Download Free Sample

Kindly complete the form below to receive a free sample of this Report

Blenders Market Research Report Information by Product Type (Countertop Blenders, Personal and Portable Blenders, Immersion and Hand Blenders, Commercial and Heavy-Duty Blenders), By Power Rating (Up To 300 Watts, 300–600 Watts, 600–900 Watts, above 900 Watts), By Material (Plastic, Glass, Stainless Steel) By Price Range (Mass (Less Than $60, Mid ($60–$150), Premium ($150–$350), High-End ($350–$700 And Above)) By End User (Consumer Or Personal, Professional Or Commercial[Foodservice, Smoothie Shops, QSR, Cafés], Hospitality, Institutional) By Distribution Channel(Brick-And-Mortar Retail, Specialty Or Kitchen Stores, Online Or E-Commerce, Direct-To-Consumer (DTC))By Region (North America, Europe, Asia Pacific, South America, Middle East & Africa) - Forecast to 2035

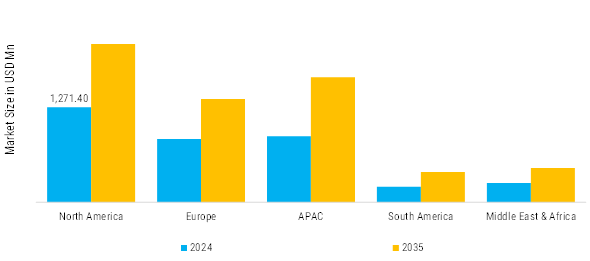

As per Market Research Future analysis, Blenders Market Size was valued at USD 3,470.0 million in 2024. The Blenders Industry is projected to grow from USD 3,641.8 million in 2025 to USD 6,040.2 million by 2035, exhibiting a compound annual growth rate (CAGR) of 5.19% during the forecast period (2025 - 2035).

The Blenders Market is trends show strong growth fueled by health trends, tech innovations, and e-commerce expansion.

| 2024 Market Size | 3,470.0 (USD Million) |

| 2035 Market Size | 6,040.2 (USD Million) |

| CAGR (2025 - 2035) | 5.19% |

Sharkninja / Ninja, Philips (Versuni), Kitchenaid (Whirlpool), Hamilton Beach, Vitamix, Cuisinart (Conair), Panasonic Corporation, Nutribullet (Capital Brands), Blendtec.

Our Impact

Enabled $4.3B Revenue Impact for Fortune 500 and Leading Multinationals

Partnering with 2000+ Global Organizations Each Year

30K+ Citations by Top-Tier Firms in the Industry

The Smart technology is revolutionizing the blender market with Wi-Fi and Bluetooth-enabled models that allow remote operation via mobile apps. These devices feature preset blending programs, real-time monitoring, and automatic shut-off for convenience and safety. Integration with digital assistants like Alexa or Google Home enhances functionality, while data-driven insights optimize performance. Consumers increasingly prefer intelligent appliances that simplify healthy meal preparation, reflecting the growing demand for kitchen automation.

Online retail has become a major growth driver for blender sales, offering consumers access to diverse brands and competitive pricing. E-commerce platforms enable product comparisons, customer reviews, and direct-to-consumer discounts, improving buyer confidence. Brands are leveraging digital marketing, influencer collaborations, and social media campaigns to reach tech-savvy audiences. This shift toward online engagement has expanded blender accessibility globally, particularly in emerging markets.

The foodservice industry—comprising cafés, juice bars, and quick-service restaurants—continues to fuel demand for commercial-grade blenders. These high-performance models are designed for continuous use, larger capacities, and heavy-duty blending. As global café culture expands and demand for fresh beverages rises, businesses are investing in durable, energy-efficient appliances to enhance service speed and consistency.

Portable blenders have become one of the fastest-growing product segments, driven by modern lifestyles that value mobility and convenience. Compact, rechargeable, and easy to carry, these blenders cater to health-conscious consumers who prepare smoothies and protein shakes on the go. The increasing fitness and travel culture, along with improvements in battery life and USB-charging capabilities, have made them essential for single-serve blending.

