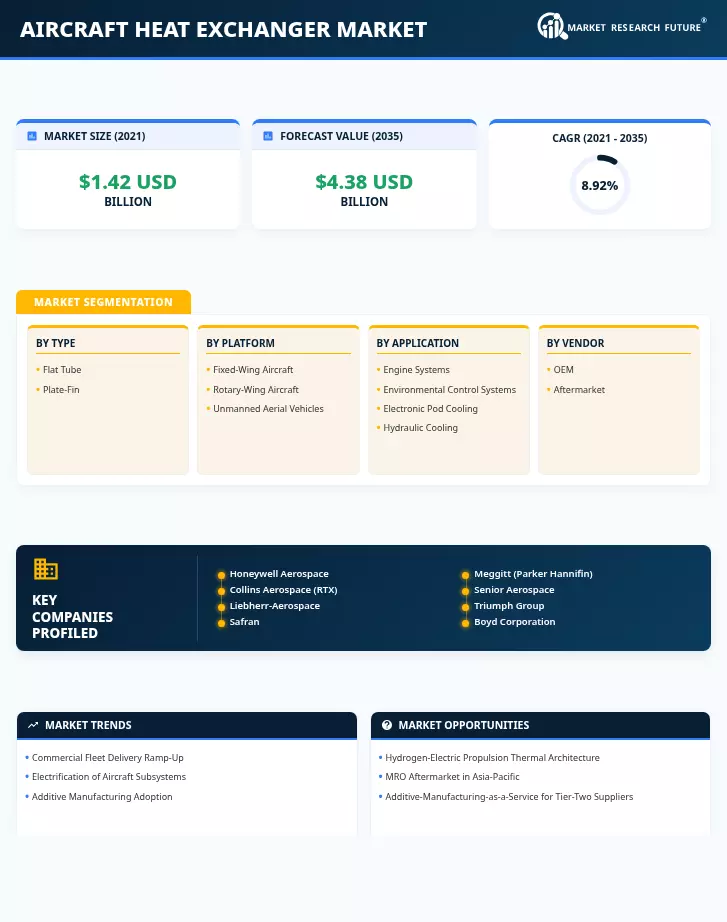

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Type | Flat Tube, Plate-Fin | Flat Tube | Plate-Fin |

| By Platform | Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Aerial Vehicles | Fixed-Wing Aircraft | Unmanned Aerial Vehicles |

| By Application | Engine Systems, Environmental Control Systems, Electronic Pod Cooling, Hydraulic Cooling | Engine Systems | Environmental Control Systems |

| By Vendor | OEM, Aftermarket | OEM | Aftermarket |

| By Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | North America |

Market Segmentation Overview

By Type

| Sub-Segment | Key Trend |

| Flat Tube | High-volume adoption in narrowbody ECS packs; mature manufacturing base |

| Plate-Fin | AM-enabled weight reduction; growing in engine oil-cooling applications |

Flat-tube heat exchangers remain the dominant type across commercial aviation due to their pressure-drop advantages and established supply chains. Plate-fin designs are gaining rapid traction as additive manufacturing unlocks topology-optimized geometries that reduce core weight by up to 30%, making them increasingly competitive for aircraft oil cooling heat exchanger and fuel-cooled aircraft heat exchanger applications.

By Platform

| Sub-Segment | Key Trend |

| Fixed-Wing Aircraft | Largest installed base; driven by narrowbody delivery surge |

| Rotary-Wing Aircraft | Steady demand from military and offshore utility helicopters |

| Unmanned Aerial Vehicles | Fastest growth driven by fuel-cell propulsion and HALE missions |

Fixed-wing aircraft generate the majority of demand due to the sheer scale of commercial and military jet fleets worldwide. UAVs are the fastest-growing platform as high-altitude long-endurance missions and fuel-cell-powered configurations push thermal-management requirements beyond legacy cooling approaches.

By Application

| Sub-Segment | Key Trend |

| Engine Systems | Core demand driver across turbofan and turboprop fleets |

| Environmental Control Systems | Fastest-growing application; driven by cabin air-quality regulation |

| Electronic Pod Cooling | Niche growth in fighter EW and radar thermal management |

| Hydraulic Cooling | Stable demand in rotary-wing and landing-gear subsystems |

Engine systems lead by revenue share because every aircraft powerplant requires dedicated oil and fuel thermal-management assemblies. Environmental control systems are growing fastest as EASA CS-25 amendments and FAA cabin air-quality directives create both OEM and retrofit demand.

By Vendor

| Sub-Segment | Key Trend |

| OEM | Revenue dominance tied to record aircraft order backlogs |

| Aftermarket | Fastest-growing channel as fleet aging and regulatory upgrades accelerate Aircraft Heat Exchanger Market demand. |

OEM sales reflect the backlog-driven production environment at Boeing and Airbus. At the same time, aftermarket growth is fueled by aging fleet retrofit cycles and expanding Aircraft Heat Exchanger Market capacity in Asia-Pacific and the Middle East.