Automotive Leaf Spring Market Summary

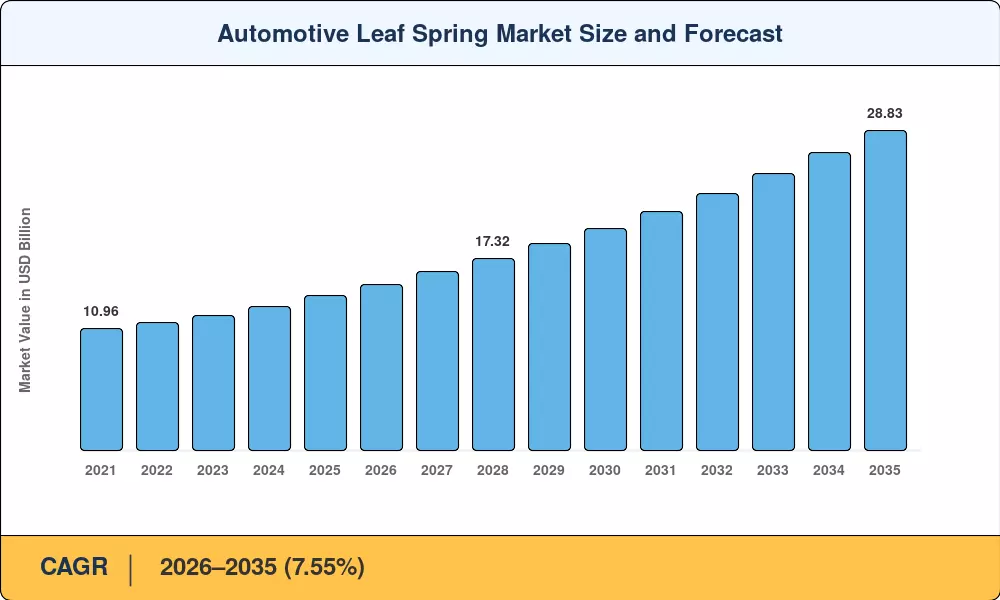

The Automotive Leaf Spring Market reached an estimated USD 13.92 billion in 2025, positioning itself for a forecast-period opening value of USD 14.97 billion in 2026 and a trajectory toward USD 28.83 billion by 2035 at a 7.55% CAGR. Two catalysts are fueling this acceleration: a global surge in commercial-vehicle production driven by e-commerce logistics infrastructure build-outs, and government mandates across the EU and China requiring fleet-level CO₂ intensity reductions that push OEMs toward lighter suspension assemblies [1][2]. The International Energy Agency's Global EV Outlook 2025 projects that medium- and heavy-duty electric truck registrations will triple by 2030, creating fresh demand for spring systems engineered to offset battery mass without sacrificing payload ratings [1].

A transformation is underway inside the Automotive Leaf Spring Market as conventional multi-leaf steel packs give way to parabolic steel and fiber-reinforced composite designs. Composite springs can deliver weight savings of 50–70% per assembly compared to traditional steel, and OEMs such as Volvo Trucks and Daimler Trucks have committed over USD 400 Million collectively to next-generation chassis lightweighting programs through 2028 [3][4]. Hybrid steel-composite architectures — pairing a single parabolic steel leaf with a glass-fiber overwrap — are emerging as a cost-effective bridge technology, especially for the aftermarket retrofit channel.

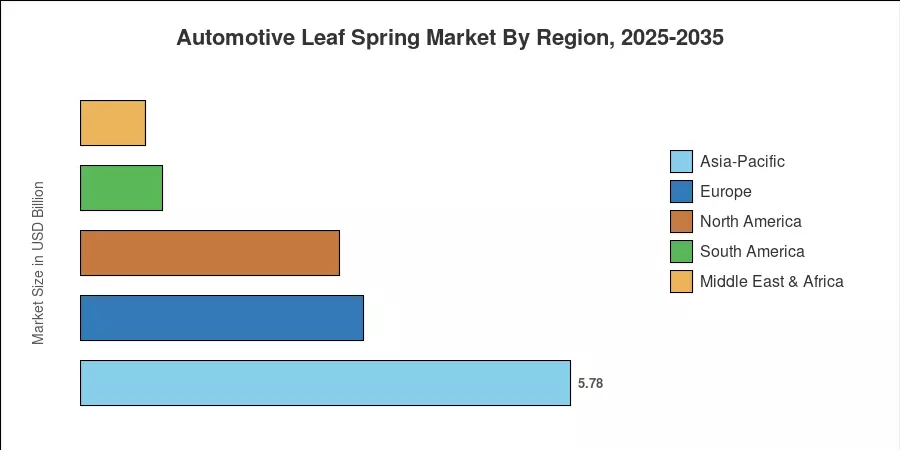

Asia-Pacific dominates the Automotive Leaf Spring Market with roughly 41.5% of 2025 revenue, powered by India's and China's combined output of more than 12 million commercial vehicles annually [5]. North America holds the second-largest position at approximately 22% share, buoyed by Class 8 truck replacement cycles and the reshoring of trailer manufacturing. Europe, contributing around 24% of global revenue, is the second-fastest-growing region as Euro VII emission standards compel fleet operators to adopt lighter suspension components. The decade ahead will reward suppliers who can scale composite production while maintaining the cost discipline that steel incumbents have perfected over generations.

Key Report Takeaways

• By Spring Type

- Semi-elliptical configurations accounted for approximately 59% of global Automotive Leaf Spring Market revenue in 2025, reflecting their entrenched position in heavy-duty truck platforms across Asia and North America.

- Parabolic designs are projected to record the fastest segment CAGR of 7.58% through 2035, as fleet operators pursue ride comfort and weight-efficiency gains.

• By Material

- Steel held a commanding 69% share of the Automotive Leaf Spring Market in 2025, owing to lower upfront cost and established supply chains.

- Composite materials are on track for an 8.85% CAGR through 2035 as OEMs intensify lightweighting efforts.

• By Vehicle Type

- Light commercial vehicles led the Automotive Leaf Spring Market with approximately 39% revenue share in 2025, driven by last-mile delivery expansion.

• By Sales Channel

- OEM installations captured roughly 65% of total Automotive Leaf Spring Market revenues in 2025.

• By Region

- Asia-Pacific accounted for 41.5% of global revenue in 2025 and is advancing at the fastest regional CAGR of 6.67%.

Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology that cross-references proprietary bottom-up revenue models with OEM production databases, trade-flow datasets, and published aftermarket channel data to arrive at historical and forecast estimates for the Automotive Leaf Spring Market. All forecast values assume a constant-currency baseline and incorporate scenario adjustments for raw-material price volatility and regulatory timelines.

.webp?v=1784551665)