Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Material Type | Glass, Fabric, Others (Polycarbonate, Composite) | Glass | Fabric |

| Sunroof System Type | Panoramic, Built-In (Inbuilt), Tilt-N-Slide, Pop-Up, Others | Panoramic | Panoramic |

| Operation Type | Electric, Manual | Electric | Electric |

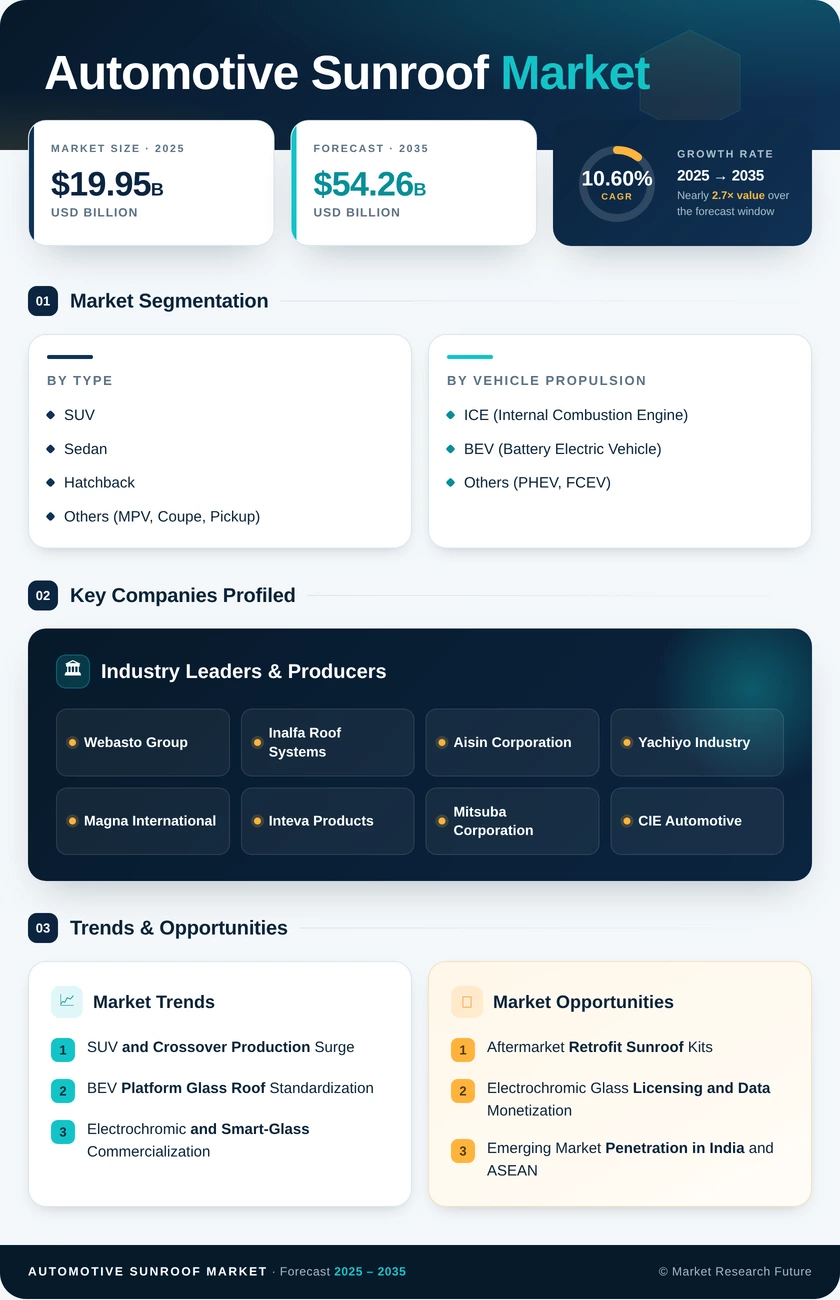

| Vehicle Type | SUV, Sedan, Hatchback, Others (MPV, Coupe, Pickup) | SUV | Hatchback |

| Vehicle Propulsion | ICE, BEV, Others (PHEV, FCEV) | ICE | BEV |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Material Type

| Sub-Segment | Key Trend |

| Glass | Continued dominance driven by cost-down learning curves and OEM standardization across all vehicle tiers |

| Fabric | Niche growth in convertible and retro-styled vehicles; soft-top folding mechanisms gaining design interest |

| Others (Polycarbonate, Composite) | Lightweight alternatives emerging for weight-sensitive BEV platforms and high-performance vehicles |

Glass materials remain the backbone of the global sunroof supply chain, supported by decades of automotive-grade manufacturing infrastructure and consumer association with premium quality. Polycarbonate and composite alternatives are gaining strategic importance as lightweighting regulations tighten, particularly in Europe under Euro 7 mandates.

By Sunroof System Type

| Sub-Segment | Key Trend |

| Panoramic | Fastest absolute growth; expanding from premium to mid-segment SUVs and crossovers globally |

| Built-In (Inbuilt) | Steady volume in sedan and hatchback applications; cost-optimized single-panel designs |

| Tilt-N-Slide | Preferred in compact vehicles for ventilation-focused functionality |

| Pop-Up | Entry-level and aftermarket segment; declining OEM fitment |

| Others | Custom and specialty configurations for luxury and limited-edition models |

The panoramic category is reshaping consumer expectations for cabin openness, with multi-panel roof designs now standard on many SUVs. Built-in systems continue to serve the sedan market reliably, while pop-up configurations are gradually exiting OEM catalogs.

By Operation Type

| Sub-Segment | Key Trend |

| Electric | Near-universal OEM adoption; integration with rain sensors, voice commands, and one-touch mechanisms |

| Manual | Declining share limited to budget vehicles in emerging markets. |

The transition from manual to electrically operated sunroofs is effectively complete in developed markets, with electric mechanisms now accounting for the vast majority of OEM installations. Manual variants persist only where extreme cost sensitivity dictates minimal electronic content.

By Vehicle Type

| Sub-Segment | Key Trend |

| SUV | Leading installation volumes; large roof area enables panoramic and multi-panel configurations |

| Sedan | Traditional sunroof segment; compact panoramic designs gaining ground in executive models |

| Hatchback | Growing sunroof adoption in European and Asian urban vehicles |

| Others (MPV, Coupe, Pickup) | Pickup truck sunroof demand rising in North America; coupe and MPV steady |

SUVs dominate sunroof installations globally due to favorable roof geometry and consumer willingness to pay for cabin experience features. Hatchbacks represent an emerging growth category as urban-focused OEMs add sunroof options to differentiate in competitive compact segments.

By Vehicle Propulsion

| Sub-Segment | Key Trend |

| ICE | Majority installed base; gradually declining share as BEV penetration accelerates |

| BEV | Fastest-growing propulsion segment; platform-native glass roof integration drives higher attach rates |

| Others (PHEV, FCEV) | Transitional powertrains with premium content; moderate sunroof adoption rates |

Internal combustion vehicles continue to represent the bulk of sunroof installations, but battery-electric platforms are growing sunroof content at approximately double the overall market rate. EV-native architecture favors fixed and retractable glass roofs as core design elements.