In the short term (2025–2027), innovation-driven demand will focus on compactness, user-friendly features, and improved portability. The growing number of young professionals and single-person households is creating a strong market for personal and portable blenders that offer convenience and mobility. Consumers are also drawn to products that enhance lifestyle appeal through smart design and multi-functionality. Leading companies such as Vitamix, Ninja, and NutriBullet are incorporating advanced motor technology, app-controlled functions, and pre-programmed blending modes that deliver consistent results with minimal effort. For example, several new blenders launches feature Bluetooth connectivity and companion apps that allow users to adjust blending speeds or choose recipes remotely. These innovations address time constraints while enhancing customization, making them appealing to consumers who want both performance and convenience. Online platforms and social media influencers are amplifying this trend by showcasing quick, nutritious recipes prepared with modern blenders, encouraging broader adoption.

In the near term, as new restaurants, cafés, juice bars, ghost kitchens, and expanded menus continue to open, especially in emerging economies, demand for commercial and high-performance blenders will spike sharply. Entrepreneurs launching new outlets often budget for key appliances early, driving capital purchases of commercial-grade blenders even before full throughput is achieved. For example, juice bar chains expanding rapidly in Asia and Latin America will order batch quantities of high-wattage blender systems to standardize equipment. This surge can lead to inventory shortages in premium models and longer lead times, pushing margins upward. Manufacturers will prioritize orders for foodservice channels, potentially compressing supply for consumer lines. Retailers may bundle consumer models with commercial-grade sister units or accessories to capitalize on the excitement of new outlet growth. In sum, the short-term effect is a step-function increase in blender unit sales tied to outlet expansion.

The rising trend of health consciousness is becoming a defining catalyst for growth in the Blenders Market, as consumers increasingly associate blending with wellness, nutrition, and convenience. The global health and wellness food sector is estimated to surpass USD 1.5 trillion by 2025, with smoothies, protein shakes, and plant-based diets accounting for a growing share of daily consumption. This shift in dietary habits is directly fueling demand for blenders, which are viewed as essential tools for preparing nutrient-rich beverages and meals. Consumers are becoming more aware of the benefits of natural, homemade nutrition over processed foods, and blenders provide a simple way to integrate fruits, vegetables, and superfoods into daily diets. As a result, manufacturers are innovating with product features tailored to health-focused users, such as nutrient retention technologies, precision blending controls, and multi-functionality for various dietary needs.

In the Blenders Market, the segment is predominantly led by Countertop Blenders, which command a significant share of the market due to their versatility and efficiency. They cater to a wide range of consumers, from home cooks to professional chefs, allowing them to handle various blending tasks with ease. Personal Blenders, while smaller in market share, are gaining traction among health-conscious individuals looking for convenience and portability in their daily routines. This shift is reflective of changing lifestyle preferences that favor on-the-go solutions.

Countertop Blenders (Dominant) vs. Personal Blenders (Emerging)

Countertop Blenders are recognized for their robust performance and large capacity, making them ideal for families and culinary enthusiasts. They often come equipped with advanced features, such as programmable settings and multiple speed options. On the other hand, Personal Blenders represent an emerging trend towards compact design and practicality, perfect for singles or small households. These blenders are particularly favored for their ability to create smoothies and single-serve drinks quickly, appealing to the increasing demand for healthy beverages. This contrast highlights the evolving preferences of consumers, balancing between traditional blending capabilities and the desire for convenience and health.

The Blenders Market showcases a diverse material composition where Plastic holds the largest share, attributed to its affordability, lightweight nature, and versatile applications. Stainless Steel is also gaining traction, particularly in high-end models, due to its durability and aesthetic appeal, while glass and other materials like aluminum and copper account for smaller portions of the market. The demand for high-quality and durable blenders is influencing consumer preferences, creating shifts in market shares among these material types. Growth trends indicate a significant shift towards stainless steel as consumers seek longevity and maintenance-friendly products. This push is driven by the rising health consciousness and a preference for materials perceived as safer and more robust. Plastic remains appealing for entry-level options, but innovations in stainless steel manufacturing are bolstering its position as a preferred choice for premium offerings, indicating a dynamic shift in consumer priorities.

