Biological Seed Treatment Market Summary

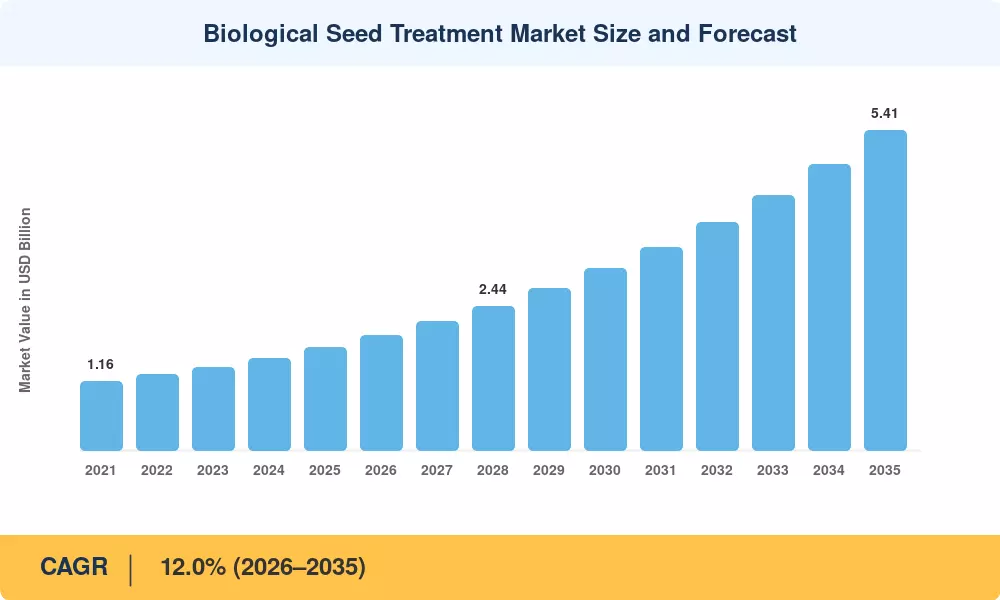

The Biological Seed Treatment Market reached a valuation of USD 1.74 billion in 2025, positioning it as one of the highest-growth corridors in crop protection. From a 2026 starting point of USD 1.95 billion, the market is projected to climb to USD 5.41 billion by 2035 at a 12.0% CAGR — an expansion trajectory driven by tightening pesticide residue limits across the EU and accelerating biotech investment pipelines in China and India [1]. The European Commission's Sustainable Use of Pesticides Directive, which mandates quantifiable reductions in chemical crop inputs, has redirected over EUR 1.7 billion toward biological alternatives, giving the Biological Seed Treatment Market a durable policy tailwind [2].

A generational shift is emerging in how producers maintain seed germination and root growth in their early stages. Legacy chemical dressings — thiram-based fungicides, neonicotinoid coatings — are seeing increasing numbers of registration cancellations. Instead, microbial inoculants and botanical extracts have demonstrated disease-control efficiency rates above 50% in replicated field trials and also improved soil biodiversity indicators [3]. An example of the type of capital commitment that is transforming the Biological Seed Treatment Market supply chain is Corteva Agriscience’s opening of a specialized Center for Seed Applied Technologies laboratory in South Africa in 2022 [4].

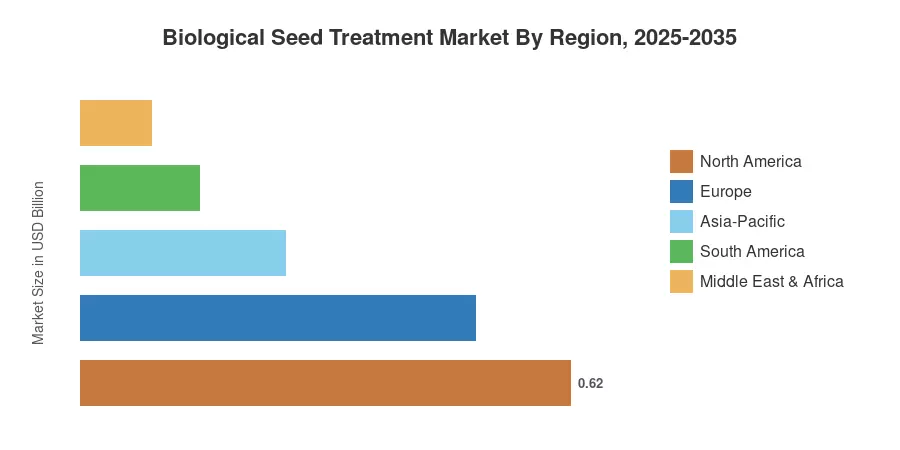

North America, which represents 35.8% of sales, is due to large-row-crop acreage in the US corn heartland and regulatory certainty from the EPA’s biopesticide registration system. The Asia-Pacific area is the fastest expanding region with a predicted CAGR of 14.8% driven by India’s biofertilizer subsidies and China’s green agricultural regulations [5]. Europe is the second greatest share (28.5%) due to the Farm to Fork Strategy’s 50% reduction objective for pesticides by 2030. Biological seed treatment data is integrated into the prescriptive planting algorithms of precision agriculture platforms, and the Biological Seed Treatment Market will continue its double-digit growth through 2035.

Key Report Takeaways

• By Type

- Microbial formulations held a 65.5% share of the Biological Seed Treatment Market in 2024, reflecting grower confidence in strain-specific efficacy data and regulatory fast-tracking for microbial registrations.

- Botanicals are projected to expand at a 15.2% CAGR through 2035, propelled by consumer-facing "residue-free" labeling trends in fresh produce.

• By Function

- Seed protection accounted for 46.0% of the Biological Seed Treatment Market in 2024, driven by fungal and bacterial pathogen pressure in humid growing regions.

- Seed enhancement is the fastest-growing functional segment at a 13.8% CAGR, as plant growth-promoting formulations gain traction in nutrient-depleted soils.

• By Crop Type

- Grains and cereals represented a 42.5% share of the Biological Seed Treatment Market in 2024, reflecting the sheer acreage volume of wheat, corn, and rice globally.

- Vegetables are forecast to grow at a 12.3% CAGR, supported by controlled-environment agriculture mandates that restrict synthetic chemistry.

• By Region

- North America led the Biological Seed Treatment Market with 35.8% revenue share in 2024.

- Asia-Pacific is projected to register the fastest regional CAGR of 14.8% through 2035, driven by government subsidy programs in India and China.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates bottom-up revenue models — aggregating manufacturer shipment data across 35+ countries — with top-down demand modeling calibrated against planted acreage, treatment rates, and average selling prices. Historical figures draw on customs trade databases, company filings, and proprietary distributor surveys. Forecast projections apply a scenario-weighted CAGR that accounts for regulatory, climatic, and competitive variables across the 2026–2035 window.

.webp?v=1785506012)