Automotive Sunroof Market Summary

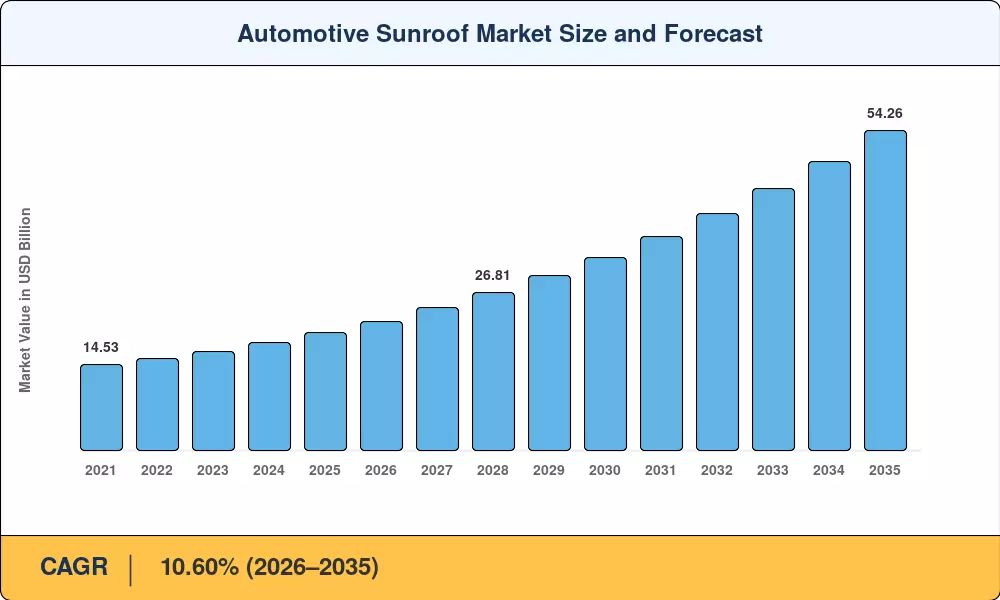

The Automotive Sunroof Market reached USD 19.95 billion in 2025 and is projected to grow from USD 21.92 billion in 2026 to USD 54.26 billion by 2035, registering a CAGR of 10.60% during the forecast period. This expansion is anchored in two converging forces: the structural shift toward sport utility vehicles across every price tier, and aggressive packaging strategies by volume automakers who now treat sunroof options as standard trim differentiators rather than luxury add-ons. OEM procurement data from 2024 shows that more than 60% of new vehicle platforms launched in North America and Europe included at least one roof-opening variant, a proportion that was below 40% just five years earlier.

The technology landscape in the Automotive Sunroof Market is set for generational shift. Traditional pop-up and tilt-only designs are quickly giving way to complete panoramic and electrochromic smart-glass setups that incorporate temperature management, UV filtration and variable tinting into a single module. Battery-electric vehicle programs have hastened this change, with fixed glass roofs simplifying body-in-white complexity while enhancing cabin aesthetics, and numerous EV-native platforms now featuring glass roof panels as a non-negotiable structural element. Global investment in smart-glass production capacity is expected to exceed USD 1.8 billion between 2023 and 2025, with significant capacity expansions in China, Germany and Mexico [2].

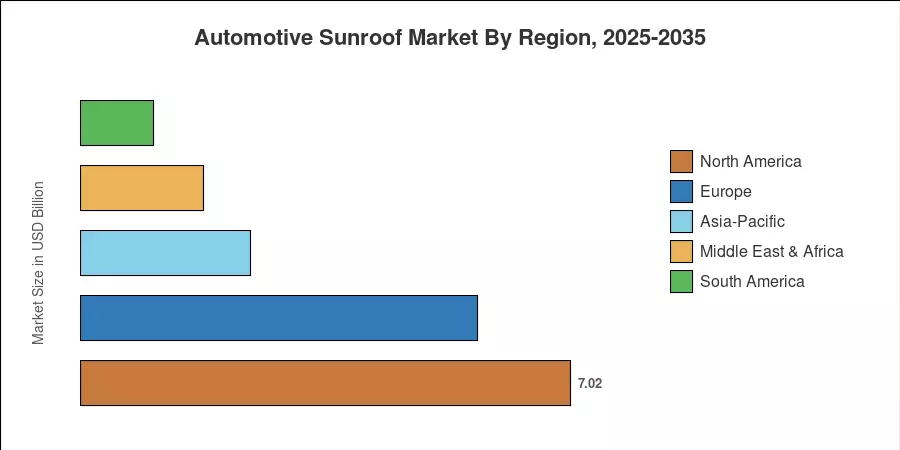

North America leads the global Automotive Sunroof Market with around 35.2% of the revenue share, owing to consumer desire for large-format SUVs and premium trim take-rates. The Asia-Pacific region will expand the fastest at 12.2% CAGR to 2035, with growth driven by increased car ownership among the middle-class in China and India, and cost-competitive production centers serving global OEM platforms. Europe has a share of around 28.5% in the market due to strict restrictions for lightweighting, which is in the favor of sophisticated glass composites instead of typical steel roof panels. In the coming decade, providers will compete on smart glass integration, modular platform compatibility and regional cost arbitrage.

Key Report Takeaways

• By Material Type

- Glass materials accounted for roughly 80.2% of the Automotive Sunroof Market in 2025, reflecting the dominance of tempered and laminated glass panels across all vehicle segments.

- Fabric alternatives are forecast to climb at a significant CAGR through 2031.

• By Vehicle Type

- SUVs led installation volumes with a 40.1% share in 2025, benefiting from large roof surface areas and consumer willingness to pay for premium features.

- Battery-electric vehicles represent the fastest-growing propulsion segment in the Automotive Sunroof Market through 2035, driven by platform designs that integrate fixed or retractable glass roofs as a core body element.

• By Geography

- North America generated the largest regional revenue for the Automotive Sunroof Market at 35.2% share in 2025, while Asia-Pacific leads forecast growth at a 12.2% CAGR.

- Europe remains the second-largest contributor, with Germany and France anchoring demand through premium vehicle production.

Automotive Sunroof Market Size and Forecast (2021–2035)

Market Research Future (MRFR) arrives at sizing estimates by using a triangulated technique using OEM production schedules, tier-1 supplier shipment data, aftermarket channel audits, and trade association information. Historical values (2021–2024) are checked to customs data and reported income of public sunroof makers. Forecast projections are derived from a bottom-up build based on car production forecasts, sunroof attachment rates by segment and average selling price trajectories.