Plastic (Dominant) vs. Stainless Steel (Emerging)

In the Blenders Market, Plastic is the dominant material, favored for its cost-effectiveness and lightness, making it ideal for budget-conscious consumers. With a wide array of colors and designs, plastic blenders appeal to a diverse demographic. On the other hand, Stainless Steel is emerging as a preference among discerning buyers due to its exceptional durability, resistance to corrosion, and modern aesthetic. As consumers increasingly prioritize quality and food safety, stainless steel blenders are gaining momentum. This duality in material choice underscores differing consumer segments: the plastic segment thrives on affordability, while stainless steel appeals to those seeking premium, long-term investments in kitchen appliances.

In the Blenders Market, the power segment exhibits a diverse range of wattages, impacting both performance and consumer preference. The > 1,000 Watts segment commands the largest market share, favored by consumers seeking higher efficiency and versatility in blending tasks. Following closely, the 700 to 999 Watts category is gaining traction among health-conscious consumers and culinary enthusiasts, leveraging technology that delivers superior blending results for recipes requiring more power.

> 1,000 Watts (Dominant) vs. 700 to 999 Watts (Emerging)

The > 1,000 Watts power segment stands out as the dominant force in the Blenders Market, appealing to professional chefs and serious home cooks. This category's blenders are typically equipped with advanced motor technology, enabling superior performance in handling tough ingredients, thereby facilitating a smooth blending experience. In contrast, the 700 to 999 Watts segment is emerging rapidly, attracting new customers who desire a balance of power and affordability. This emerging group is characterized by models that provide effective blending without the premium price associated with higher wattages, making them popular among everyday users.

The Blenders Market exhibits a significant division in sales channels, with the Offline Channel holding a majority share. Traditional retail outlets such as appliance stores, department stores, and specialty kitchenware shops continue to dominate sales, benefiting from immediate product access and customer support. However, the Online Channel is progressively capturing a broader audience as consumers increasingly prefer the convenience of online shopping. This shift has led to more brands investing in e-commerce strategies, enhancing product availability via digital platforms. In recent years, the Online Channel has emerged as the fastest-growing segment within the Blenders Market, driven by the surge in online shopping and a growing preference for home delivery. Factors such as the rise of e-commerce, availability of customer reviews, and promotional offers have encouraged shoppers to seek blenders online. Moreover, the influence of social media and online marketing has boosted consumer awareness, leading to greater demand for diverse product offerings available through online retailers.

Sales Channel: Offline Channel (Dominant) vs. Online Channel (Emerging)

The Offline Channel remains dominant in the Blenders Market, characterized by established retail networks that allow consumers to physically evaluate products before purchase. This segment thrives on customer trust and brand loyalty, providing immediate customer service and support. Many consumers enjoying the sensory experience of hands-on trials prefer this method of shopping, especially for high-investment appliances like blenders. However, the Online Channel is rapidly emerging, catering to tech-savvy consumers who appreciate the convenience of shopping from home. This segment features enhanced product visibility, competitive pricing, and the ability to explore extensive options. The growth in this channel is propelled by factors such as trend analysis through online reviews, targeted marketing campaigns, and flexibility in purchasing options that appeal to the modern consumer.

Based On Distribution Channel, Brick-and-Mortar Retail, Specialty or Kitchen Stores, Online or E-commerce, Direct-to-Consumer (DTC). This channel thrives on experiential selling, expert consultations, and brand-led demonstrations. Specialty retailers cater to affluent consumers, culinary enthusiasts, and professional buyers seeking high-quality materials, motor durability, and design aesthetics. Products most often sold here include high-wattage countertop blenders, stainless-steel jar commercial models, and quiet-operation premium blenders from brands like Vitamix, Breville, Blendtec, and KitchenAid. Specialty stores also drive accessory sales—spare jars, tampers, and blades—contributing to higher margins. End-users include prosumers, small restaurants, hotels, smoothie chains, and cooking schools, who often prefer in-store demos to evaluate performance before large investments. Brands like Vitamix, Breville, Blendtec, SMEG, Bosch, Kenwood, and Electrolux Professional use this channel to communicate craftsmanship and innovation. Major retail partners include Williams Sonoma, Sur La Table, Crate & Barrel, John Lewis, Lakeland, Darty, and Currys. Growth is driven by the increasing global appetite for gourmet and health-conscious lifestyles, coupled with rising premium kitchen appliance adoption in Asia-Pacific. The channel’s future lies in interactive displays, AI-assisted product selectors, and chef-partnered workshops that blend education with commerce, allowing high-margin players to build loyalty and brand prestige.

