Ammonium Sulphate Market Summary

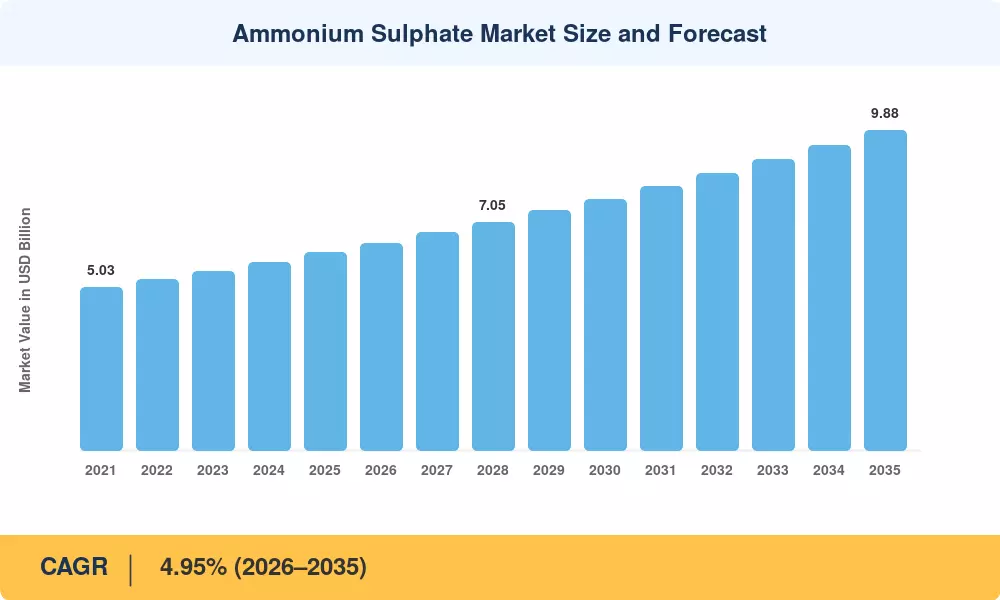

The Ammonium Sulfate Market was valued at USD 6.10 Billion in 2025, with the forecast period beginning at USD 6.40 Billion in 2026 and projected to reach USD 9.88 Billion by 2035, expanding at a CAGR of 4.95% during 2026–2035. Rising global food demand, coupled with government-backed fertilizer subsidy programs across India, Brazil, and Southeast Asia, has catalyzed sustained investment in nitrogen fertilizers and sulfate fertilizers. The Indian government's Nutrient-Based Subsidy (NBS) scheme allocated over USD 7.5 billion toward fertilizer support in 2024 alone, directly boosting procurement of agrochemical fertilizers, including ammonium sulfate [2].

A notable shift is underway in how farmers approach soil nutrient additives. Traditional urea-heavy regimes are being supplemented — and in some geographies replaced — by balanced crop nutrition chemicals that supply both nitrogen and sulfur in a single application. Water-soluble fertilizers and blended fertilizer-grade chemicals are gaining traction as precision agriculture platforms expand. The International Fertilizer Association (IFA) estimated that global sulfur fertilizer consumption crossed 7.8 million tonnes in 2024, up 4.2% year-over-year, reflecting stronger demand for dual-nutrient formulations [3].

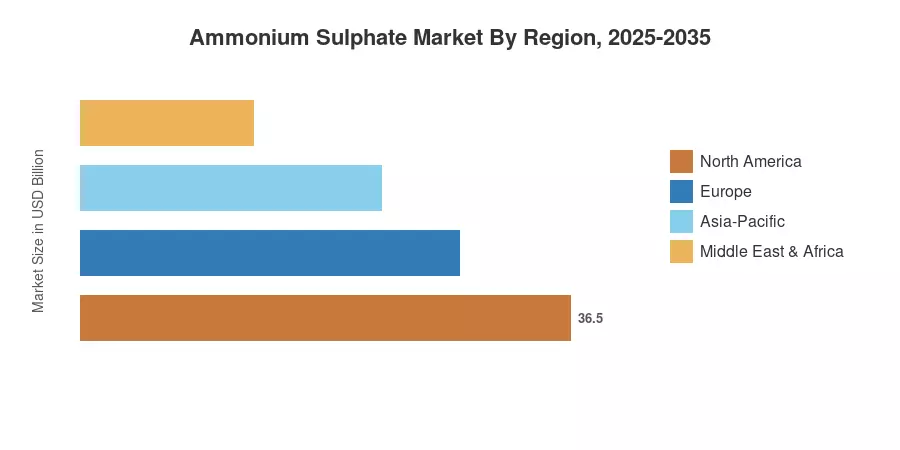

North America commands approximately 33% of the Ammonium Sulfate Market, anchored by corn-belt sulfur supplementation programs in the US Midwest Asia-Pacific represents the fastest-growing region, registering a forecast CAGR of 5.8%, propelled by agricultural intensification in India and China. Europe holds the second-largest share at roughly 24%, driven by EU Integrated Nutrient Management policies. The trajectory through 2035 points toward sustained mid-single-digit growth as sulfur-deficient soils and rising protein crop acreage keep demand firmly on an upward curve.

Key Report Takeaways

• By End-Use

- Solid ammonium sulfate accounts for approximately 72% of the Ammonium Sulfate Market, driven by granular and crystalline demand in broadacre farming

- Liquid ammonium sulfate is growing at a CAGR of 6.1% through 2035 as fertigation and foliar spray adoption accelerate among specialty crop growers

• By Application

- Fertilizer applications represent USD 5.19 Billion in 2025 value, reflecting ammonium sulfate's dominance as a nitrogen fertilizer input for row crops

- Food and Feed Additive usage is expanding at a 5.4% CAGR, supported by demand for food-grade sulfate fertilizers in protein enrichment and dough conditioning

- Pharmaceutical applications contribute approximately 4% of market share, serving as a protein precipitation agent in biopharma production

• By Region

- North America leads the Ammonium Sulfate Market at roughly 33% share, underpinned by corn and soybean sulfur deficiency management programs

- Asia-Pacific is the fastest-growing region, reaching a projected USD 3.12 billion by 2035 as soil nutrient additives demand surges

Market Size and Forecast (2021–2035)

The market size series below integrates bottom-up production and trade flow analysis with demand-side consumption modeling across 35 countries. Historical figures (2021–2024) derive from customs databases, producer shipment records, and FAO nutrient-balance statistics. Forecast values (2026–2035) apply a compound growth trajectory calibrated against macroeconomic agricultural output projections and policy-driven fertilizer procurement trends.