Animal Disinfectants Market Summary

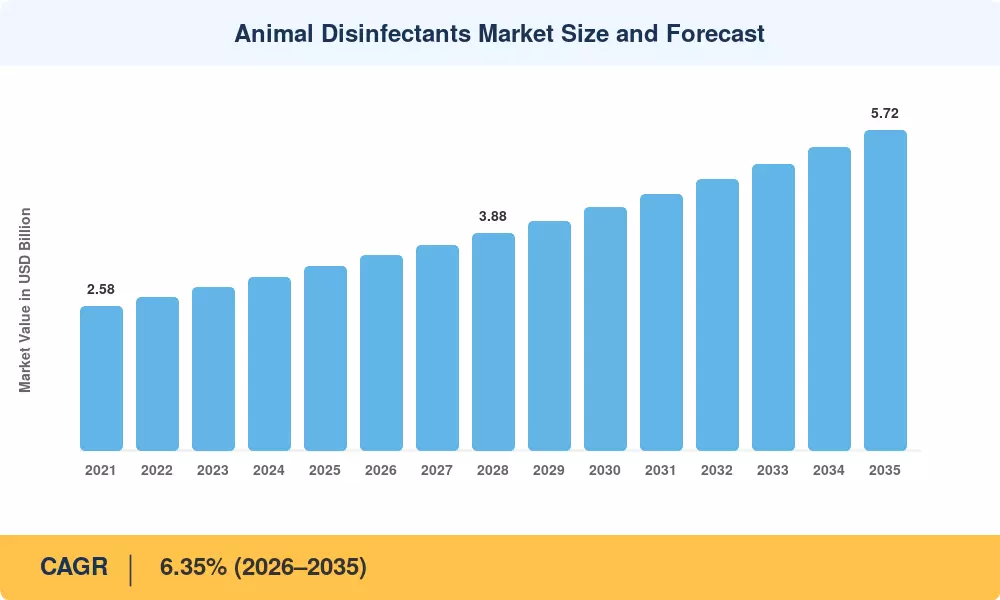

The Animal Disinfectants Market reached an estimated USD 3.29 billion in 2025 and is projected to climb from USD 3.50 billion in 2026 to USD 5.72 billion by 2035, registering a CAGR of 6.35% during the forecast period. Two forces anchor this trajectory: the European Union's accelerated phase-out of formaldehyde-based chemistries under REACH Regulation amendments [2] and a surge in government-backed livestock biosecurity programs across Southeast Asia, where avian influenza outbreaks triggered over USD 1.2 billion in emergency veterinary sanitation products procurement between 2022 and 2024 [3].

A technological shift is reshaping the Animal Disinfectants Market from manual spray-and-pray routines toward precision dosing and sensor-enabled dispensing platforms. Legacy chlorine-based dipping systems — the backbone of farm animal hygiene for decades — are giving way to automated fogging units and IoT-connected barn and stable sanitizers that cut chemical consumption by 20–30% while maintaining pathogen kill rates above 99.9% [4]. The EU's Horizon Europe program has earmarked EUR 180 million through 2027 for sustainable poultry disinfection solutions and antimicrobial stewardship research [5].

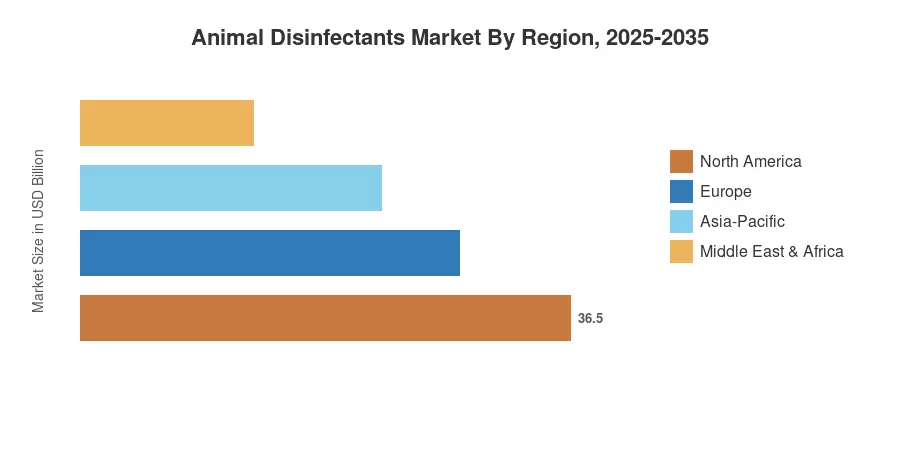

Europe commanded approximately 35% of the Animal Disinfectants Market in 2024, driven by strict livestock biosecurity mandates and early adoption of next-generation veterinary sanitation products. Asia-Pacific is the fastest-growing region at a projected CAGR of 7.95%, fueled by mega-farm expansion in China, India, and Vietnam. North America accounted for roughly 27% of global revenue, underpinned by USDA biosecurity modernization directives [6]. The decade ahead will reward suppliers who can pair chemical efficacy with digital traceability — a convergence that is redefining competitive advantage across the Animal Disinfectants Market.

Key Report Takeaways

• By Product Type

- Iodine compounds led the Animal Disinfectants Market in 2024 with approximately 31% revenue share, driven by broad-spectrum efficacy in dairy and poultry disinfection solutions environments

- Peracetic acid is set to expand at a 9.7% CAGR through 2035, propelled by zero-residue mandates in organic farm animal hygiene protocols

- Chlorine-based products accounted for USD 0.58 billion in 2024, though regulatory headwinds are compressing growth

• By Form

- Liquid formulations held 67% of the Animal Disinfectants Market in 2024, reflecting ease of integration with automated dosing lines

- Foam formats are accelerating at an 8.1% CAGR, favored for contact-time advantages in barn and stable sanitizers applications

• By Application

- Dairy operations captured 37% of revenue in 2024, as teat-dip protocols and milking parlor sanitation remain non-negotiable

- Poultry disinfection solutions are poised to grow at a 10.3% CAGR, the fastest among all application segments

• By End User

- Livestock farms represented 61% of 2024 revenue within the Animal Disinfectants Market

- Integrated protein processors are forecast to grow at a 9.4% CAGR through 2035, as supply-chain traceability requirements expand

• By Region

- Europe dominated with 35% share in 2024

- While Asia-Pacific is the fastest-growing region at a 7.95% CAGR

Market Size and Forecast (2021–2035)

MRFR's sizing methodology triangulates bottom-up revenue modeling (manufacturer shipments, distributor sell-through) with top-down demand estimation (livestock population × disinfectant spend per head). Historical data draws on customs trade databases, company annual filings, and veterinary sanitation products procurement records. Forecast assumptions incorporate regulatory timelines, disease-outbreak frequency models, and raw-material price indices for iodine and quaternary ammonium compounds.