Auto Bodywork Repair Market Summary

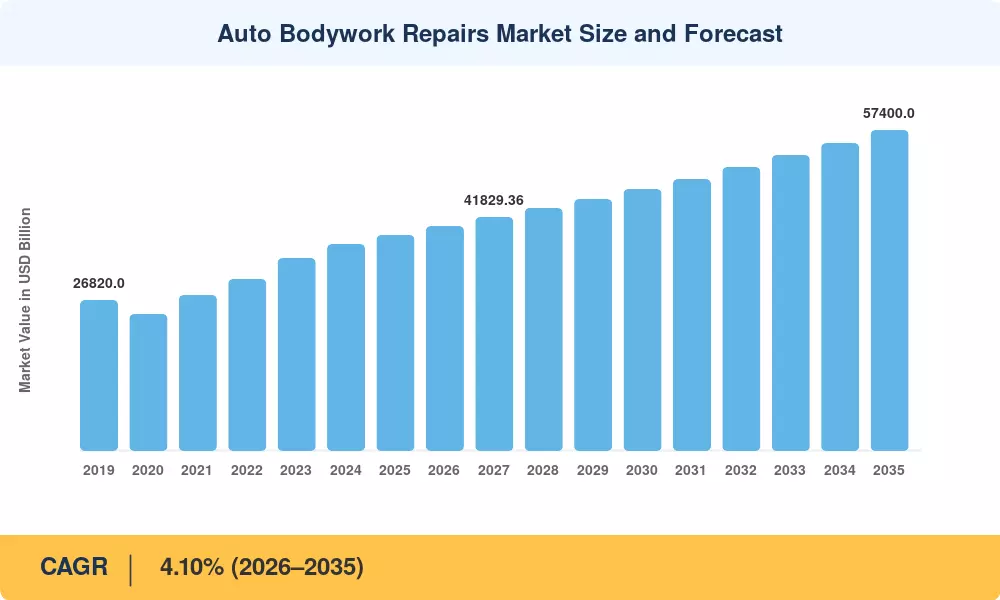

The global auto bodywork repairs market was valued at USD 38.63 billion in 2025 and is projected to reach USD 40.11 billion in 2026, growing to USD 57.40 billion by 2035 at a compound annual growth rate (CAGR) of 4.10% during the forecast period (2026–2035). This steady expansion is underpinned by a sustained increase in the global vehicle parc, which surpassed 1.47 billion units in 2024, directly elevating the frequency and volume of collision and cosmetic repair incidents [2]. Simultaneously, the rise of disposable incomes across both developed and emerging economies has encouraged vehicle owners to seek professional bodywork services rather than informal or deferred repairs, supporting higher average repair order values. Technological advancements in repair equipment—including AI-assisted damage estimation, computerized paint-matching systems, and advanced welding techniques- have further enhanced throughput and quality, drawing a larger share of repairs into the formal market [3].

With USD 11.04 billion in 2025, the collision repair market is the single largest service category, showing the ongoing incidence of traffic accidents worldwide. But with a 5.20% CAGR through 2035, paint repair and refinishing is the service type that is expanding the fastest due to consumer demand for aesthetic restoration and the widespread use of premium, multi-coat paint finishes on contemporary cars [4]. With AI-powered parts procurement producing quantifiable benefits in workflow performance and cycle-time reduction, the December 2025 rollout of Orderly by PartsTrader throughout Crash Champions' more than 650 repair centers is an example of how technology-led efficiency gains are transforming the industry [5]. As fleet operators place a greater emphasis on vehicle appearance and structural integrity for safety compliance and brand image, the commercial vehicles market is growing at a 5.30% CAGR on the vehicle-type axis, with buses and coaches leading the way with a 6.10% CAGR.

