Bariatric Surgery Market Summary

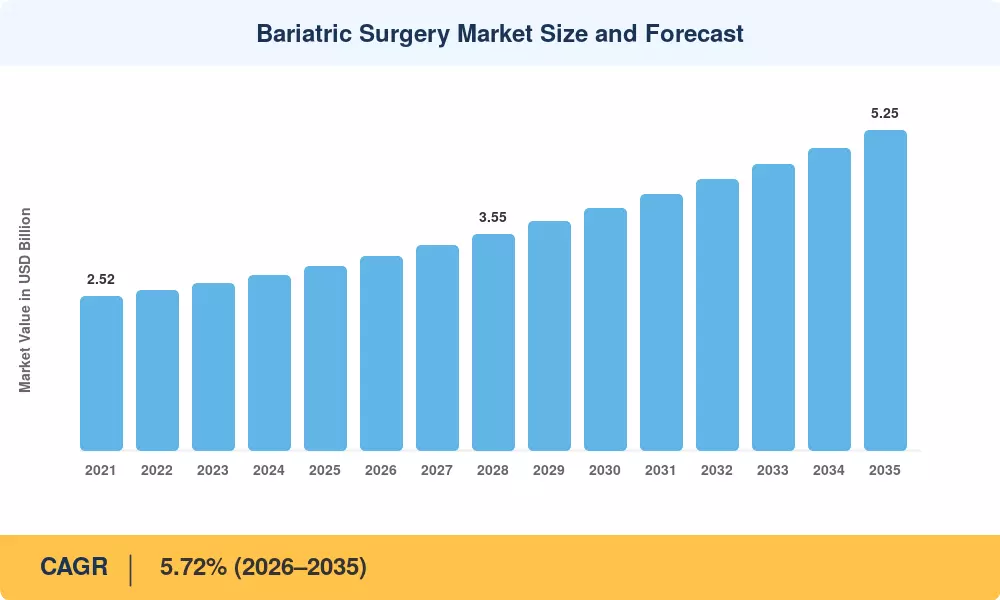

The Bariatric Surgery Market size was valued at USD 3.02 Billion in 2025, and the market is projected to grow from USD 3.18 Billion in 2026 to USD 5.25 Billion by 2035, registering a CAGR of 5.72% during the forecast period 2026–2035. Rising obesity prevalence across both developed and emerging economies—coupled with expanding insurance coverage mandates in over 30 national health systems—has created a durable demand base for surgical weight-management interventions [1]. The World Health Organization's 2024 classification update, which lowered BMI thresholds for intervention eligibility in several Asian populations, further widened the addressable patient pool for the Bariatric Surgery Market [2].

A technology transition is reshaping how providers approach bariatric procedures. Traditional open surgical techniques are giving way to robotic-assisted platforms, single-incision laparoscopic systems, and swallowable intragastric balloon devices that reduce recovery times from weeks to days. Intuitive Surgical's da Vinci platform alone accounted for over 78,000 bariatric cases in 2024, while magnetic compression anastomosis devices entered pivotal trials in the EU, signaling a shift toward sutureless interventions [3]. The U.S. Centers for Medicare & Medicaid Services expanded bariatric procedure reimbursement codes in January 2025, adding an estimated USD 420 million in annual covered spending [4].

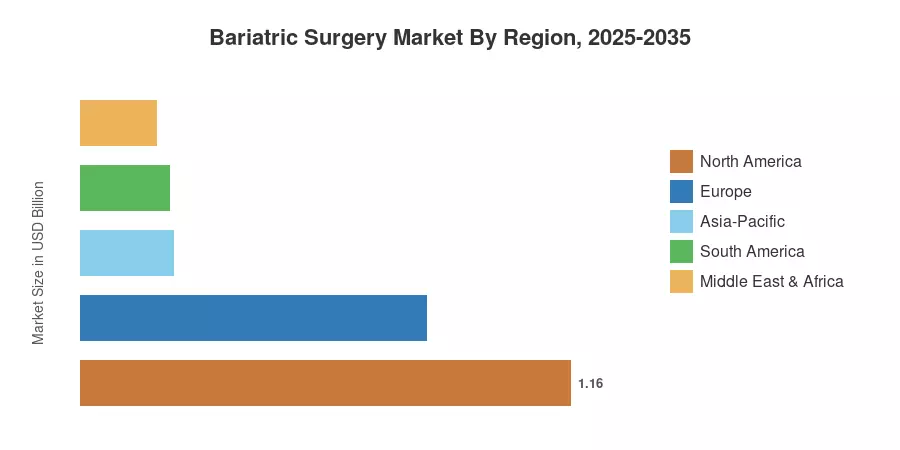

North America commands roughly 38.5% of the global Bariatric Surgery Market, anchored by high procedure volumes in the United States and a mature payer ecosystem. Asia-Pacific stands as the fastest-growing region at a projected 7.32% CAGR, driven by surging obesity rates among younger demographics in China and India. Europe holds the second-largest share at approximately 27%, where national health systems in Germany, the UK, and France are increasingly recognizing bariatric interventions as cost-effective chronic disease prevention. The decade ahead will see the Bariatric Surgery Market evolve from a procedure-driven space into an integrated care platform linking surgical devices with pharmacotherapy and digital health monitoring.

Key Report Takeaways

• By Device Type

- Assisting devices led the Bariatric Surgery Market in 2025 with an estimated 54.2% revenue share, reflecting widespread adoption of stapling, suturing, and energy-based instruments across hospital operating theaters.

- Implantable devices are forecast to register the strongest segment CAGR through 2035, driven by next-generation adjustable gastric bands and intragastric balloon systems gaining regulatory clearance in emerging economies.

• By Procedure Type

- Sleeve gastrectomy accounted for the largest share of total bariatric procedures in 2025, supported by shorter operative times and favorable long-term outcomes data from the STAMPEDE and SLEEVE trials.

- Endoscopic procedures are poised to grow at the fastest pace within the Bariatric Surgery Market, as outpatient-friendly profiles attract ambulatory surgical centers seeking higher case throughput.

• By Region

- North America retained the dominant position in the Bariatric Surgery Market, with the United States contributing the vast majority of regional revenue through robust private-payer coverage and high surgeon density.

- Asia-Pacific is projected to expand at a 7.32% CAGR, as China, India, and ASEAN nations accelerate public health infrastructure investments targeting obesity-related comorbidities.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing model combines bottom-up procedure volume data from 42 national health registries, average device revenue per procedure benchmarks, and top-down cross-validation against manufacturer-reported revenues and payer claims databases. Historical figures reflect actual device shipment values; forecast figures apply a compound annual growth trajectory calibrated to evolving reimbursement policies, technology adoption curves, and demographic obesity projections [1][5].