Alarm Monitoring Market Summary

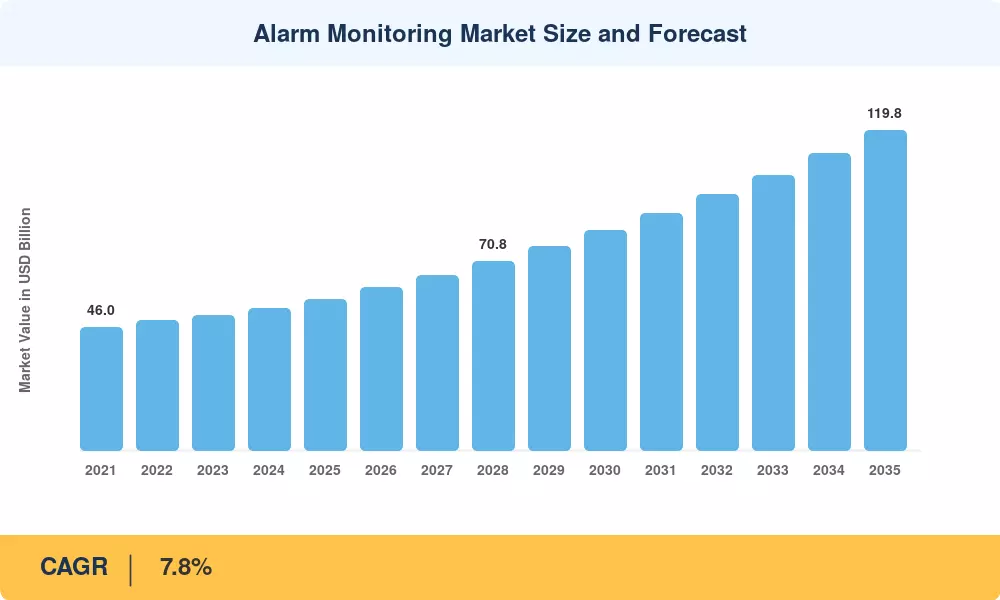

The global alarm monitoring market reached USD 56.5 billion in 2025 and is projected to climb to USD 60.9 billion in 2026, expanding to USD 119.8 billion by 2035 at a 7.8% CAGR through the forecast window. Two catalysts anchor the trajectory: the FCC's continued telephone-network modernization rules that are accelerating the sunset of copper PSTN lines used by legacy panels, and the rapid growth of insurance-linked monitoring discounts that now exceed USD 1.2 billion annually in premium reductions across North American carriers [1][2].

A structural technology pivot is reshaping how signals are received, verified, and dispatched. Cellular LTE-M, NB-IoT, and IP-based alarm transmission protocols that are compliant with the ANSI/SIA DC-09 and EN 50136 standards are replacing traditional dialer-based panels that rely on POTS lines [3]. Honeywell, Johnson Controls, and ADT have collectively allocated over USD 2.3 billion between 2023 and 2025 to platform modernization, AI verification engines, and central station automation, which are financing the transition.

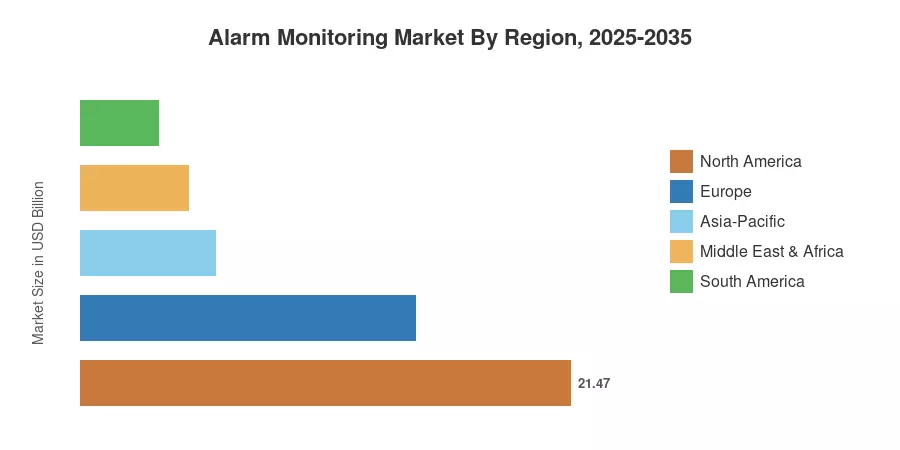

North America commands roughly 38% of global revenue on the strength of its mature monitoring ecosystem, while Asia-Pacific is expanding fastest at a 10.5% CAGR as urbanization and smart-city programs accelerate. Europe holds the second-largest position, driven by stringent grade-rated compliance under EN 50131. The market is consolidating around platform-native players that can verify events, suppress false alarms, and integrate with smart-home ecosystems.

Key Report Takeaways

• By Technology

- IP-based alarm transmission protocols expanding at a 12.4% CAGR through 2035 as PSTN networks retire

- Wireless/cellular monitoring accounts for the leading 41% share of the connectivity layer

- Video verification alarm monitoring services projected to reach USD 18.2 billion by 2035

• By Sector

- Commercial properties hold a 47% share of total monitored endpoints

- Residential monitoring expanding at a 9.1% CAGR, faster than the overall market

- Industrial and critical infrastructure segment estimated at USD 11.4 billion in 2025

• By Region

- North America: dominant region with ~38% revenue share

- Asia-Pacific: fastest-growing region at 10.5% CAGR

- Europe: second-largest contributor with USD 14.7 billion in 2025 revenue

Market Size and Forecast (2021–2035)

MRFR's forecast model triangulates company-disclosed monitoring account counts, central station signal volumes, and insurance industry reimbursement data, cross-validated with regulatory filings from UL-listed monitoring centers and EN 50518-certified Alarm Receiving Centers (ARCs) [6].