Xanthan Gum Market Summary

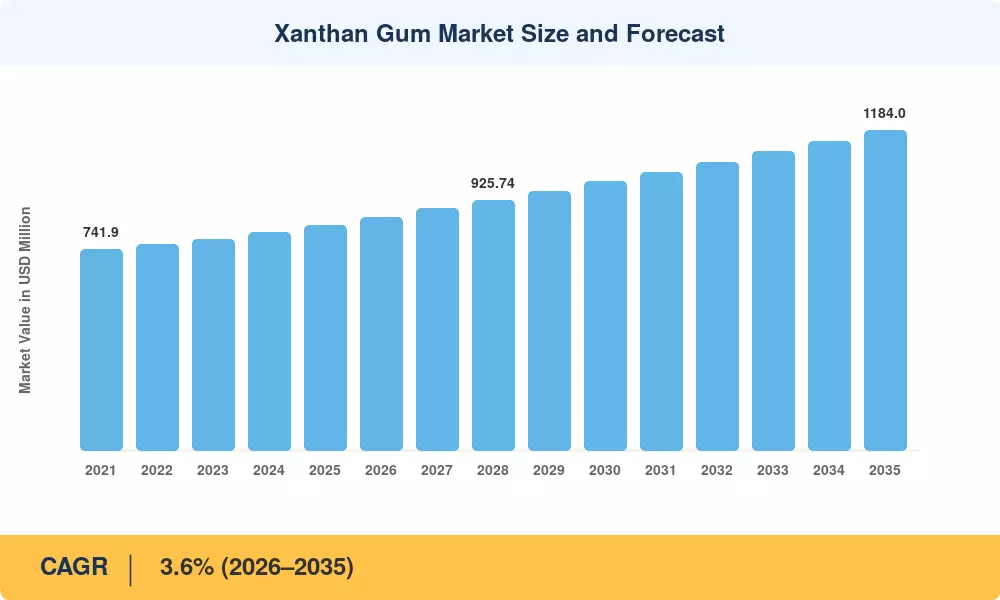

The global Xanthan Gum Market reached USD 832.50 Million in 2025 and is projected to expand from USD 862.50 Million in 2026 to USD 1,184.00 Million by 2035, registering a CAGR of 3.6% across the forecast period. Accelerating demand from clean-label food manufacturers and tightening oilfield chemical specifications are the two structural catalysts anchoring this trajectory. Regulatory pushes toward transparent ingredient labeling in the EU and North America have compelled food processors to replace synthetic stabilizers with naturally fermented alternatives, channeling fresh capital into xanthan gum production infrastructure [1].

The production landscape is undergoing a quiet but meaningful transformation. Legacy batch-fermentation facilities — many built in the 1990s — are giving way to continuous-fermentation platforms that cut cycle times by 30–40% and reduce wastewater discharge. China's Ministry of Industry and Information Technology allocated approximately USD 120 Million in upgrade subsidies for bio-based additive plants between 2023 and 2025, catalyzing capacity modernization across Shandong and Inner Mongolia provinces [2]. These investments are reshaping supply economics and tilting cost advantages further toward Asian producers.

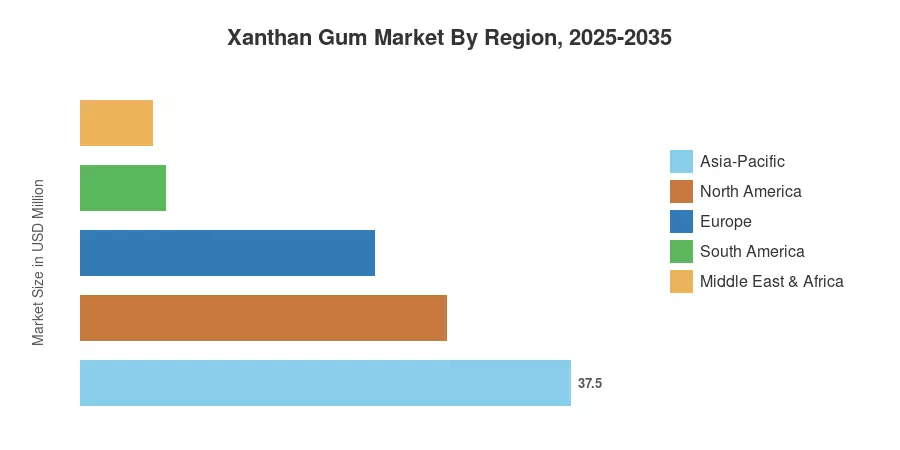

Asia-Pacific commands roughly 37.5% of global revenue, functioning as both the largest production hub and the fastest-growing consumption region at a projected 4.2% CAGR through 2035. North America holds the second position with 28.0% share, sustained by robust oilfield services demand and premium food-grade applications. Europe accounts for approximately 22.5%, driven by stringent additive regulations that favor high-purity grades. As plant-based food categories continue their double-digit expansion and shale drilling activity rebounds, the Xanthan Gum Market is positioned for steady compounding over the coming decade.

Key Report Takeaways

• By Form

- Dry xanthan gum represented approximately 80% of total Xanthan Gum Market revenue in 2025, reflecting its shelf stability and ease of transport across intercontinental supply chains.

- Liquid grades are forecast to register a 5.7% CAGR through 2035, gaining traction in ready-to-use cosmetic and pharmaceutical formulations.

• By Application

- Food and beverages accounted for a 44.5% share of the Xanthan Gum Market in 2025, led by sauces, dressings, and dairy-alternative categories.

- Oil and gas drilling fluids represent the second-largest application, expanding as operators in the Permian Basin and Middle Eastern fields specify xanthan-based muds for high-salinity formations.

• By Region

- Asia-Pacific held a 37.5% share of the Xanthan Gum Market, with China's fermentation clusters supplying over half of global production volume.

- North America is projected to grow at a 3.3% CAGR through 2035, buoyed by shale-sector recovery and premiumization of food-grade gum specifications.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on primary interviews with 45+ industry participants, customs-trade databases, corporate filings, and proprietary demand models validated against production-capacity audits across six countries.

.webp?v=1782993717)