Anti Reflective Coatings Market Summary

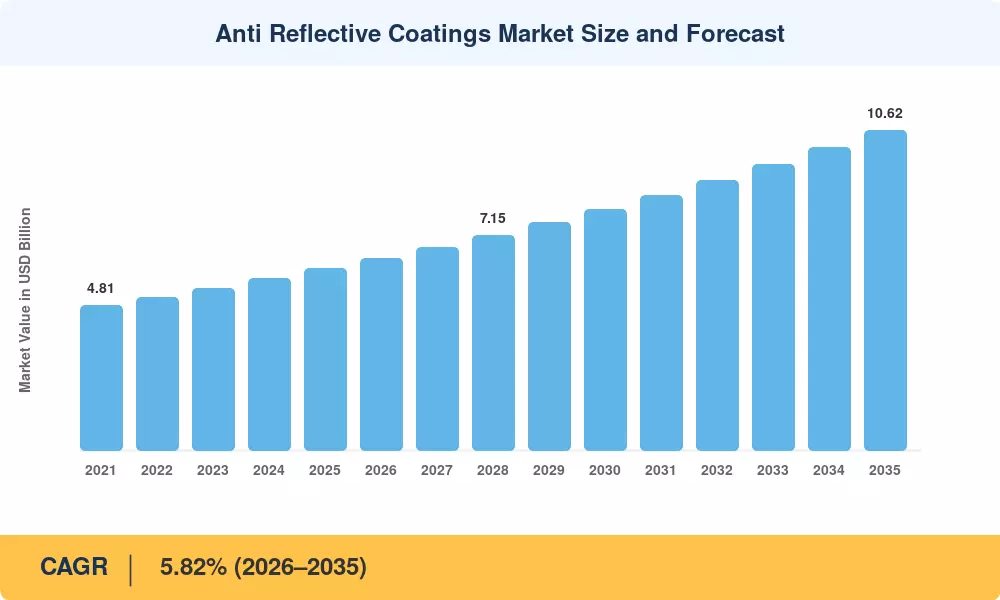

The Anti-Reflective Coatings Market was valued at USD 6.03 Billion in 2025 and is projected to grow from USD 6.38 Billion in 2026 to USD 10.62 Billion by 2035, registering a CAGR of 5.82% during the forecast period (2026–2035). Demand for optical thin films that suppress glare and boost light transmission coatings performance is accelerating across photovoltaic modules, consumer electronics, and precision optics. Government incentives for renewable energy capacity — particularly the U.S. Inflation Reduction Act's USD 370 billion clean-energy allocation and the EU's REPowerEU solar mandate — are expanding addressable coating area at a pace not seen in the previous decade [1][2].

The market for anti-reflective coatings is undergoing a significant technological change. Modern multilayer optical coating materials created by magnetron sputtering and plasma-enhanced chemical vapor deposition are replacing outdated single-layer magnesium fluoride stacks. Older dip-coat methods are unable to match the broadband reflectance < 0.5% that these lens coating technologies provide across the visible spectrum. Industry estimates indicate that as manufacturers grow throughput for bifacial solar glass and foldable display panels, global capital expenditure on new sputtering lines approached USD 1.2 billion in 2024 alone[4].

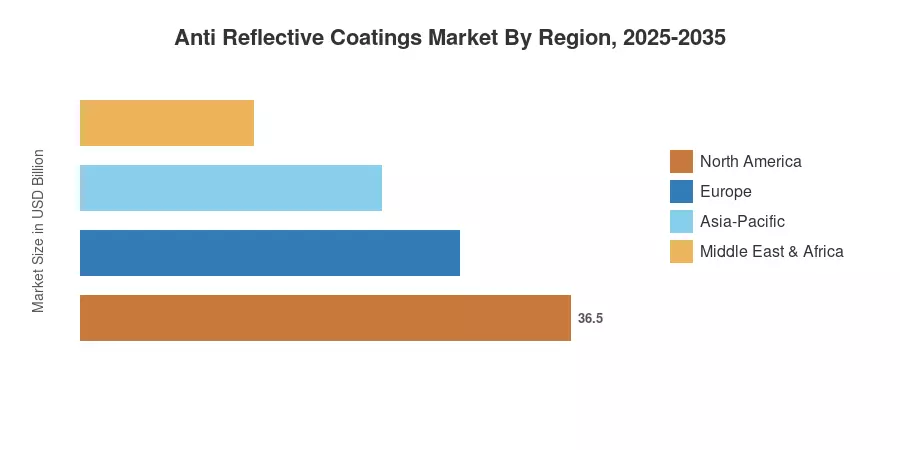

Driven by South Korea's display screen coatings ecosystem and China's dominating solar module manufacturing base, the Asia-Pacific region is the largest and fastest-growing region in the Anti-Reflective Coatings Market, accounting for around 36.5% of worldwide sales. North America comes in second with a 27.8% share, spurred by the growth of semiconductor factories and the acquisition of defense optics. Europe makes up about 23.2% of the total, with France and Germany leading the way in precision optical materials for medical devices and automotive head-up display integration. Businesses that combine proprietary recipe libraries with the scale of deposition equipment are increasingly rewarded by the competitive landscape [5][6].

Key Report Takeaways

• By Deposition Method

- Chemical vapor deposition held a 31.2% revenue share in the Anti-Reflective Coatings Market in 2025, anchored by its dominance in semiconductor-grade optical thin films.

- Sputtering is forecast to register the fastest CAGR of 6.93% through 2035, driven by demand for dense, low-defect glare reduction coatings on large-area glass substrates.

• By Application

- Electronic devices led the Anti-Reflective Coatings Market with a 39.3% share in 2025, reflecting surging adoption of display screen coatings in smartphones, tablets, and automotive infotainment panels.

- Solar panels are expected to post the highest application-level CAGR of 8.55% from 2026 to 2035, fueled by bifacial module architectures and light transmission coatings mandates.

• By Region

- Asia-Pacific accounted for a 36.5% revenue share in 2025 and is projected to expand at an 8.18% CAGR through 2035.

- North America's Anti-Reflective Coatings Market is valued at approximately USD 1.68 billion in 2025, supported by defense optics and semiconductor precision optical materials.

Market Size and Forecast (2021–2035)

Market Research Future's forecast model triangulates bottom-up revenue estimates from coating equipment OEMs, substrate manufacturers, and end-use adoption rates against top-down macroeconomic indicators, trade data, and capacity utilization surveys. Historical figures (2021–2024) reflect audited shipment volumes; forecast values (2026–2035) apply a calibrated CAGR of 5.82%, validated against primary interviews with coating line operators and procurement teams.