Cloud Music Services Market Summary

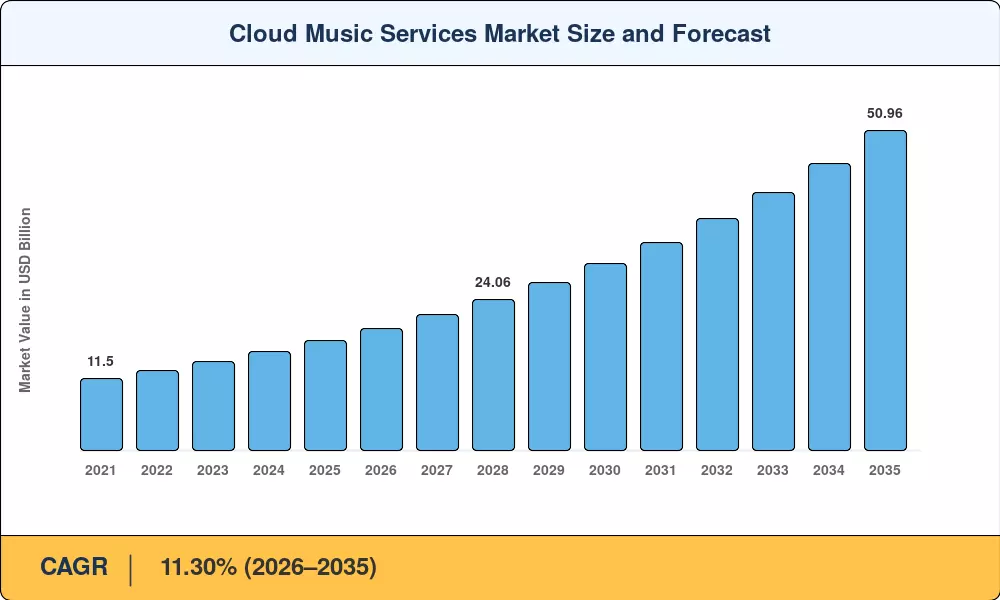

The cloud music services market was valued at USD 17.45 billion in 2025 and is projected to reach USD 19.42 billion in 2026 before climbing to USD 50.96 billion by 2035, registering a CAGR of 11.30% during the 2026–2035 forecast period. Two catalysts anchor this trajectory: the relentless global expansion of 4G/5G mobile subscriptions—which surpassed 5.5 billion connections in 2024 [1]—and platform investments exceeding USD 2 billion annually in AI-powered recommendation algorithms that extend average listening sessions beyond 80 minutes per day [2]. These forces compress churn rates and push free-tier listeners toward paid subscriptions at a pace legacy download-and-own models never achieved.

A generational shift from ownership to access underpins the transformation reshaping the cloud music services market. Physical media and permanent digital downloads have given way to on-demand libraries hosting over 100 million tracks apiece, delivered through globally distributed cloud networks. Operators are pouring capital into lossless and spatial audio codecs—Apple alone committed over USD 500 million to Dolby Atmos Music integration across its ecosystem in 2023–2024 [3]. Parallel regulatory activity, including the EU Copyright Directive and the U.S. Music Modernization Act, is standardizing rights-holder payment structures and increasing catalog transparency [4].

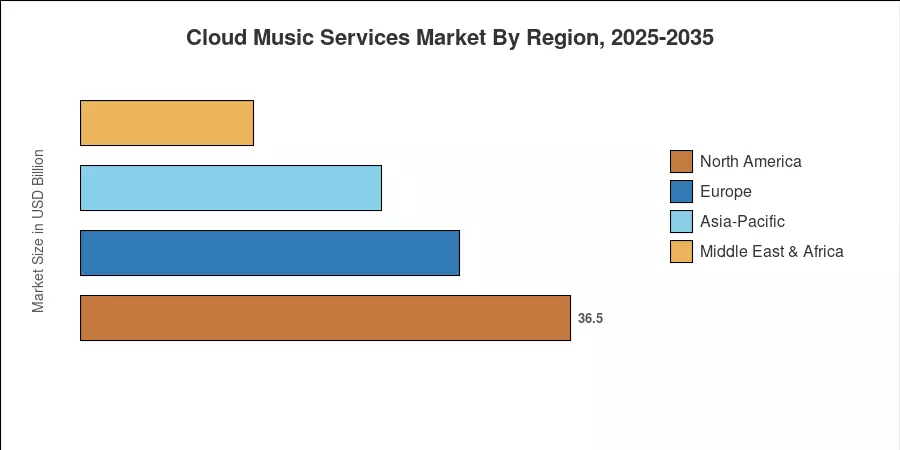

North America leads the cloud music services market with roughly 45.0% of global revenue, powered by mature subscription penetration and a robust advertising ecosystem. Asia-Pacific stands as the fastest-growing region at an estimated 12.44% CAGR through 2035, propelled by smartphone-first populations in India and Southeast Asia. Europe holds the second-largest share, supported by telco-bundled offerings and harmonized digital copyright rules. As 5G rollouts deepen and connected vehicle dashboards multiply, the next decade will see cloud-delivered audio embed itself into virtually every screen and speaker.

Key Report Takeaways

• By Service Type

- On-demand streaming captured approximately 77% of the cloud music services market revenue in 2025, driven by catalog depth and personalization algorithms.

- Live streaming is forecast to grow at a 14.00% CAGR through 2035, fueled by virtual concert monetization and real-time fan interaction.

• By Revenue Model

- Subscription-based tiers accounted for roughly 73% of total revenue in 2025, reflecting premium tier adoption and family-plan expansion.

• By Platform

- Automotive infotainment platforms are projected to post a 15.60% CAGR, the fastest across all platform types, as connected-car shipments accelerate.

• By Region

- North America maintained a dominant 45.0% share of the cloud music services market in 2025.

- The Asia-Pacific region is anticipated to expand at a 12.44% CAGR through 2035, led by India, China, and ASEAN economies.

Market Size and Forecast (2021–2035)

Market Research Future derives its estimates from a triangulated methodology combining top-down revenue analysis of publicly listed platform operators, bottom-line subscriber-count modeling validated against IFPI and RIAA databases, and regional demand signals from telecom partnership disclosures [1][5].