CCTV Market Summary

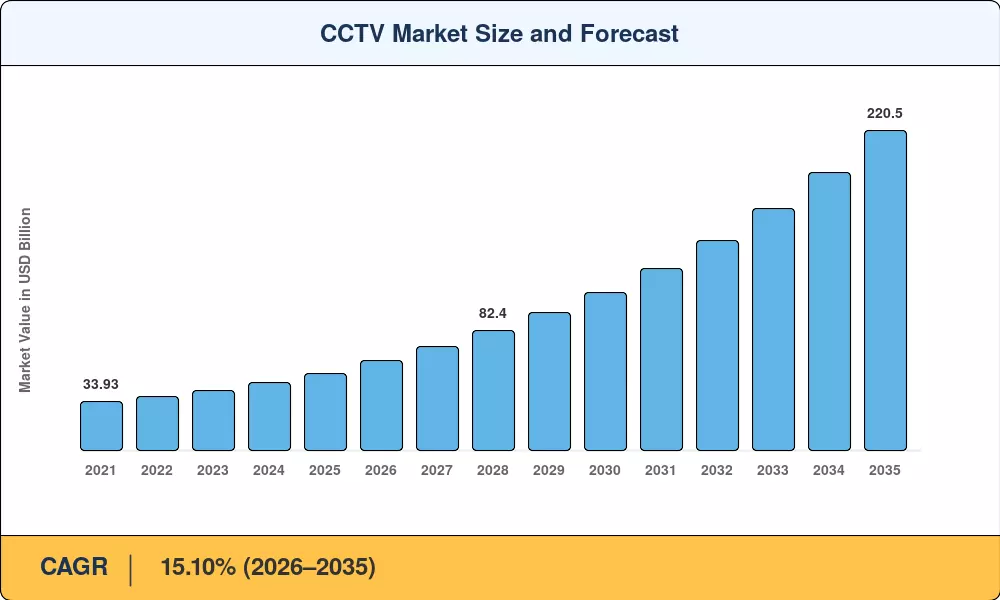

The global CCTV Market reached an estimated USD 53.35 Billion in 2025, positioning itself for a projected expansion from USD 62.20 Billion in 2026 to USD 220.50 Billion by 2035 at a CAGR of 15.10% during the forecast period. Two catalysts anchor this trajectory: smart-city mandates—India's Safe City Mission alone earmarked INR 2,700 Crore (~USD 325 million) across 15 cities [1]—and enterprise refresh cycles triggered by tightening data-protection regulations across the EU's AI Act and China's Personal Information Protection Law [2]. These policies are converting passive camera budgets into active surveillance-intelligence programs at a pace the industry has not seen in a decade.

Legacy analog CCTV systems, which still represent a declining but sizable installed base, are giving way to IP-based platforms equipped with on-camera inference chipsets and cloud-managed video subscriptions. The shift is not simply about higher resolution; it is about converting raw footage into structured metadata for traffic management, retail analytics, and workplace safety compliance. Global enterprise spending on intelligent video analytics surpassed USD 8.5 Billion in 2024, according to IHS Markit estimates, and continues to climb as edge-processing costs fall below USD 50 per camera [3].

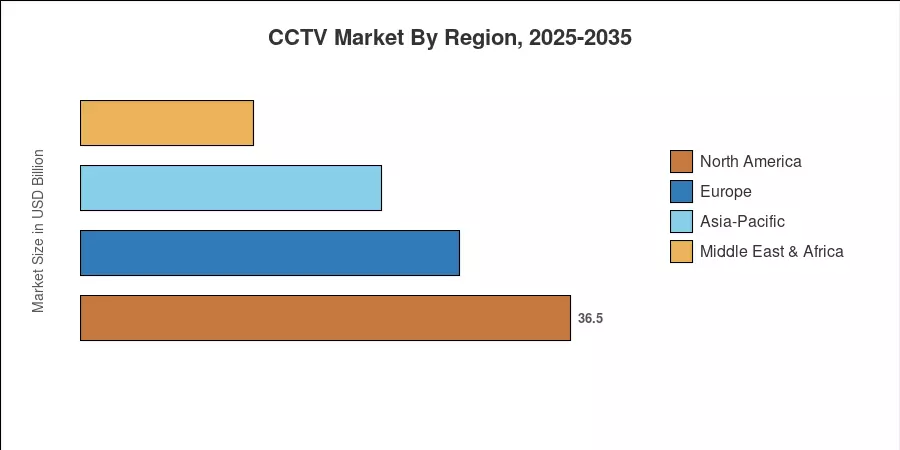

Asia-Pacific dominates the CCTV Market with a 37.1% revenue share in 2025, driven by government-led surveillance rollouts across China and India. The Middle East & Africa region is advancing at the fastest clip, registering a projected CAGR of 19.5% through 2035 as Gulf states invest in mega-project security and African nations digitize urban infrastructure. Europe holds the second-largest position, buoyed by GDPR-compliant upgrades and critical-infrastructure protection directives. As 5G coverage widens and bandwidth tariffs drop, the CCTV Market is poised to mature from a security cost center into a multi-purpose data asset.

Key Report Takeaways

• By Camera Type

- IP cameras captured 44.2% of the CCTV Market share in 2025, reflecting the accelerating migration from analog infrastructure.

- The 4K/Ultra-HD segment is forecast to grow at an 18.7% CAGR through 2035, driven by forensic-grade imaging requirements in government tenders.

• By End-User Vertical

- Government and public safety led the CCTV Market with a 30.8% revenue share in 2025, underscoring the weight of homeland-security budgets.

- Hospitality and healthcare verticals are expanding at a 16.1% CAGR, powered by patient-monitoring mandates and guest-experience analytics.

• By Region

- Asia-Pacific accounted for 37.1% of the global CCTV Market revenue in 2025.

- The Middle East & Africa is the fastest-growing region with a projected 19.5% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines bottom-up revenue aggregation from equipment and software vendors, validated against top-down macroeconomic indicators such as urban-security expenditure ratios and construction-permit data. Historical figures draw from company filings and customs-trade databases; forecast estimates apply segment-level CAGRs calibrated to policy timelines and technology adoption curves.

.webp?v=1785854587)