Biological Skin Substitutes Market Summary

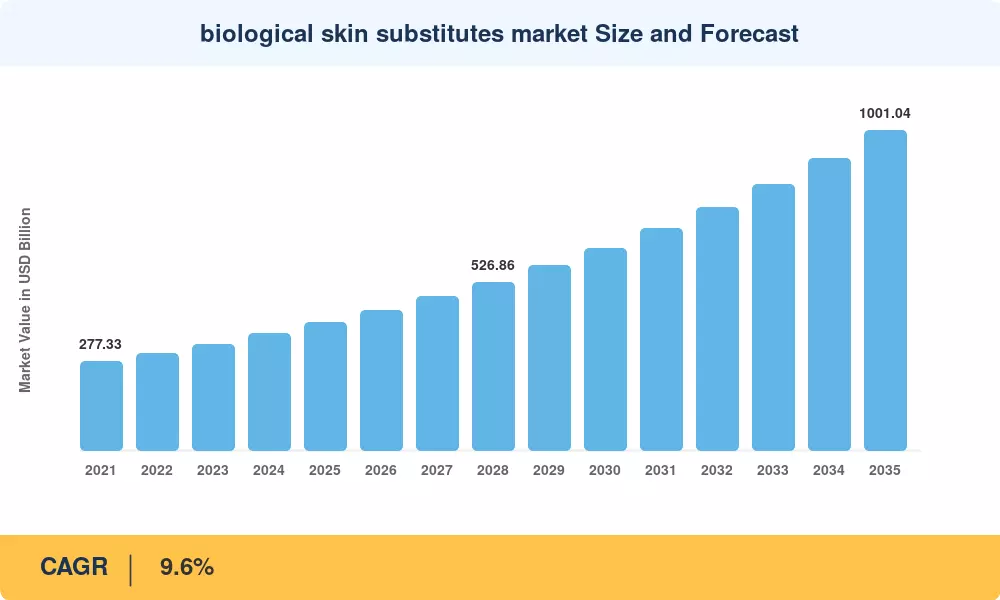

The Global Biological Skin Substitutes Market size was valued at USD 400.16 Million in 2025, and the market is projected to grow from USD 438.58 Million in 2026 to USD 1,001.04 Million by 2035, registering a CAGR of 9.6% during the forecast period 2026–2035. Two catalysts underpin this trajectory: expanding Local Coverage Determinations issued by CMS that increasingly favor products with documented outcomes data [3], and the U.S. Department of Defense's Armed Forces Institute of Regenerative Medicine, which allocated over USD 85 Million in fiscal-year 2024 for battlefield wound-closure research that routinely transitions into civilian burn units [11].

A technology inflection is reshaping the competitive mix. Legacy cadaveric allografts and simple xenografts are yielding shelf space to bioengineered wound dressings built on 3-D bioprinting platforms and autologous cell-harvesting cartridges. Wake Forest Institute for Regenerative Medicine reported a 40% throughput gain in its bioprinted dermal tissue substitutes pilot line during 2024 [14], signaling that scalable manufacturing of regenerative skin products is closer than many procurement teams assume. Regulatory bodies in both the United States and the European Union now maintain expedited evaluation pathways for acellular skin matrices that demonstrate faster re-epithelialization versus standard-of-care grafts [2][5].

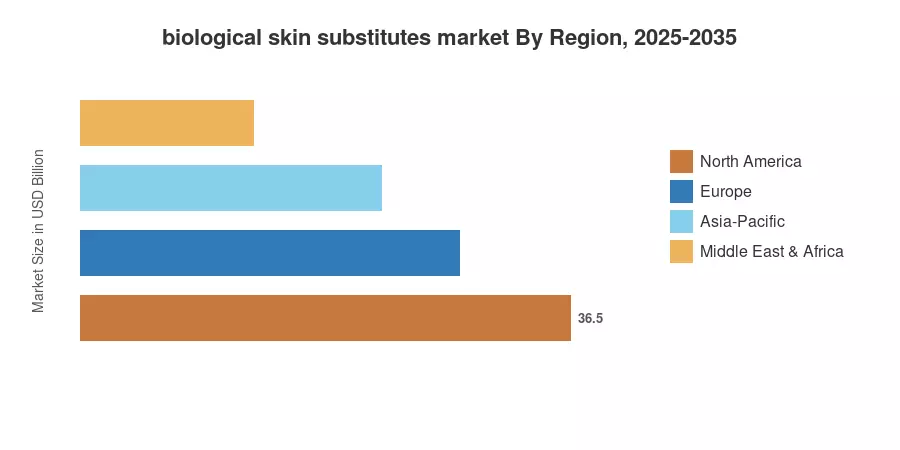

North America anchored the biological skin substitutes market with a 43.1% revenue share in 2024, driven by mature reimbursement frameworks and high burn-center density. Asia-Pacific posts the fastest regional expansion at a 13.4% CAGR through 2035, fueled by hospital infrastructure investment across China and India Europe held the second-largest share at 26.4%, supported by harmonized EMA pathways for advanced-therapy medicinal products. The decade ahead will favor companies that pair clinical evidence with cost-effectiveness dossiers tailored to value-based purchasing committees.

Key Report Takeaways

• By Source Material

- Human allografts commanded a 45.9% revenue share of the biological skin substitutes market in 2024, sustained by organ-procurement network expansions

- Cell-based constructs are forecast to post a 14.5% CAGR through 2035, powered by autologous keratinocyte spray systems

• By Product Type

- Acellular skin matrices captured 44.6% of the biological skin substitutes market in 2024, reflecting strong wound-center adoption

- Bioengineered 3-D printed skin leads product-type growth at a 19.7% CAGR to 2035

• By Application

- Burns accounted for 43.2% of total demand in 2024, underpinned by national burn-center referral networks

- Pediatric congenital-defect coverage expands at a 16.8% CAGR, the fastest application-level rate

• By End User

- Hospitals held 59.2% of the end-user share, anchored by inpatient burn-unit protocols

- Military and defense facilities register a 15.9% CAGR, the quickest end-user growth rate through 2035

• By Region

- North America generated 43.1% of global revenue in the biological skin substitutes market

- Asia-Pacific is expanding at a 13.4% CAGR, the fastest among all regions

Market Size and Forecast (2021–2035)

MRFR's sizing methodology blends top-down revenue analysis of key manufacturer filings with bottom-up unit-volume tracking across 14 product classes. Historical figures (2021–2024) are reconciled against FDA 510(k)/PMA clearance databases and CMS billing data; forecast values apply a multi-factor regression anchored to demographic burn-incidence projections, reimbursement-expansion scenarios, and technology-penetration curves[17].

.webp?v=1782976094)