Certificate Authority Market Summary

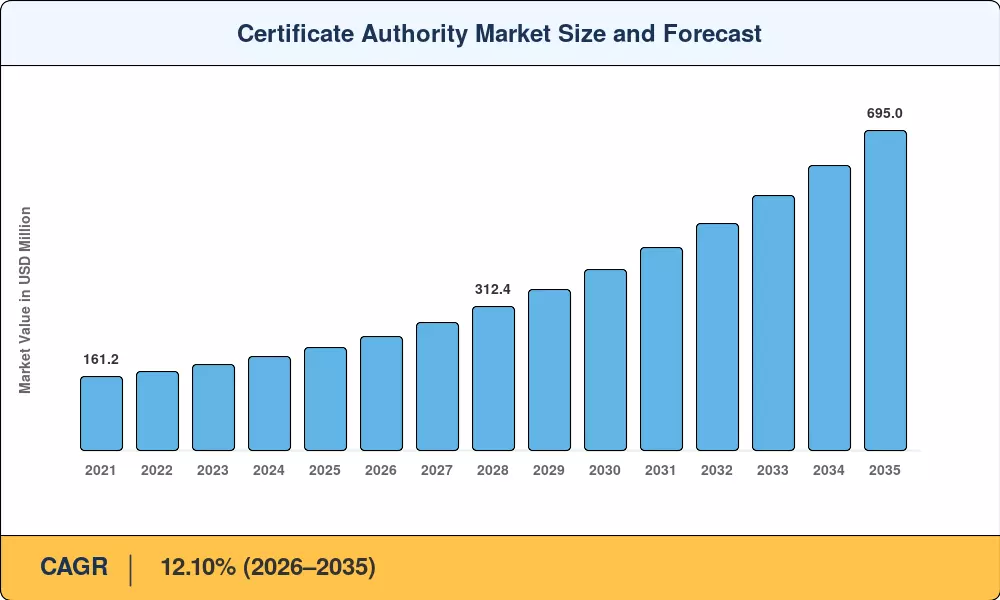

The certificate authority market was valued at USD 223.30 million in 2025 and is projected to reach USD 248.60 million by 2026, climbing to USD 695.00 million by 2035 at a compound annual growth rate of 12.10% during the forecast period (2026–2035). Two structural forces are accelerating demand: browser vendors — led by Apple and Google — have compressed maximum certificate validity to 90 days, triggering a wave of enterprise automation investment, while NIST's post-quantum cryptography standards (FIPS 203–205, finalized August 2024) are compelling organizations to run parallel hybrid key hierarchies [1]. These policy-driven mandates have turned certificate lifecycle management from a periodic IT task into a continuous, high-frequency operational requirement.

The technology shift underway is unmistakable. Legacy manual provisioning workflows that once handled a few hundred certificates per enterprise are giving way to API-first issuance platforms embedded directly inside CI/CD pipelines and infrastructure-as-code toolchains. Hyperscalers such as AWS, Google Cloud, and Microsoft Azure now offer native private certificate authority services that compress deployment from days to seconds. estimated that the average large enterprise manages over 300,000 machine identities, a figure growing 20% annually [2]. This explosion of non-human identities — containers, microservices, IoT endpoints — has made the certificate authority market a cornerstone of zero-trust architecture adoption.

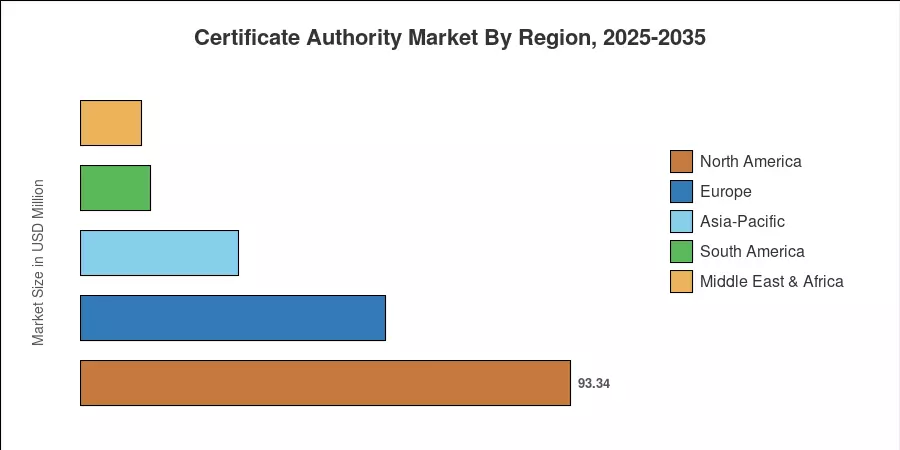

North America commanded a 41.8% share of the certificate authority market in 2025, supported by aggressive federal zero-trust mandates under Executive Order 14028 and the Cybersecurity and Infrastructure Security Agency's binding operational directives [3]. Asia-Pacific is registering the fastest regional CAGR at 13.5% through 2035, fueled by India's Digital Personal Data Protection Act and China's expanding Cybersecurity Law requirements. Europe holds the second-largest regional share at approximately 26.0%, driven by eIDAS 2.0 trust service provider regulations. The next decade will see the certificate authority market evolve from a trust infrastructure niche into a mission-critical automation layer spanning every connected endpoint.

Key Report Takeaways

• By Component

- Certificate types captured 51.6% of the certificate authority market share in 2025, reflecting enterprise demand for SSL/TLS, code-signing, and email-security certificates

- Services revenue is expanding at a 12.8% CAGR through 2035, driven by managed PKI and certificate lifecycle automation consulting

• By Organization Size & End-User Vertical

- Large enterprises accounted for 67.9% of the certificate authority market revenue in 2025, owing to complex multi-domain environments requiring centralized issuance

- BFSI led end-user verticals with a 31.2% share in 2025, as PCI-DSS 4.0 and open-banking API mandates require continuous certificate validation

- Healthcare and life sciences are forecast to grow at a 13.5% CAGR through 2035, propelled by HIPAA encryption mandates and connected medical device proliferation

• By Region

- North America maintained a 41.8% share of the certificate authority market in 2025

- Asia-Pacific is registering the fastest CAGR at 13.5%, with India and China driving digital infrastructure investments

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates supply-side revenues from publicly listed certificate authority vendors, demand-side enterprise IT security budgets, and third-party certificate transparency log volumes. Historical estimates (2021–2024) draw on audited company filings, while the forecast period (2026–2035) applies a calibrated growth model anchored to digital identity proliferation rates and regulatory enforcement timelines.

.webp?v=1782120130)