Based on Product Type, the Blenders Market has been segmented into: -Personal and portable blenders, Immersion and Hand Blenders, Commercial and Heavy-Duty Blenders. First is versatility: full-size jars and high-torque motors handle smoothies, soups, frozen desserts, nut butters, sauces, and meal-prep tasks better than smaller formats. Second is continued feature migration from commercial lines—variable-speed control, preset programs, jar vortex optimization, brushless motors, thermal/overload protection, and quieter housings—all of which improve texture consistency while shrinking cycle time and perceived noise. Demand is tied to foodservice scale—smoothie bars, cafés, QSR beverage stations, hotels, resorts, and institutional kitchens. Growth levers: throughput and consistency (programmable cycles, tamperless jar designs), noise management for open counters (acoustic hoods, suspended motors), and durability (heavy bearings, reinforced couplings, thermal management for continuous duty). Operators seek predictable texture across staff shifts, so menu-linked presets and auto-stop reduce variability and training time. Increasingly, chains want telemetry/predictive maintenance that logs cycle counts and heat events, enabling proactive service to minimize downtime. End-use is entirely professional/commercial; ROI is measured by speed of service, drink yield, and uptime.

Get more detailed insights about Blenders Market Request Free Sample

North America: Expanding Consumers trade

The North American Consumers trade up for quieter housings, variable-speed control, and self-clean cycles, while prosumers gravitate toward near-commercial results at home (600–900 W and 900 W+ tiers). Commercial buyers emphasize throughput, consistency, and acoustic control for open counters. Distribution is omnichannel: specialty/kitchen stores and DTC drive premium discovery and service plans; e-commerce has become a default research and replenishment path; big-box retail moves volume in mass and mid segments. Materials skew BPA-free plastics and Tritan jars for portability and impact resistance, with glass popular in design-centric households and stainless prominent in foodservice.

Europe: Emerging high cooking frequency

The region’s blender demand is shaped by compact urban kitchens, high cooking frequency, and a strong culture of soups, sauces, and purées that favors immersion wands alongside countertop models. Consumers focus on energy efficiency, safety, and design, with glass jars and stainless shafts popular given Europe’s hygiene and durability preferences. Regulations around eco-design, recyclability, and product safety reinforce shifts toward efficient motors, longer warranties, and repairability. Premiumization is steady—quieter, better-finished appliances with multi-function kits—and specialty retail remains influential for demonstrations and attachment upsells, while e-commerce accelerates cross-border access to niche brands. Commercial demand is healthy in cafés, boutique hospitality, and bakery/café hybrids seeking consistency and lower noise. Growth is supported by renovation cycles, electrification of small appliances in Eastern Europe, and wellness culture spreading beyond early-adopter markets.

Asia-Pacific: Development of modern retail and e-commerce

The Asia-Pacific is rapid urbanization, expansion of modern retail and e-commerce, rising disposable incomes, and a young, digital-first consumer base eager for portable, affordable appliances. The region’s culinary diversity drives distinct use cases—from soy/plant-milk and hot-blend soups to fruit-ice smoothies—supporting both personal/portable formats (≤300 W) and mid-power countertop units (300–900 W). India’s juicer-mixer-grinder heritage boosts prosumer adoption in the 600–900 W band; China’s social commerce and live-stream retail accelerate new-brand trial; Japan and Korea favor quiet, compact, and high-precision builds. Commercial demand expands with café chains, bubble-tea and smoothie concepts, and QSR beverage programs in malls and transit hubs. Procurement is heavily online for consumers (marketplaces, live-stream deals) and increasingly DTC for premium and commercial specs. Materials skew to Tritan/polycarbonate for impact resistance and portability.

