Battery Energy Storage System (BESS) Market Summary

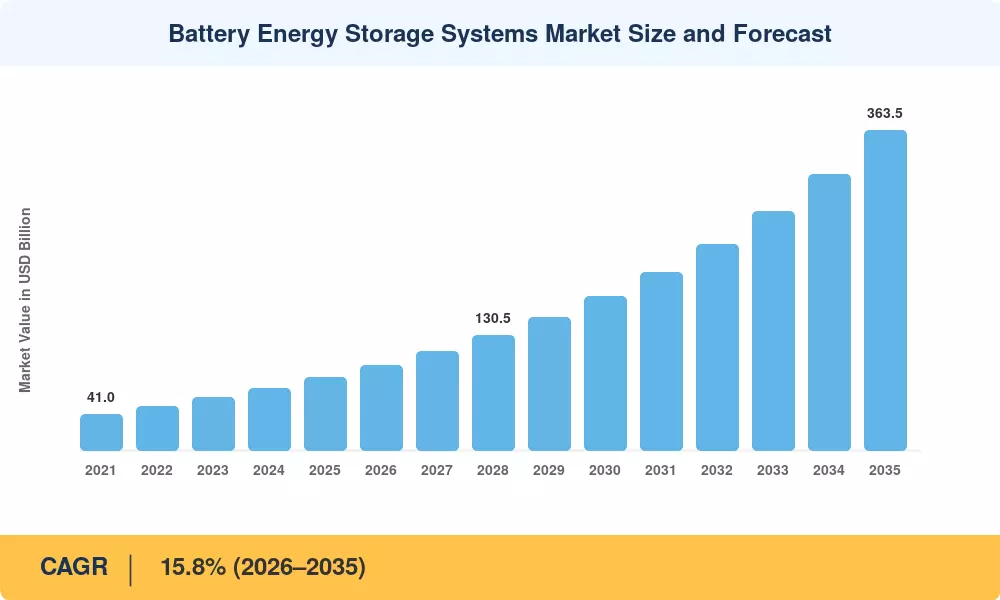

The Battery Energy Storage Systems Market reached an estimated USD 82.80 billion in 2025 and is projected to grow from USD 97.10 billion in 2026 to USD 363.50 billion by 2035, registering a CAGR of 15.8% during the forecast period. Two policy catalysts anchor this trajectory: the Inflation Reduction Act's standalone storage investment tax credit in the United States and the European Union's Net-Zero Industry Act, which together have underwritten multi-gigawatt procurement pipelines across both continents [1][8]. These mandates converted large-scale battery storage from a grid-edge experiment into a bankable infrastructure class practically overnight.

A generational technology shift is underway. Lead-acid and pumped-hydro systems that once dominated stationary storage are yielding to lithium-ion and lithium iron phosphate chemistries that offer faster response, modular scalability, and rapidly falling unit economics. BloombergNEF estimates that lithium-ion pack prices declined by more than 20% year-on-year in 2024, pushing four-hour system costs below USD 150 per kilowatt-hour in several tender markets [11]. Utility procurers now treat the Battery Energy Storage Systems Market as a capacity resource rather than a pilot technology.

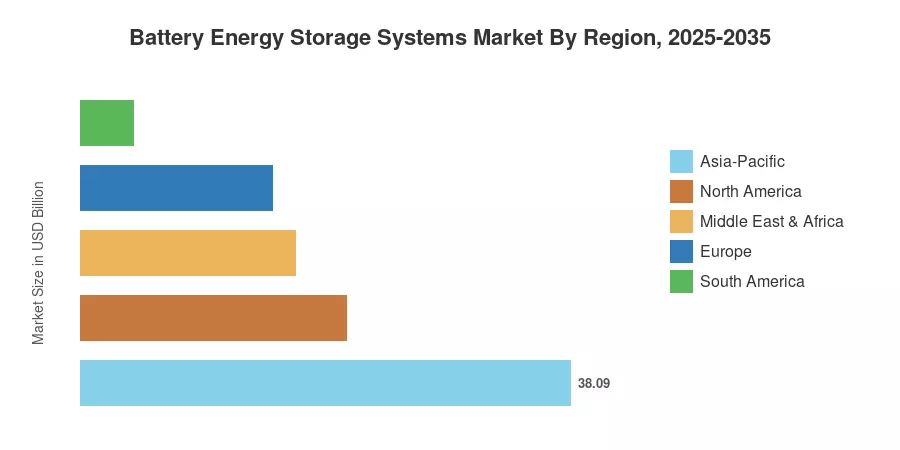

Asia-Pacific commands roughly 46% of the Battery Energy Storage Systems Market, driven by China's dominance in cell manufacturing and aggressive provincial procurement targets [16]. The Middle East & Africa region is the fastest-growing geography at a projected 20.2% CAGR, fueled by Saudi Arabia's Vision 2030 storage mandates and South Africa's loadshedding-driven demand [14]. North America holds the second-largest share at approximately 25%, anchored by interconnection-queue growth and IRA-linked tax incentives [1]. As grid-forming inverter requirements expand revenue streams beyond simple energy arbitrage, the Battery Energy Storage Systems Market is poised to enter a sustained buildout phase through 2035.

Key Report Takeaways

• By Technology (Battery Type)

- Lithium-ion batteries held an 82% share of the Battery Energy Storage Systems Market in 2025, reflecting the chemistry's dominance across utility and commercial applications.

- Lithium Iron Phosphate (LFP) is the fastest-expanding battery segment, forecast at a 20.0% CAGR through 2035, as developers favor its superior cycle life and lower thermal risk.

• By End User

- Utility-scale deployments captured approximately 52% of the Battery Energy Storage Systems Market in 2025.

- Residential storage is advancing at the fastest pace among end-user segments, with an estimated 17.8% CAGR to 2035.

• By Application

- On-grid installations represented 73% of connection-type revenue in 2025, while off-grid applications are expected to expand at 19.5% CAGR.

• By Region

- Asia-Pacific led with a 46% regional share in 2025, while the Middle East & Africa region is forecast to grow at 20.2% CAGR.

- North America accounted for roughly USD 20.70 billion in 2025 market value.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines bottom-up revenue aggregation from tier-one cell manufacturers, EPC contractors, and system integrators with top-down cross-validation against government deployment registries and utility interconnection filings. Historical figures (2021–2024) draw on audited annual reports and customs-trade data; forecast values (2026–2035) apply a scenario-weighted model incorporating policy pipeline analysis, commodity-price trajectories, and disclosed project backlogs [2][6].