Automotive Fuel Delivery System Market Summary

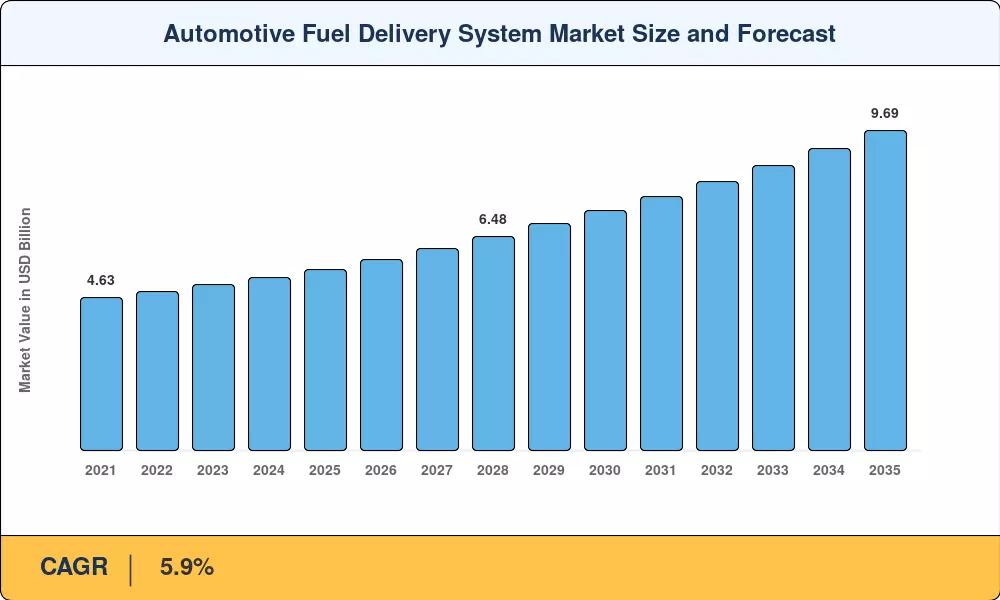

The Automotive Fuel Delivery System Market reached USD 5.48 billion in 2025 and is projected to grow from USD 5.78 billion in 2026 to USD 9.69 billion by 2035, registering a CAGR of 5.9% across the forecast period. Two regulatory forces are keeping capital flowing into combustion-era fuel hardware even as electrification gains ground: the European Commission's Euro 7 emission limits, enforceable from July 2025, and the U.S. EPA Phase 3 greenhouse-gas standards taking effect in 2027 [1][2]. Both mandates require automakers to deploy higher-precision injection modules and corrosion-resistant fuel lines, sustaining investment in modern internal-combustion engine (ICE) architectures.

A significant technology shift is underway within the Automotive Fuel Delivery System Market. Legacy port fuel injection setups are giving way to gasoline direct injection (GDI) platforms that improve combustion efficiency by 15–20% while cutting particulate emissions [3]. Tier-1 suppliers have earmarked more than USD 2.8 billion collectively for next-generation fuel rail, pump, and injector programs through 2028, according to company filings and BloombergNEF estimates [4]. Hydrogen-compatible delivery hardware is also attracting R&D budgets as fuel-cell commercial vehicles move beyond pilot stages.

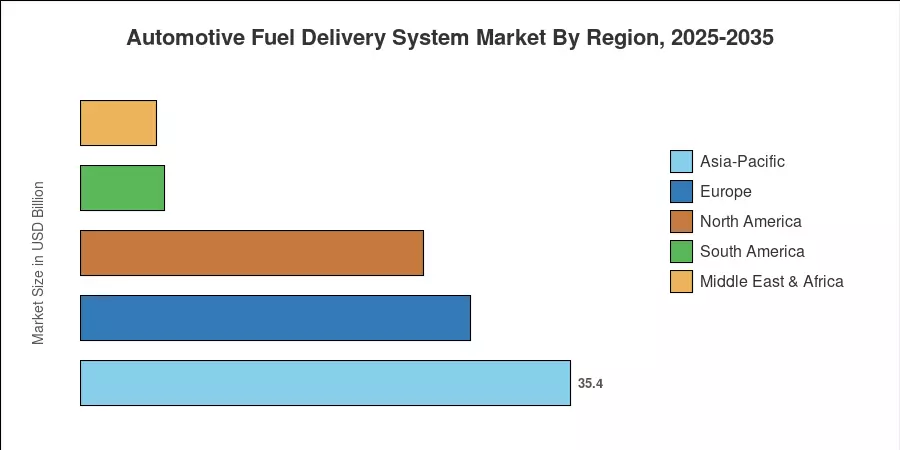

Asia-Pacific commands the largest share of the Automotive Fuel Delivery System Market at roughly 35.4% of 2025 revenue, driven by China's 28-million-unit annual vehicle output and India's expanding passenger-car parc [5]. The region is also the fastest-growing, forecast to post a 7.3% CAGR through 2035. Europe holds the second-largest position with approximately 28.2% share, anchored by stringent emission compliance timelines that compel ongoing fuel-system upgrades. North America follows at 24.8%, where light-truck and SUV dominance sustains demand for high-flow fuel pump assemblies.

Key Report Takeaways

• By Component

- Fuel pumps accounted for 34.6% of the Automotive Fuel Delivery System Market in 2025, reflecting their role as the highest-value single component in every ICE powertrain.

- Fuel injectors are forecast to expand at a 7.5% CAGR through 2035, outpacing the overall market as GDI adoption intensifies.

• By Vehicle Type

- Passenger cars generated 59.2% of the Automotive Fuel Delivery System Market revenue in 2025, underpinned by sedan and crossover production volumes in China and Europe.

• By Fuel Type

- Hydrogen fuel delivery systems are projected to grow at a 13.0% CAGR to 2035 as commercial-vehicle OEMs scale fuel-cell platforms.

• By Delivery Method

- Gasoline direct injection captured 42.6% of total revenue in 2025, reflecting widespread OEM adoption in turbocharged engines.

• By Distribution Channel

- The aftermarket replacement channel is poised for an 8.1% CAGR through 2035 as the global vehicle parc ages beyond warranty coverage.

• By Region

- Asia-Pacific led the Automotive Fuel Delivery System Market with 35.4% share in 2025 and is forecast to register a 7.3% CAGR to 2035.

- North America contributed 24.8% share, buoyed by strong pickup-truck and SUV sales requiring high-capacity fuel delivery modules.

Market Size and Forecast (2021–2035)

Data in this section draws on company filings, OICA production statistics, regulatory impact assessments, and proprietary triangulation by Market Research Future. Historical values reflect actual industry revenue; forecast figures apply the calibrated 5.9% CAGR with year-level adjustments for anticipated regulatory step-changes and production cycle effects.