Biscuits Market Summary

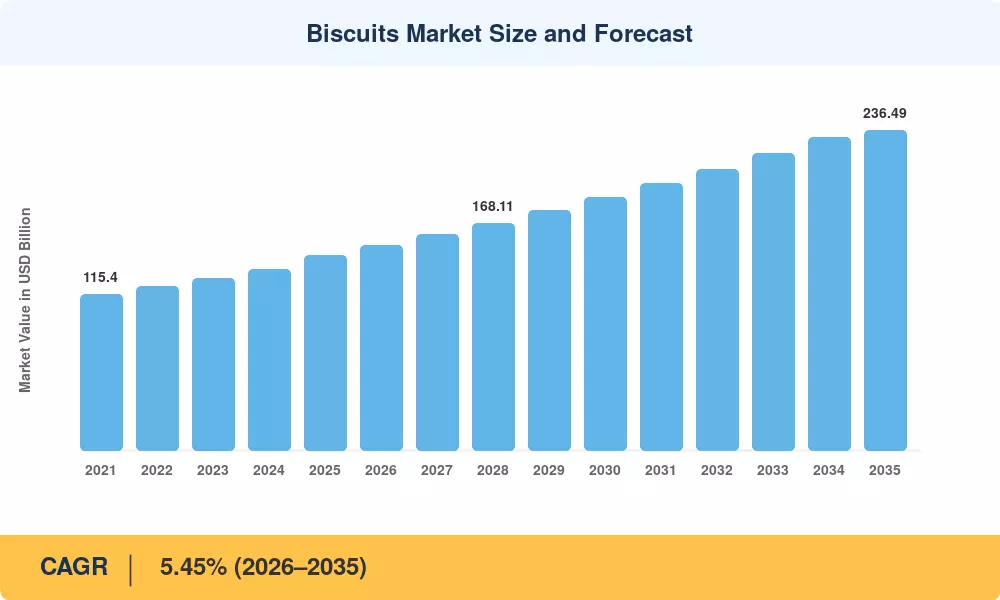

The Biscuits Market reached an estimated USD 143.82 Billion in 2025, with the forecast period beginning at USD 151.18 Billion in 2026 and climbing to USD 236.49 Billion by 2035 at a CAGR of 5.45%. This trajectory reflects sustained household consumption habits, rapid urbanization across developing economies, and government-backed nutrition fortification programs that have drawn both multinational and regional producers into reformulation drives. Rising disposable incomes — particularly in Asia-Pacific and South America — have turned sweet-savory biscuit snack categories into everyday staples rather than occasional indulgences.

Manufacturers across the Biscuits Market are overhauling legacy production lines to accommodate whole grain digestive biscuit formulations, reduced-sugar variants, and fiber-enriched recipes. Mondelēz International alone committed over USD 1.2 billion in capital expenditure between 2023 and 2025 to modernize baking facilities in India, Brazil, and Eastern Europe [2]. Meanwhile, premium artisan biscuit brand portfolios have expanded rapidly through direct-to-consumer e-commerce channels, bypassing traditional retail gatekeepers and capturing higher per-unit margins.

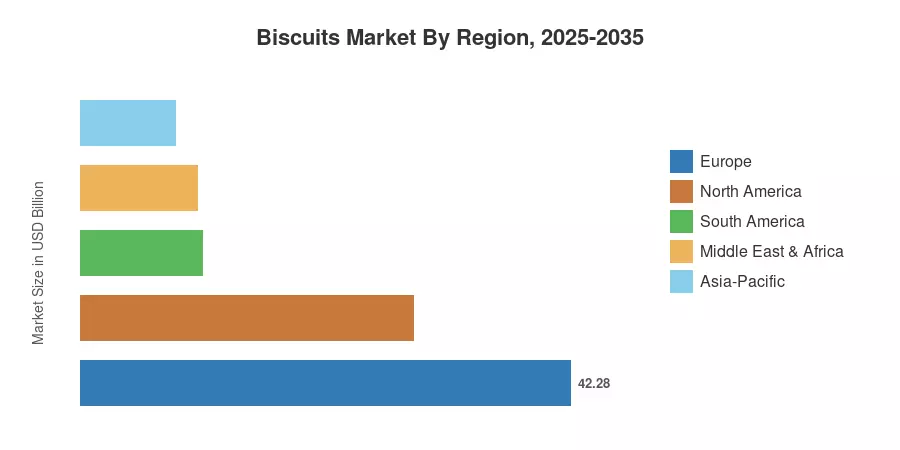

Europe dominated the Biscuits Market with approximately 29.4% of global revenue in 2025, underpinned by deeply rooted tea-time and snacking cultures in the UK, France, and Germany South America emerged as the fastest-growing region at a projected 7.32% CAGR through 2035, fueled by middle-class expansion in Brazil and Argentina. Asia-Pacific held the second-largest share at roughly 26.8%, driven by India and China's massive consumer bases and growing appetite for gluten-free biscuit alternative products. The next decade promises intensifying competition as biscuit packaging innovation and single-serve formats reshape how consumers discover and purchase biscuits globally.

Key Report Takeaways

• By Product Type

- Sweet biscuits commanded a 76.8% revenue share of the Biscuits Market in 2025, anchored by chocolate-coated and cream-filled subcategories

- Crackers and savory biscuits are forecast to advance at a 6.65% CAGR through 2035, reflecting the shift toward lower-sugar sweet savory biscuit snack options

• By Category

- Conventional wheat-based SKUs captured 90.1% of the Biscuits Market in 2025, though growth is decelerating as health-aware shoppers explore alternatives

- Free-from options — including gluten-free biscuit alternative products — are expanding at a 6.72% CAGR between 2026 and 2035

• By Distribution Channel

- Supermarkets and hypermarkets accounted for USD 66.93 billion of the Biscuits Market in 2025

- Online retail is climbing at an 8.52% CAGR to 2035, with single-serve and premium artisan biscuit brand offerings leading digital penetration

• By Region

- Europe held a 29.4% share of the Biscuits Market in 2025

- South America is on course for the fastest CAGR at 7.32% over 2026–2035, while Asia-Pacific contributed USD 38.54 Billion in 2025

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates primary interviews with 120+ industry participants, secondary validation through customs trade data, production volume tracking, and company financials. Historical estimates (2021–2024) rely on audited data; the 2025 base year blends preliminary actuals with modeled estimates; and the forecast (2026–2035) applies a bottom-up segmental build calibrated against macroeconomic indicators.

.webp?v=1785231586)