Automotive Vacuumless Braking Market Summary

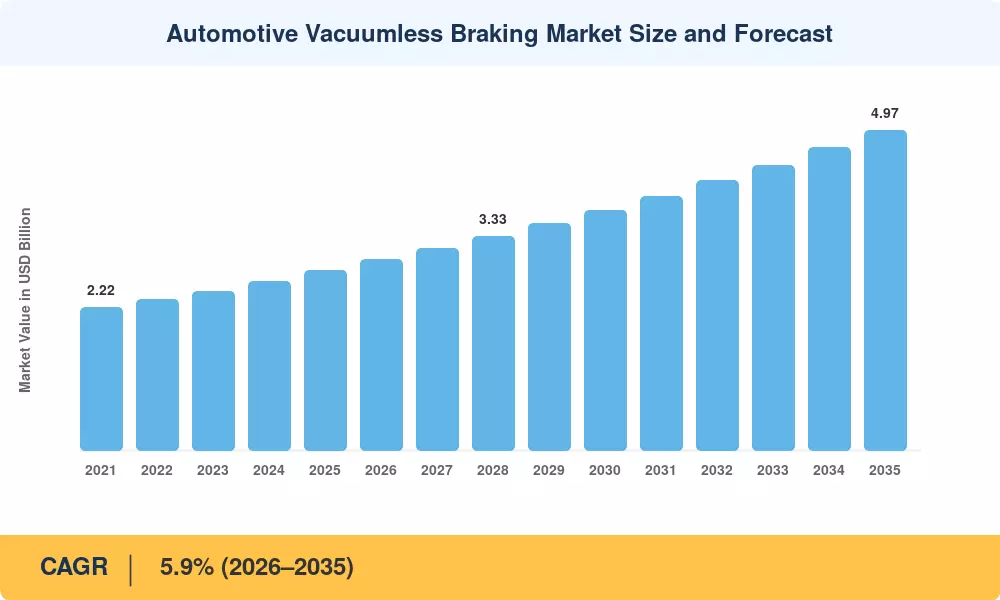

The automotive vacuumless braking market reached an estimated USD 2.80 billion in 2025 and is projected to grow from USD 2.97 billion in 2026 to USD 4.97 billion by 2035, registering a CAGR of 5.9% during the forecast period. This expansion is anchored in the global pivot toward vehicle electrification — battery electric vehicles and plug-in hybrids eliminate the engine-driven vacuum pump that traditional brake boosters depend on, making vacuumless solutions a structural requirement rather than an optional upgrade. The European Union's tightening CO₂ fleet-emission standards (95 g/km target) and China's dual-credit policy have accelerated OEM adoption timelines for these systems across every major production platform [2].

Legacy vacuum-assisted brake boosters, which have served the industry for over five decades, are being displaced by electronically controlled hydraulic and electromechanical brake-by-wire architectures. Continental's MK C1 integrated brake system and Bosch's iBooster represent the leading edge of this transition, with cumulative OEM integration contracts surpassing 40 million units by late 2024 [3]. Automakers are investing heavily because these systems enable faster brake-pressure build-up, seamless regenerative braking integration, and the pedal-feel calibration necessary for Level 3+ autonomous driving.

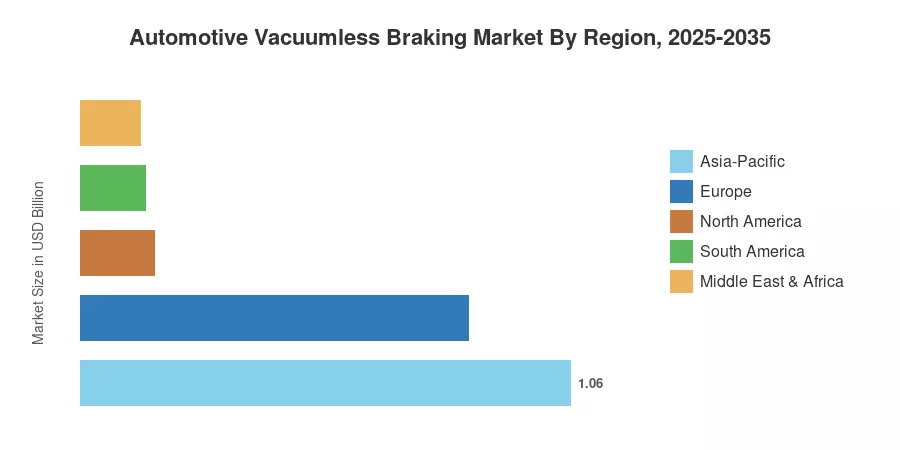

Asia-Pacific commands the largest share of the automotive vacuumless braking market at roughly 38% of 2025 revenue, driven by massive EV production volumes in China, Japan, and South Korea. The region also holds the fastest CAGR at approximately 6.8% through 2035. Europe follows as the second-largest region with about 30% share, supported by stringent emissions mandates and strong Tier-1 supplier presence. North America rounds out the top three with approximately 22% share, buoyed by the Inflation Reduction Act's EV tax credits and rising ADAS penetration across light trucks and SUVs.

Key Report Takeaways

• By Vehicle Type

- Passenger cars account for the dominant share of the automotive vacuumless braking market, holding approximately 68% of 2025 revenue, propelled by the mass-market EV transition across sedans, hatchbacks, and crossovers.

- Commercial vehicles represent a CAGR of 7.1% through 2035, as fleet electrification programs and autonomous trucking pilots accelerate brake-by-wire adoption.

• By Electric Vehicle Type

- Battery electric vehicles (BEVs) lead the automotive vacuumless braking market with an estimated 52% share, since these platforms have zero vacuum generation and require electric or electrohydraulic boosting by default.

- Plug-in hybrid electric vehicles (PHEVs) are the fastest-growing EV sub-segment at a projected 6.5% CAGR, reflecting increasing PHEV production in Europe and China.

• By Region

- Asia-Pacific dominates the automotive vacuumless braking market with a 38% revenue share, led by China's position as the world's largest EV producer.

- North America is projected to reach USD 1.09 billion by 2035, supported by rising EV and ADAS adoption rates across the region.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates bottom-up OEM production data, Tier-1 supplier revenue disclosures, and top-down macroeconomic modeling. Historical figures (2021–2024) rely on audited financial statements and trade databases; the 2025 base year uses preliminary production and shipment data. Forecast projections (2026–2035) apply a compound annual growth rate derived from demand-side drivers, regulatory scenarios, and technology adoption curves calibrated against comparable published benchmarks.