Middle Eat & Africa: Emerging youthful demographics

Middle East and Africa (MEA) demand is increasingly shaped by youthful demographics, expanding modern trade, and the proliferation of cafés, juice bars, and casual dining across GCC cities and North African hubs. Households adopt mid-range countertop blenders for smoothies, soups, and regional sauces; portables gain traction among office workers and students; immersion wands assist compact urban kitchens. In the Gulf, premiumization is visible in design-forward appliances and quieter housings; in North and Sub-Saharan Africa, value and mid-tier units dominate, with e-commerce and social commerce widening access beyond major cities. Commercial buyers in hospitality and QSRs emphasize durability, service coverage, and quick-clean designs suited to high ambient temperatures and long hours. Retail is a mix of hypermarkets, electronics chains, specialty stores, and fast-growing online marketplaces.

South America: Emerging e-commerce and digital payments

South America is demand is anchored in Brazil, Mexico, Argentina, Chile, and Colombia, where home blending is strongly associated with fruit-based beverages and cooking prep. Growth is powered by rising middle-class consumption, the normalization of e-commerce and digital payments, and retailer private-label programs that broaden affordability. Mass and mid-range countertop models dominate, typically with plastic/Tritan jars for lightness and resilience, while immersion blenders gain share in compact kitchens. Portables see rapid uptake among students and young professionals. Commercial demand is steady in juice bars, bakeries, and cafés, with higher-wattage units adopted by QSR beverage counters in malls. Sales channels vary by country: hypermarkets and appliance chains move volume, while marketplaces (Mercado Libre and retailer.com sites) expand reach and price transparency. Currency swings and import duties can influence ASPs, making locally assembled or regional brands particularly competitive.

Many global, regional, and local vendors characterize the Blenders Market. The market is highly competitive, with all the players competing to gain market share. Intense competition, rapid advances in technology, frequent changes in government policies, and environmental regulations are key factors that confront market growth. The vendors compete based on cost, product quality, reliability, and government regulations. Vendors must provide cost-efficient, high-quality products to survive and succeed in an intensely competitive market.The major players in the market Include Sharkninja / Ninja, Philips (Versuni), Kitchenaid (Whirlpool), Hamilton Beach, Vitamix, Cuisinart (Conair), Panasonic Corporation, Nutribullet (Capital Brands), Blendtec strategic market developments and decisions to improve operational effectiveness.

May 2025: SharkNinja has built its growth strategy on a strong foundation of innovation, consumer-centric design, and product diversification. The company focuses heavily on understanding evolving consumer needs, particularly in modern households that prioritize speed, convenience, and multifunctionality. By integrating intelligent blending systems, multiple attachments, and smart control features, SharkNinja has established itself as a brand that simplifies complex culinary tasks. A major strategic pillar has been the expansion of its Ninja sub-brand into a versatile kitchen ecosystem that includes food processors, beverage makers, and air fryers—allowing it to cross-leverage consumer loyalty across categories.

January 2025: Philips, now operating under the home appliance entity Versuni, has adopted a strategy rooted in technological innovation, energy efficiency, and wellness integration. The company focuses on creating appliances that combine functionality with health benefits, appealing to consumers increasingly concerned about nutrition and sustainability. In its blender segment, Philips leverages proprietary technologies like ProBlend and vacuum blending systems to enhance texture, nutrient retention, and blending consistency. A major part of its growth strategy is centered around digital transformation, integrating smart features such as app connectivity, recipe guidance, and automatic blending programs. Philips also places heavy emphasis on sustainability, designing energy-efficient motors, recyclable components, and durable build quality to extend product lifecycles. Versuni has been strengthening e-commerce distribution by partnering with platforms like Amazon and developing direct sales through brand-owned online stores.

May 2025: KitchenAid’s strategy is anchored in premium craftsmanship, design-led innovation, and heritage branding. As a division of Whirlpool Corporation, KitchenAid capitalizes on its iconic reputation for durability and performance to maintain dominance in the high-end blender segment. The company focuses on blending aesthetics with functionality—its blenders feature robust motors, metal bodies, and customizable finishes that appeal to both professional chefs and design-conscious consumers. KitchenAid’s strategy centers on sustaining a premium identity, avoiding overexposure in the mass market to preserve its luxury positioning. Its product innovation roadmap focuses on performance upgrades, including improved speed controls, blending precision, and energy efficiency.

