Casino Management System Market Summary

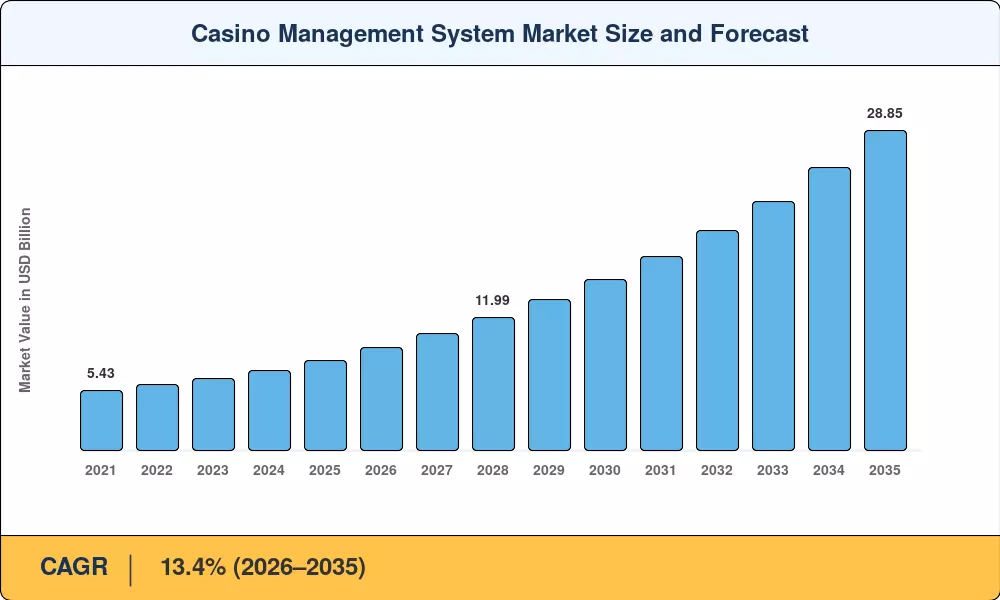

The Casino Management System Market stood at USD 8.10 billion in 2025 and is projected to reach USD 9.32 billion in 2026 before climbing to USD 28.85 billion by 2035, reflecting a 13.4% CAGR across the 2026–2035 forecast window. Mandatory cashless gaming directives rolling out across Nevada and several Australian jurisdictions, combined with sovereign data-residency requirements in the European Union, are forcing operators to replace fragmented legacy platforms with unified, compliance-ready architectures [1]. The strategic push for real-time patron intelligence and outcome-based vendor pricing is amplifying budget reallocation toward next-generation casino management system solutions.

Operators worldwide are retiring siloed slot-accounting terminals and standalone surveillance servers in favor of modular, API-first suites that converge floor analytics, loyalty management, cage operations, and cybersecurity monitoring on a single cloud-ready stack. The Asia-Pacific integrated-resort development pipeline — valued above USD 12 billion through 2030 — is a decisive catalyst, as greenfield properties increasingly specify end-to-end digital platforms at the design stage rather than retrofitting post-opening [2]. This structural shift turns the Casino Management System Market from a replacement cycle into a platform-economy buildout.

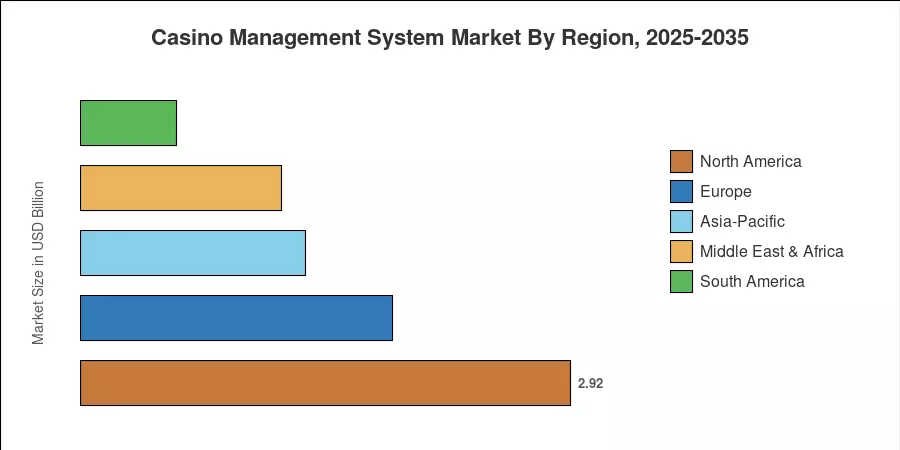

North America retained roughly 36% of the global Casino Management System Market revenue in 2025, anchored by tribal gaming expansion and state-level sports-betting legalization. Asia-Pacific is the fastest-growing region at an estimated 16.5% CAGR through 2035, driven by Macau concession renewals and Japan's emerging IR framework. Europe ranks as the second-largest region, with regulatory harmonization under the EU's Digital Services Act creating cross-border compliance demand. The decade ahead will reward vendors that balance hyperscale elasticity with tribal data sovereignty and multi-jurisdiction audit trails.

Key Report Takeaways

• By Component

- Services captured roughly 43% of the Casino Management System Market revenue in 2025, reflecting operators' growing reliance on managed implementation, training, and ongoing optimization contracts.

- The software segment is forecast to expand at a 12.8% CAGR through 2035 as modular licensing models replace legacy perpetual fees.

• By Deployment Mode

- Cloud-based deployments accounted for approximately 35% of the Casino Management System Market share in 2025, up from under 20% in 2021.

- On-premise solutions still dominate total revenue but are ceding ground as hybrid architectures gain regulatory acceptance.

• By Region

- North America generated an estimated USD 2.92 billion in Casino Management System Market revenue in 2025.

- Asia-Pacific is charting the fastest regional expansion, with a projected 16.5% CAGR through 2035.

- Europe held roughly 23% of the Casino Management System Market in 2025, supported by regulatory harmonization across member states.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates top-down macro indicators (gaming gross revenue, IT-spend ratios, regulatory filings) with bottom-up vendor-revenue tracking across 45 country markets. Historical figures draw on audited financial disclosures, while forecast values apply the calibrated 13.4% CAGR alongside segment-level acceleration and deceleration adjustments. All figures are denominated in USD Billion at constant 2025 exchange rates.

.webp?v=1782120130)