API Management Market Summary

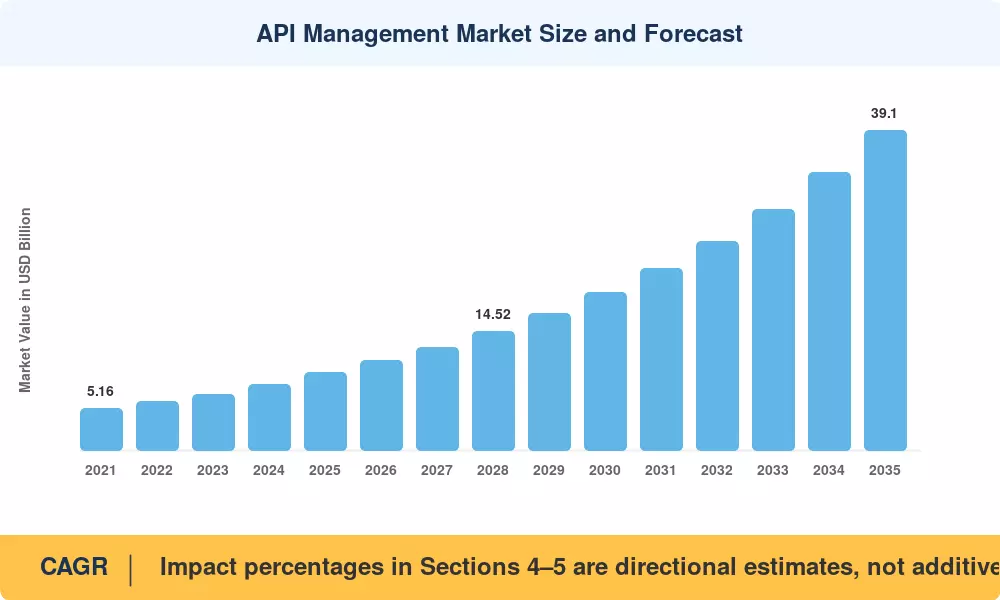

The API Management Market was valued at USD 9.50 Billion in 2025 and is projected to grow from USD 10.94 Billion in 2026 to USD 39.10 Billion by 2035, registering a CAGR of 15.2% during the forecast period (2026–2035). This expansion tracks directly to the enterprise-wide pivot toward API-first architectures, where every digital interface is designed, governed, and monetized as a standalone product rather than a backend utility. Regulatory pressure is compounding this shift — the EU's PSD3 directive and the U.S. Consumer Financial Protection Bureau's open-banking rulemaking both mandate standardized API access, forcing financial institutions to invest in compliant management platforms [1][2].

The technology transformation reshaping this space is structural. Monolithic middleware stacks that once handled integration tasks are giving way to distributed gateways, service meshes, and event-driven brokers that can scale across containerized and serverless environments. Cloud-native spending on application infrastructure crossed USD 68 Billion globally in 2024 according to estimates, and a meaningful share of that budget flows into the API Management Market as organizations operationalize microservices at scale [3].

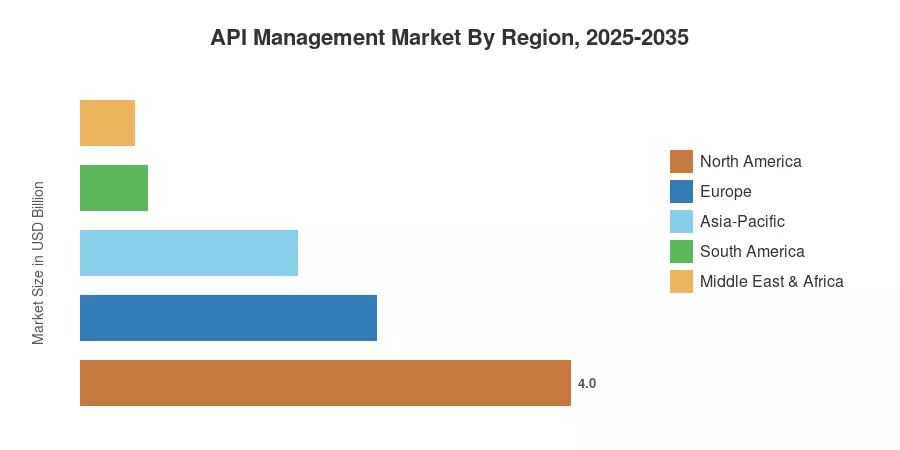

North America held approximately 42.1% of global revenue in 2025, anchored by hyperscaler ecosystems and a mature SaaS economy that generates massive API traffic volumes. Asia-Pacific is the fastest-growing region with a projected CAGR of 18.6% through 2035, propelled by 5G infrastructure rollouts, government digitization mandates in India and Indonesia, and the GSMA Open Gateway framework accelerating telecom API commercialization. Europe accounted for the second-largest share at roughly 25.5%, driven by open-finance regulation and the Digital Markets Act's interoperability requirements. The API Management Market is poised for a decade of compounding investment as generative AI workloads, embedded finance, and cross-industry data exchanges raise the governance stakes for every exposed endpoint.

Key Report Takeaways

• By Deployment Model

- Cloud deployments captured approximately 74.0% of the API Management Market in 2025, reflecting the migration of enterprise workloads to public and multi-cloud environments.

- Hybrid architectures are forecast to register a 19.4% CAGR through 2035 as regulated industries balance cloud economics with on-premise compliance requirements.

• By Offering

- Platform solutions accounted for roughly 65.6% of the API Management Market revenue in 2025, consolidating gateway, analytics, and policy-enforcement capabilities into unified suites.

- Services are projected to expand at a 24.6% CAGR to 2035, driven by demand for managed API operations and migration consulting.

• By End-User Industry

- Banking, financial services, and insurance led all verticals with a 29.3% revenue share in 2025, underpinned by open-banking mandates and real-time payment APIs.

- Healthcare is set to grow fastest at a 17.3% CAGR through 2035, fueled by FHIR-based interoperability standards and telehealth platform expansion.

• By Enterprise Size

- Large enterprises held 53.8% of the API Management Market in 2025.

- SMEs are advancing at a 23.5% CAGR through 2035, enabled by self-service developer portals and usage-based pricing tiers.

• By Region

- North America dominated with a 42.1% share in 2025.

- Asia-Pacific is forecast to register an 18.6% CAGR through 2035.

API Management Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining vendor revenue disclosures, enterprise IT budget surveys, and bottom-up demand modeling across deployment, offering, vertical, and enterprise-size dimensions. Historical figures (2021–2024) reflect audited vendor filings and verified industry datasets; forecast values (2026–2035) apply a calibrated CAGR anchored to macro indicators including cloud infrastructure spend, regulatory API mandates, and digital transformation budgets tracked by the World Bank [3][4].