The Blenders Market is projected to grow at a 5.19% CAGR from 2025 to 2035, driven by increasing demand for high-performance computing and enhanced security features.

New opportunities lie in:

By 2035, the Blenders Market is expected to achieve robust growth, reflecting evolving consumer preferences and innovation.

|

Market Size 2024 |

3,470.0 (USD Million) |

|

Market Size 2025 |

3,641.8 (USD Million) |

|

Market Size 2035 |

6,040.0 (USD Million) |

|

Compound Annual Growth Rate (CAGR) |

5.19% (2025 - 2035) |

|

Report Coverage |

Revenue Forecast, Competitive Landscape, Growth Factors, and Trends |

|

Base Year |

2024 |

|

Market Forecast Period |

2025 - 2035 |

|

Historical Data |

2019 - 2023 |

|

Market Forecast Units |

USD Million |

|

Key Companies Profiled |

Sharkninja / Ninja, Philips (Versuni), Kitchenaid (Whirlpool), Hamilton Beach, Vitamix, Cuisinart (Conair), Panasonic Corporation, Nutribullet (Capital Brands), Blendtec |

|

Segments Covered |

By Product Type, By Power Rating, By Material, By Price Range, By End User, By Distribution Channel |

|

Key Market Opportunities |

Expansion Of E-Commerce Platforms Offering Greater Accessibility to Blenders. Growing Trend of Meal Prep and Smoothie Culture Creating New Customer Segments. Development Of Smart Blenders Integrated with Technology for Convenient Usage. |

|

Key Market Dynamics |

Growth Of the Foodservice Industry Supporting Elevated Sales of Blenders. Increasing Demand for Innovative Kitchen Appliances Among Consumers. Rising Trend of Health Consciousness Leading to Higher Usage of Blenders for Nutritious Foods. |

|

Region Covered |

North America, Europe, APAC, South America, MEA |

The Blenders Market was valued at 3.472 USD Billion in 2024.

The Blenders Market is projected to reach a valuation of 6.065 USD Billion by 2035.

The expected CAGR for the Blenders Market during the forecast period 2025 - 2035 is 5.2%.

In 2024, Countertop Blenders had the highest valuation at 2.5 USD Billion.

In 2024, online sales were valued at 1.972 USD Billion, while offline sales were at 1.5 USD Billion.

Kindly complete the form below to receive a free sample of this Report

“This is really good guys. Excellent work on a tight deadline. I will continue to use you going forward and recommend you to others. Nice job”

“Thanks. It’s been a pleasure working with you, please use me as reference with any other Intel employees.”

“Thanks for sending the report it gives us a good global view of the Betaïne market.”

“Thank you, this will be very helpful for OQS.”

“We found the report very insightful! we found your research firm very helpful. I'm sending this email to secure our future business.”

“I am very pleased with how market segments have been defined in a relevant way for my purposes (such as "Portable Freezers & refrigerators" and "last-mile"). In general the report is well structured. Thanks very much for your efforts.”

“I have been reading the first document or the study, ,the Global HVAC and FP market report 2021 till 2026. Must say, good info! I have not gone in depth at all parts, but got a good indication of the data inside!”

“We got the report in time, we really thank you for your support in this process. I also thank to all of your team as they did a great job.”

“The Automotive 48V ECU Components Procurement Intelligence Study” was a complex project, but the Market Research Future (MRFR) team handled it with quality, agility, and customer-centricity. They delivered all requested data on time and within the agreed scope. The team, including Shubhendra Anand and Rahul Gotadki, was always readily available to clarify questions and swiftly implement necessary adjustments, driving the project to a successful conclusion within a very demanding timeframe.

I would also like to specifically commend Akshay Agarwal for his responsiveness and support at every stage—from our initial inquiry on May 6th through to final delivery on June 18th. His dedication made the entire process seamless.”