Centrifugal Blower Market Summary

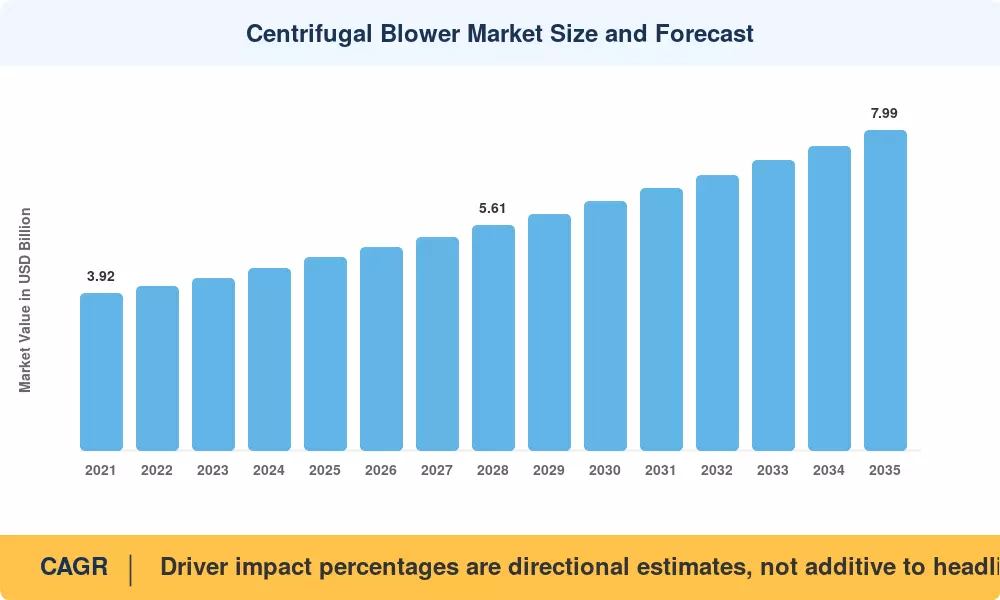

The global Centrifugal Blower Market reached an estimated USD 4.82 billion in 2025 and is projected to grow from USD 5.07 billion in 2026 to USD 7.99 billion by 2035, registering a CAGR of 5.2% during the forecast period (2026–2035). Two structural tailwinds anchor this trajectory: tightening industrial emissions mandates under the EU Industrial Emissions Directive recast and accelerating brownfield modernization across cement, steel, and power plants in developing Asia. Capital expenditure on air handling and gas conveyance infrastructure topped USD 11 billion globally in 2024, with centrifugal blower replacements capturing a growing share of that spending [1].

Legacy constant-speed blower installations — many dating to the 1990s — are giving way to digitally controlled, variable-speed systems that cut energy consumption by 20–35%. The U.S. Department of Energy's Industrial Decarbonization Roadmap targets a 30% reduction in industrial compressed-air and blower energy use by 2030, directly incentivizing upgrades [2]. European manufacturers are similarly aligning product portfolios around IE5 ultra-premium-efficiency motors, pushing lifecycle cost arguments over upfront price.

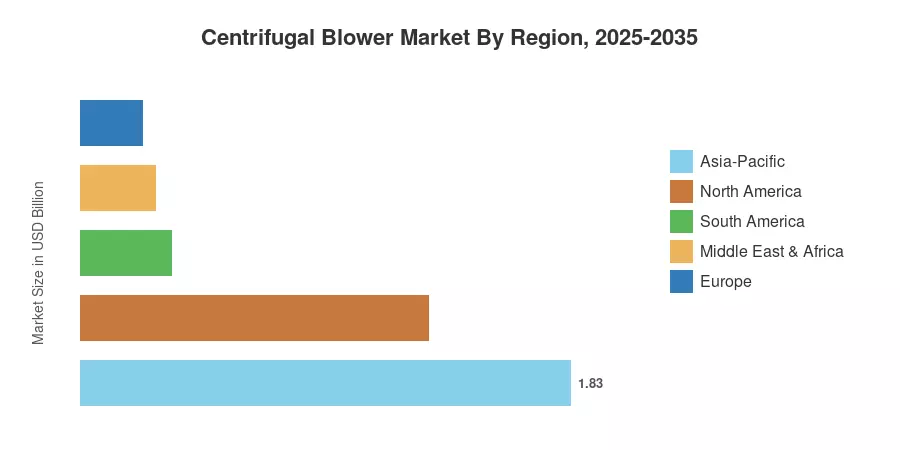

Asia-Pacific commands the largest regional share at approximately 38% of global revenue, driven by China's cement and wastewater treatment build-out. The region also leads growth with a forecast CAGR of 6.8%. North America holds roughly 27% share, buoyed by shale-gas processing and EPA emission compliance upgrades, while Europe accounts for about 22%, anchored by circular-economy retrofits. The Centrifugal Blower Market is poised for sustained expansion as decarbonization policies and industrial digitalization converge across every major end-use vertical.

Key Report Takeaways — Centrifugal Blower Market

By Type

- Backward curved blowers dominate the Centrifugal Blower Market with an estimated 34% revenue share, favored for high-efficiency HVAC and process-air applications.

- Radial blade designs register the fastest segment CAGR at 6.1%, driven by heavy-duty material handling in mining and cement.

- Airfoil blowers account for approximately USD 0.91 billion in 2025, serving clean-air applications across pharmaceutical and electronics manufacturing.

By End-Use Industry

- Power generation remains the top demand vertical in the Centrifugal Blower Market, contributing roughly 24% of global revenues.

- Water and wastewater treatment grows at approximately 6.4% CAGR through 2035, fueled by municipal infrastructure investment across India and Southeast Asia.

- Chemical and petrochemical plants represent USD 0.84 billion in 2025 blower consumption.

By Region

- Asia-Pacific leads the Centrifugal Blower Market at 38% share, with China alone accounting for over half of regional demand.

- North America delivers steady growth at 4.6% CAGR, supported by refinery modernization and data-center cooling.

- The Middle East & Africa region is the fastest-growing outside Asia-Pacific, at 5.9% CAGR, linked to desalination and petrochemical megaprojects.

Centrifugal Blower Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up revenue estimates from OEM shipment data, distributor channel audits across 22 countries, and top-down cross-validation against industrial motor and air-system market benchmarks. Historical figures (2021–2024) are reconciled with company annual filings; forecast values (2026–2035) apply a constant 5.2% CAGR calibrated against capital-expenditure pipelines from IEA and World Bank industrial datasets [3].