Automotive Night Vision System Market Summary

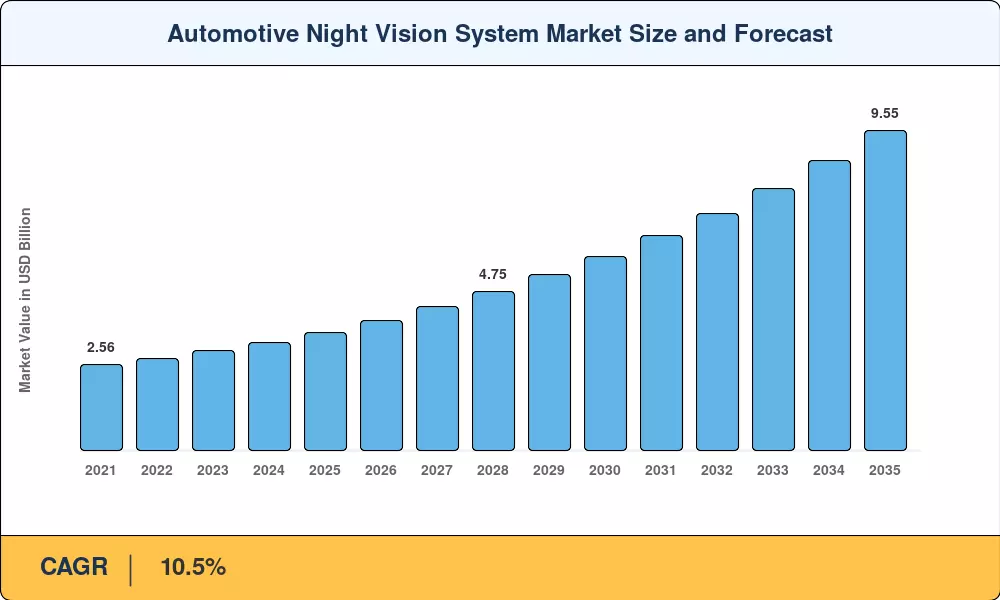

The Automotive Night Vision System Market was valued at USD 3.52 billion in 2025 and is projected to reach USD 3.89 billion in 2026 before climbing to USD 9.55 billion by 2035, registering a CAGR of 10.5% during the forecast period (2026–2035). This upward trajectory is anchored in regulatory momentum: the U.S. National Highway Traffic Safety Administration's Federal Motor Vehicle Safety Standard No. 127 mandates pedestrian automatic emergency braking for all new light vehicles by September 2029, compelling OEMs to integrate thermal-sensing modules into production pipelines [1]. The European Union's updated General Safety Regulation, effective July 2024, similarly pressures automakers to adopt advanced pedestrian-protection technologies across all new type-approved vehicles [2].

A technology shift is underway across the Automotive Night Vision System Market as legacy visible-light camera stacks yield ground to uncooled microbolometer arrays and wafer-level optics. Between 2023 and 2025, average sensor module costs fell approximately 18%, driven by semiconductor wafer-level packaging innovations that reduced per-unit optics costs from roughly USD 120 to under USD 98 [3]. Premium battery-electric platforms from European and Chinese manufacturers have become early adopters, embedding thermal cameras directly into ADAS architectures rather than treating night-vision as a standalone luxury add-on [4].

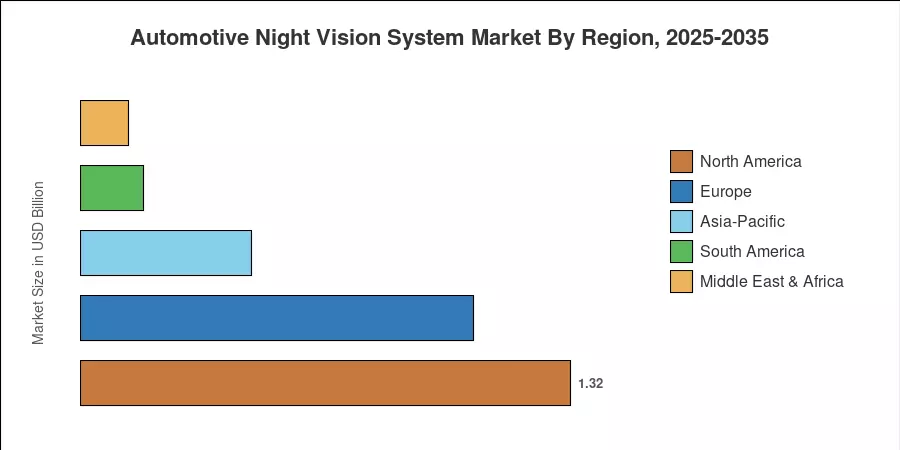

North America commands the largest share of the Automotive Night Vision System Market at 37.5% of global revenue in 2025, buoyed by stringent federal pedestrian-safety mandates and a large premium-vehicle installed base. Asia-Pacific is the fastest-growing region, projected at a 13.2% CAGR through 2035, as Chinese and South Korean OEMs scale thermal integration across mid-tier platforms. Europe holds the second-largest share at 30.2%, supported by Euro NCAP's tightening scoring protocols that reward active night-vision functionality [5]. By 2035, the Automotive Night Vision System Market is expected to transition from a premium differentiator to a mainstream compliance feature across all major automotive regions.

Key Report Takeaways

• By Technology

- Far Infrared (LWIR) technology held 58.4% of the Automotive Night Vision System Market share in 2025, reflecting its passive detection advantage and lower component complexity.

- Short-Wave Infrared (SWIR) is the fastest-growing technology segment, advancing at a 17.1% CAGR through 2035 as gallium arsenide sensor costs decline.

• By Component

- Night Vision Cameras accounted for 59.1% of component revenue in 2025, remaining the core hardware element in every integration architecture.

• By Display

- Central Infotainment Screens are forecast to grow at a 17.0% CAGR through 2035, displacing dedicated instrument-cluster displays.

• By Region

- North America led the Automotive Night Vision System Market with 37.5% revenue share in 2025, driven by FMVSS No. 127 compliance timelines.

- Asia-Pacific is projected to expand at a 13.2% CAGR, with China alone contributing over half of regional demand.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates top-down revenue estimates from OEM procurement databases with bottom-up sensor-shipment volumes reported by tier-1 suppliers. Historical figures (2021–2024) rely on audited company filings and customs-trade data, while the forecast horizon (2026–2035) applies econometric regressions tied to vehicle production volumes, regulatory phase-in calendars, and component price-erosion curves.