Chewing Gum Market Summary

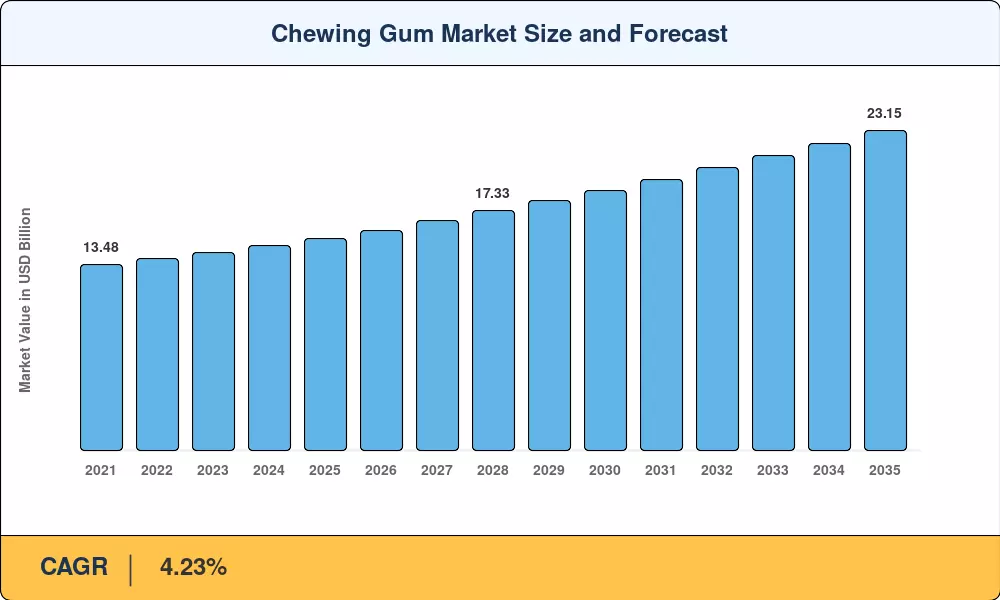

The global Chewing Gum Market stood at USD 15.35 billion in 2025 and is projected to reach USD 15.95 billion in 2026 before climbing to USD 23.15 billion by 2035, registering a CAGR of 4.23% across the forecast window. This trajectory reflects a consumer base that increasingly views gum not just as a confection but as a delivery vehicle for oral health benefits, energy boosts, and stress relief. Rising demand for sugar-free variants — now accounting for nearly two-thirds of global revenue — has reshaped product development priorities across the Chewing Gum Market, compelling manufacturers to reformulate around plant-derived sweeteners and functional additives [1].

The transformation underway in the Chewing Gum Market centers on moving beyond conventional chicle-based recipes toward synthetic and biodegradable gum bases that address both performance and environmental concerns. The European Commission's Single-Use Plastics Directive, which classifies traditional gum residue alongside plastic waste, has accelerated R&D investment estimated at over USD 320 million industry-wide between 2023 and 2025 [2]. Clean-label positioning and recyclable packaging formats are replacing legacy wrappers, while digital shelf analytics now guide assortment decisions at major retail chains.

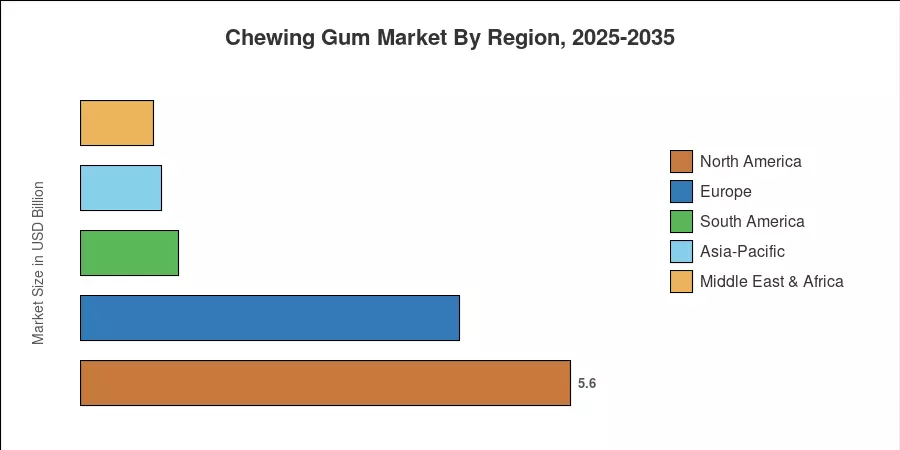

North America commands approximately 36.5% of the global Chewing Gum Market revenue, supported by entrenched per-capita consumption habits and robust convenience-store infrastructure. Asia-Pacific represents the fastest-growing region at a projected 6.02% CAGR through 2035, driven by urbanization, rising disposable incomes, and aggressive social-media marketing campaigns targeting younger demographics. Europe holds the second-largest share at roughly 28.2%, anchored by premiumization trends in Western markets. The decade ahead will reward companies that can balance health-forward innovation with the impulse-purchase dynamics that still drive the category.

Key Report Takeaways

• By Type

- The sugar-free segment captured approximately 63.5% of the Chewing Gum Market in 2025, reflecting a decisive consumer shift toward reduced-calorie and dental-friendly products.

- Sugar-based chewing gum is forecast to grow at a 3.18% CAGR through 2035, sustained by traditional confectionery demand in emerging economies.

• By Packaging

- Pouches led with a 53.2% revenue share in 2025 across the Chewing Gum Market, favored for portability and resealability.

- Bottles are projected to expand at a 5.48% CAGR, gaining traction in office and automotive consumption occasions.

• By Distribution Channel

- Supermarkets and hypermarkets held a 48.4% share of the Chewing Gum Market revenue in 2025.

- Online retail channels are anticipated to register a 6.32% CAGR between 2026 and 2035, fueled by subscription models and bundled oral-care offerings.

• By Region

- North America accounted for 36.5% of the global Chewing Gum Market value in 2025.

- Asia-Pacific is positioned to achieve a 6.02% CAGR through 2035, the highest among all regions.

Chewing Gum Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining top-down industry sizing from trade-association data, bottom-up company-level revenue analysis, and demand-side consumer-survey validation. Historical figures (2021–2024) reflect audited sales reported by leading confectionery producers, while forecast projections (2026–2035) incorporate macroeconomic inputs, regulatory scanning, and retail-channel growth modeling.