Capacitor Market Summary

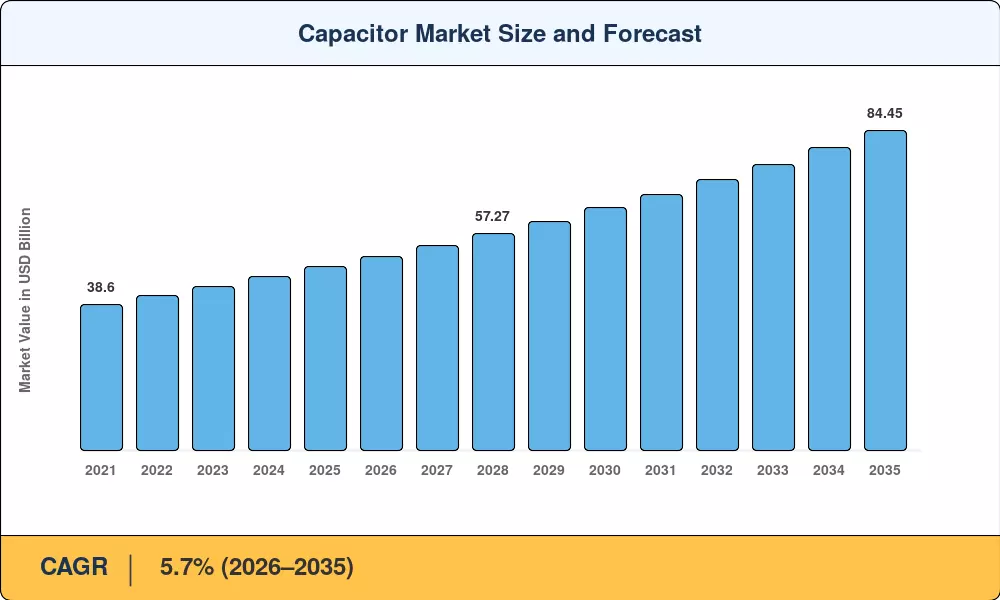

The global Capacitor Market reached an estimated USD 48.50 billion in 2025 and is projected to grow from USD 51.26 billion in 2026 to USD 84.45 billion by 2035, registering a CAGR of 5.7% during 2026–2035. This trajectory reflects two converging catalysts: the accelerating electrification of transportation — with global EV sales surpassing 17 million units in 2024 [1] — and the ongoing build-out of 5G telecommunications infrastructure that demands increasingly sophisticated passive components for signal integrity and power conditioning.

A generational shift is underway in capacitor technology. Legacy single-layer ceramic and basic aluminum electrolytic designs are yielding ground to advanced multilayer ceramic capacitors, high-capacitance polymer hybrids, and solid-state supercapacitors engineered for higher energy densities and tighter thermal envelopes. The U.S. Department of Energy's USD 3.5 billion Advanced Energy Manufacturing Tax Credit [2] and the EU's European Chips Act — directing EUR 43 billion toward semiconductor and component self-sufficiency [3] — are pulling investment into domestic capacitor fabrication lines across North America and Europe.

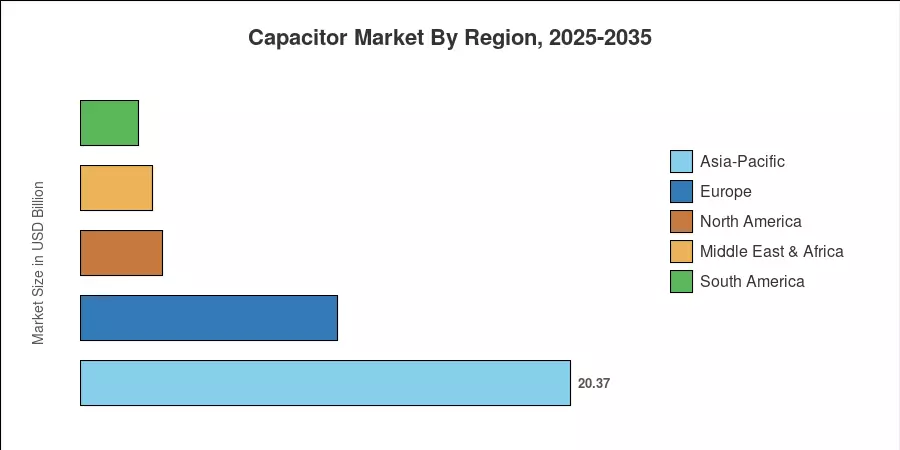

Asia-Pacific commands approximately 42% of the Capacitor Market, anchored by Japan, China, and South Korea's vertically integrated electronics supply chains. North America is the fastest-growing region, expanding at roughly 7.0% CAGR as reshoring incentives and defense procurement budgets swell. Europe holds the second-largest share at around 22%, driven by automotive OEM demand and renewable-grid investment. The decade ahead will reward manufacturers that can scale thin-film and high-voltage dielectric platforms while navigating tightening rare-earth material supply chains.

Key Report Takeaways

• By Type

- Ceramic capacitors account for approximately 45% of the Capacitor Market, supported by ubiquitous demand in smartphones, EVs, and base stations.

- Supercapacitors represent the fastest-growing type segment, expanding at a 9.4% CAGR through 2035 as energy-recovery and grid-storage applications scale.

- Film capacitors hold about 15% share, sustained by industrial motor drives and renewable inverter applications.

• By End-Use Industry

- Consumer electronics remains the largest end-use vertical, valued at roughly USD 15.52 billion in 2025.

- The automotive segment is expanding at the fastest pace among end-use categories, driven by EV power modules and ADAS circuitry.

• By Region

- Asia-Pacific dominates the Capacitor Market with a 42% value share in 2025, led by Japan and China.

- North America is the fastest-growing region at 7.0% CAGR, propelled by defense spending and chip-act-linked component reshoring.

Capacitor Market Size and Forecast (2021–2035)

Market size estimates draw on a triangulated methodology combining top-down industry production data from JEITA and ECIA trade associations, bottom-up revenue models built from leading manufacturer filings, and cross-validated import-export customs records for passive electronic components across 48 countries [4].