Automotive Parts Market Summary

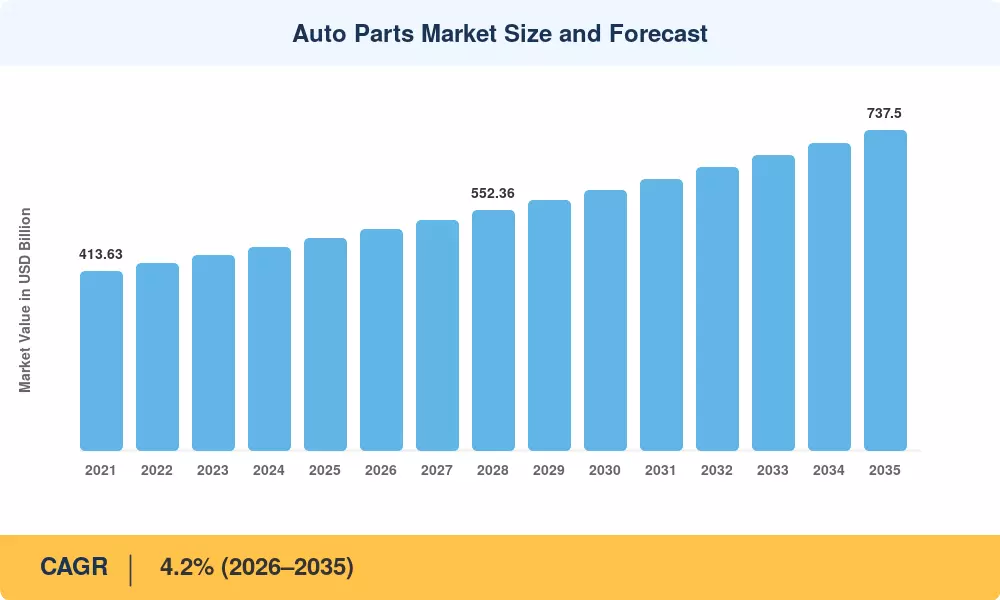

The global Auto Parts Market reached an estimated USD 488.0 billion in 2025 and is projected to grow from USD 509.0 billion in 2026 to USD 737.5 billion by 2035, registering a CAGR of 4.2% during the forecast period (2026–2035). Two structural forces are powering this expansion: the accelerating EV battery motor supply chain build-out driven by government mandates such as the EU's 2035 combustion-engine phase-out, and the explosive rise of aftermarket e-commerce platforms that are reshaping how consumers and workshops procure replacement components [2][3].

The auto parts market is undergoing a broad technological revolution. Remanufactured parts exchange programs and digital-first distribution models are supplementing, and in some cases replacing, traditional single-source OEM genuine parts replacement channels. A parallel demand corridor for battery packs, electric drive modules, and thermal management assemblies was established by the U.S. Inflation Reduction Act alone, which allocated nearly USD 7.5 billion in EV-related manufacturing credits until 2032 [4]. The industry is expected to save over USD 140 billion in raw material costs by 2030, thanks to the remanufacturing sector, which highlights the financial benefits of circular supply chains.

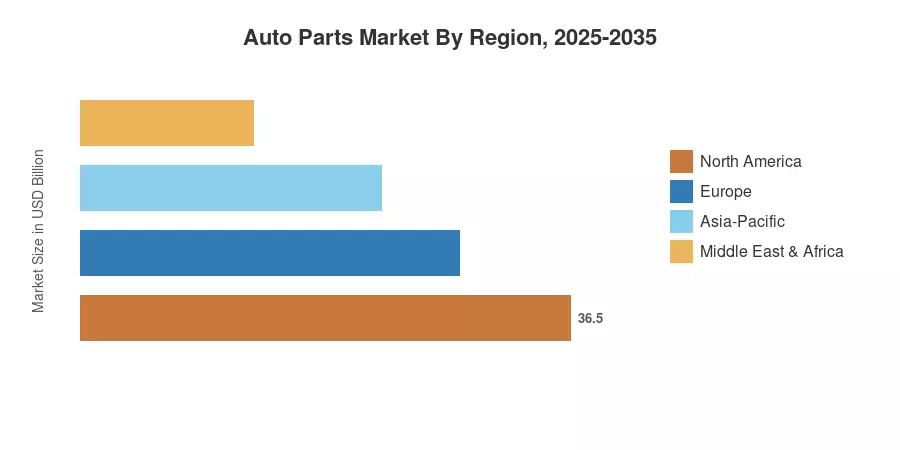

With a revenue share of over 42%, Asia-Pacific dominates the auto parts market thanks to the enormous vehicle fleets of China, India, and Japan. With an estimated 5.4% CAGR, the region likewise has the fastest growth, driven by the expansion of parts distribution warehouses and rising rates of car ownership. Due to strict Euro 7 emissions regulations that raise the complexity and cost of replacement parts, Europe has the second-largest share at over 25%. North America comes in second with a share of 23%, where a developed aftermarket e-commerce infrastructure and counterfeit anti-fraud enforcement maintain consistent demand [5][6]. Players that simultaneously master omnichannel distribution and EV preparedness will be rewarded in the upcoming ten years.

Key Report Takeaways

• By Part Type

- Engine and powertrain components account for approximately 28% of the Auto Parts Market, reflecting ongoing ICE fleet servicing needs alongside hybrid powertrain growth

- Electrical and electronic parts are growing at an estimated 5.8% CAGR, propelled by ADAS proliferation and EV battery motor supply requirements

- Suspension and braking systems represent roughly USD 89 billion in 2025 revenue, supported by OEM genuine parts replacement demand in commercial fleets

• By Sales Channel

- The aftermarket channel holds approximately 55% of the Auto Parts Market, driven by vehicle aging trends and aftermarket e-commerce adoption

- OEM channels are expanding at a 3.6% CAGR as automakers invest in certified remanufactured parts exchange programs

• By Region

- Asia-Pacific dominates with 42% share in the Auto Parts Market, led by China's parts distribution warehouse investments

- North America's aftermarket e-commerce penetration exceeds 18% of total channel revenue

- Middle East & Africa grows at 4.8% CAGR, driven by expanding vehicle parc and import-dependent supply chains

Auto Parts Market Size and Forecast (2021–2035)

Market sizing combines bottom-up revenue tracking from 120+ OEM and aftermarket suppliers with top-down validation against vehicle registration databases, trade flow data, and government industrial statistics across 32 countries.