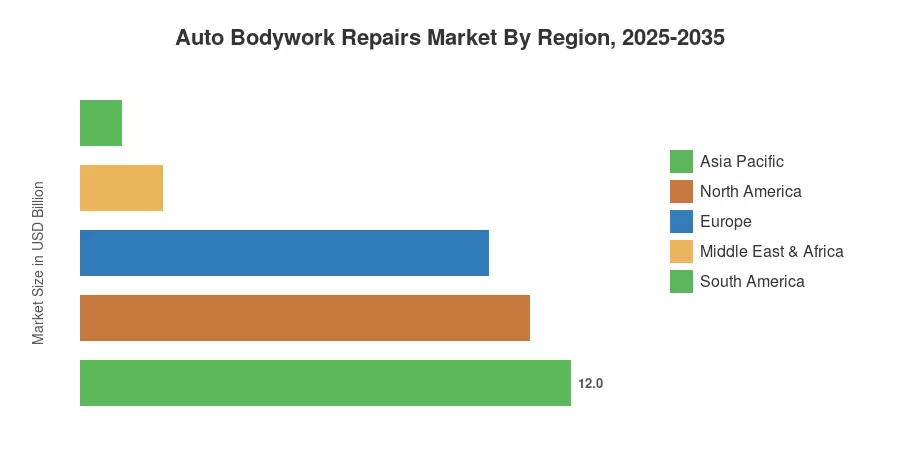

With a 2025 revenue base of USD 11.79 billion, North America continues to be the leading regional market. This is due to the region's high insurance penetration, well-established multi-shop operator (MSO) networks, and strict OEM-certified repair standards [6]. With an expected CAGR of 5.28%, Asia Pacific is the fastest-growing area, driven by China's enormous and developing auto aftermarket as well as the fast motorization of Indonesia (7.60% CAGR) and India (7.80% CAGR) [7]. With a projected value of USD 10.03 billion in 2025, Europe is the second-largest regional market. The adoption of electric vehicles and the governmental drive for environmentally friendly repair methods are driving this increase. Long-term, above-GDP growth is anticipated in all major regions through 2035 due to the convergence of EV-specific repair demand, digital service booking platforms, and MSO consolidation.

Key Report Takeaways

| Segment Dimension | Key Metric | Notes |

| By Service Type — Dominant | Collision Repair: USD 11,038.47 Mn (2025) | The largest service category is driven by road traffic accident frequency |

| By Service Type — Fastest Growing | Paint Repair and Refinishing: 5.20% CAGR | Premium paint finishes and aesthetic restoration demand are rising |

| By Vehicle Type — Dominant | Passenger Cars: USD 25,878.16 Mn (2025) | SUVs contribute USD 10,935.25 Mn within this category |

| By Vehicle Type — Fastest Growing | Commercial Vehicles: 5.30% CAGR | The Buses and Coaches sub-segment at 6.10% CAGR leads the growth |

| By Application — Dominant | ICE Vehicles: USD 31,942.95 Mn (2025) | Still represents 82.7% of the total market revenue |

| By Application — Fastest Growing | Electric Vehicles: 6.90% CAGR | EV-specific bodywork repair demand is accelerating rapidly |

| By End-User — Dominant | Insurance Companies: USD 15,763.54 Mn (2025) | Insurance-funded claims account for 40.8% of the market value |

| By End-User — Fastest Growing | Fleet Owners and Corporate Clients: 4.40% CAGR | Corporate fleet management is driving outsourced repair volumes |

| By Service Provider — Dominant | Independent Body Shops: USD 20,822.22 Mn (2025) | Commands 53.9% market share by revenue |

| By Service Provider — Fastest Growing | Multi Shop Operators (MSOs): 4.70% CAGR | Consolidation through M&A continues to accelerate |

| By Region — Dominant | North America: USD 11,792.00 Mn (2025) | High insurance penetration and mature MSO ecosystem |

| By Region — Fastest Growing | Asia Pacific: ~5.28% CAGR | India and Indonesia each exceed 7.5% CAGR |

Market Size and Forecast (2019–2035)

Market Research Future (MRFR) employs a triangulated forecasting methodology combining bottom-up revenue aggregation from company financials and industry associations, top-down macroeconomic modeling incorporating vehicle registration growth, accident frequency rates, and insurance claim trends, and demand-side analysis validated through primary interviews with body shop operators, insurers, and OEM parts distributors. The base year for this study is 2025, with historical data spanning 2019–2024 and forecast projections extending through 2035.

.webp?v=1784802951)