Body Contouring Market Summary

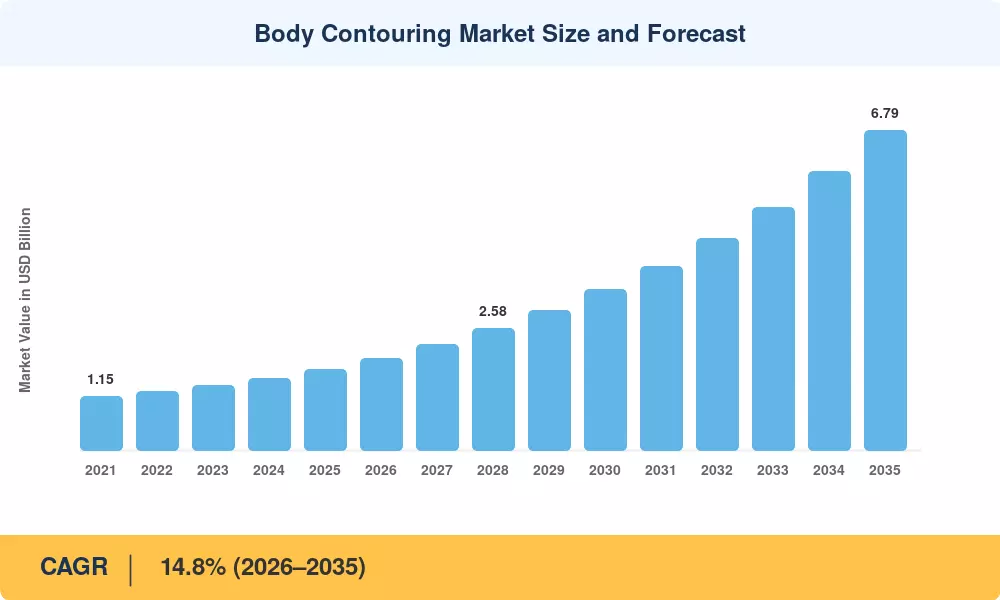

The Body Contouring Market reached USD 1.71 billion in 2025 and is projected to grow from USD 1.96 billion in 2026 to USD 6.79 billion by 2035, advancing at a 14.8% CAGR through the forecast window. Rising disposable incomes across middle-income demographics and the normalization of aesthetic procedures among adults aged 25–40 are the twin catalysts behind this expansion. Regulatory bodies in the United States and European Union have accelerated clearance pathways for energy-based devices, trimming average approval timelines by roughly 15–20% since 2022 [1].

A technology shift is reshaping the Body Contouring Market from single-modality surgical tools toward multi-application, AI-calibrated platforms that combine fat reduction, tissue tightening, and muscle stimulation in one session. Legacy vacuum-assisted liposuction systems are steadily giving ground to cryolipolysis, radiofrequency, and high-intensity focused electromagnetic (HIFEM) combinations. Global aesthetic-device capital expenditure exceeded USD 8.4 billion in 2024, reflecting provider confidence in next-generation hardware.

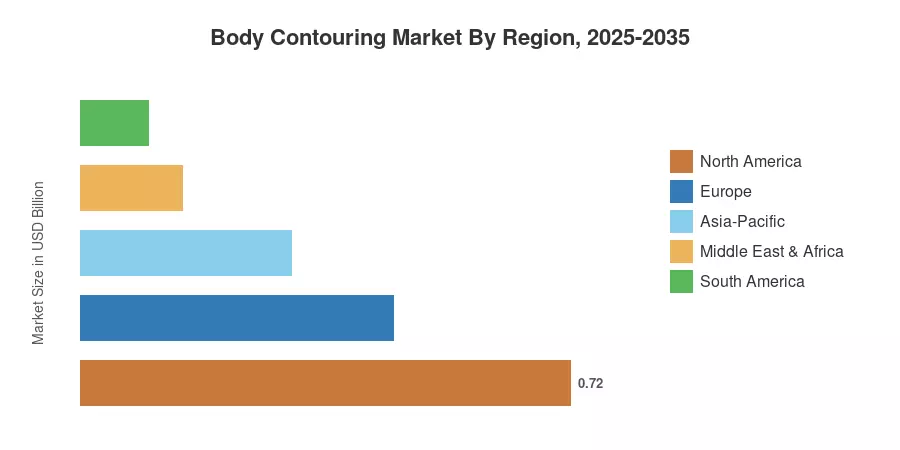

North America commanded roughly 42% of Body Contouring Market revenue in 2025, underpinned by mature medical-spa infrastructure and high consumer awareness. Asia-Pacific is the fastest-growing region at an 18.3% CAGR, fueled by expanding insurance-adjacent wellness spending in China, South Korea, and India. Europe held the second-largest share at approximately 27%, driven by strong demand in Germany, the UK, and France. The decade ahead will be defined by subscription-model adoption, AI-driven dose optimization, and deeper penetration into tier-2 and tier-3 cities worldwide.

Key Report Takeaways

• By Product Type

- Non-invasive and minimally invasive devices captured roughly 62% of the Body Contouring Market in 2025, reflecting consumer preference for zero-downtime procedures.

- Invasive devices — including laser-assisted liposuction platforms — are forecast to grow at a 12.4% CAGR through 2035, sustained by demand for high-volume fat extraction in clinical settings.

• By Application

- Skin tightening and cellulite reduction accounted for approximately 45% of global Body Contouring Market revenue in 2025.

- Muscle toning and definition represent the fastest-growing application segment, projected at a 19.7% CAGR to 2035 as HIFEM platforms gain regulatory clearances in new geographies.

• By End User

- Hospitals retained roughly 69% of Body Contouring Market share in 2025 owing to procedural volume and reimbursement infrastructure.

- Medical spas are expanding at an 18.2% CAGR, driven by subscription pricing models and consumer convenience expectations.

• By Region

- North America led the Body Contouring Market with a 42% revenue share in 2025.

- Asia-Pacific is set to register the highest regional CAGR of 18.3% through 2035, powered by rising aesthetic awareness in China, South Korea, and India.

Market Size and Forecast (2021–2035)

Data for 2021–2024 draws on historical shipment records, provider revenue filings, and validated third-party databases. Forecast estimates (2026–2035) apply a compound-growth model calibrated to regional demand trajectories, regulatory pipeline analysis, and technology adoption curves published by Market Research Future.