Cocoa Beans Market Summary

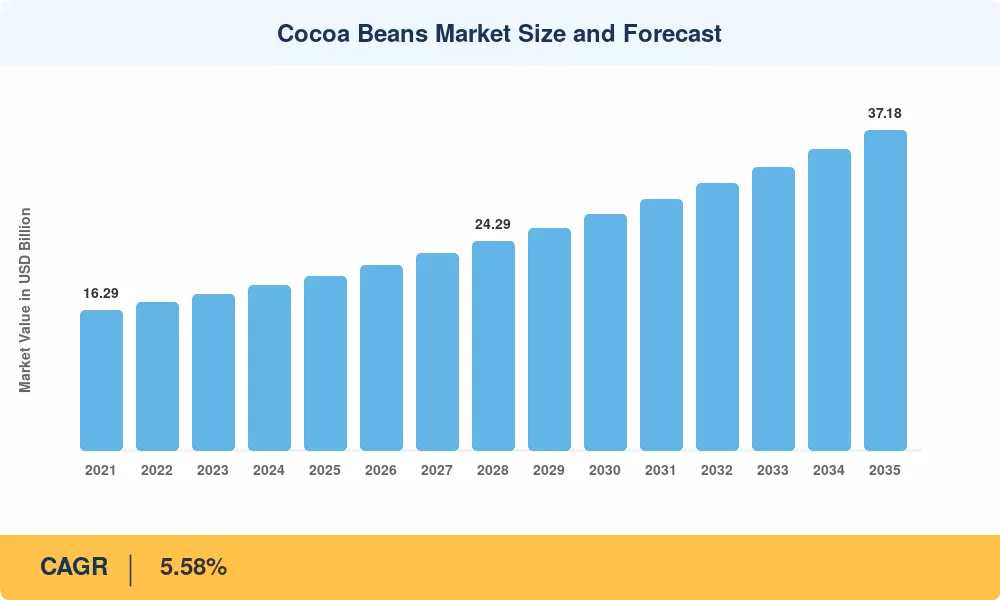

The global Cocoa Beans Market reached an estimated USD 20.24 billion in 2025 and is projected to expand from USD 21.38 billion in 2026 to USD 37.18 billion by 2035, registering a CAGR of 5.58% across the forecast window. Two catalysts are accelerating this trajectory: the European Union Deforestation Regulation (EUDR), which compels importers to prove zero-deforestation sourcing by late 2025, and a USD 1.3 billion coordinated investment program by West Africa cocoa production boards aimed at rehabilitating aging tree stock across Côte d'Ivoire and Ghana [2][3]. Together, these forces are reshaping cocoa supply chain sustainability practices and pulling capital into origin-country processing infrastructure.

There is a change in technology taking place across the cocoa value chain. Age-old sun-drying and manual fermentation procedures long established in West Africa’s cocoa-producing regions are being replaced by solar-powered fermentation chambers, satellite-monitored crop health platforms and blockchain-backed traceability ledgers. Cargill alone pledged more than USD 130 million from 2024-2025 to install 500 solar fermentation units in Indonesia, reducing post-harvest losses by about 15% and increasing the uniformity of cocoa bean origin flavor at the farm gate [4]. Consumer demand for ethically sourced products continues to grow, with an estimated 22% of the global traded volume already certified under fair trade cocoa programs (16% in 2021) [5].

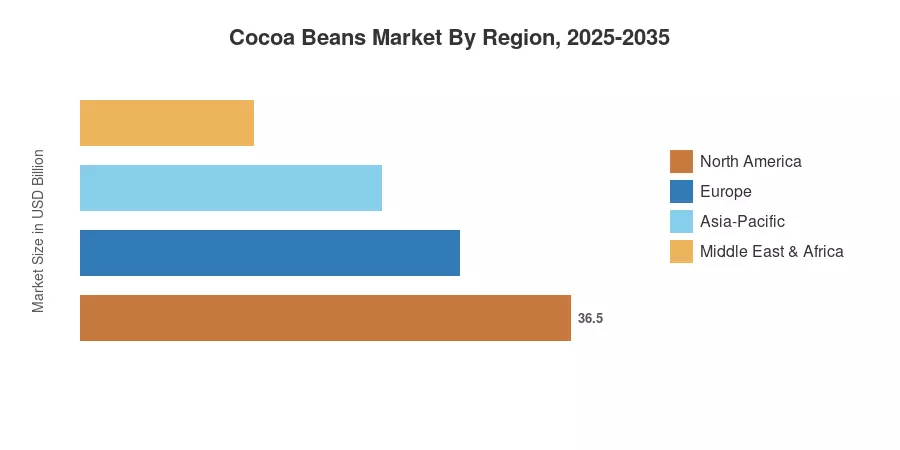

The European Cocoa Beans Market accounts for around 35% of the world’s Cocoa Beans Market value, with the Netherlands and Germany as major grinding hubs and a legacy of quality chocolate production. Asia-Pacific is the fastest growing area and is expected to develop at a CAGR of 5.30% through 2035, as consumption of confectionary products is seeing a significant surge in China, India and ASEAN countries. The second largest region is North America with a share of about 24%. The region is driven by artisan chocolate innovation and commodity hedging of cocoa bean prices by industrial customers The next decade will pay off for enterprises that combine sustainability in the cocoa supply chain, with processing at origin and digital traceability.

Key Report Takeaways

• By Product Type

- Conventional cocoa beans account for roughly 72% of the Cocoa Beans Market by value in 2025, reflecting bulk confectionery and industrial demand

- Organic and specialty-grade beans are projected to grow at a 7.10% CAGR through 2035, outpacing the overall market as fair trade cocoa certification expands retail shelf space

• By Application

- Chocolate confectionery remains the dominant application, valued at approximately USD 12.8 billion in 2025, driven by premiumization and single-origin branding

- Cocoa butter and powder for cosmetics and pharmaceuticals are expanding at a 6.25% CAGR, fueled by clean-label ingredient trends

• By Region

- Europe held a 35% share of the Cocoa Beans Market in 2025, supported by EUDR compliance investment and deep grinding infrastructure

- Asia-Pacific is set to expand at a 5.30% CAGR to 2035 as cocoa bean origin flavor awareness grows among Asian consumers

- The Cocoa Beans Market in North America is valued at approximately USD 4.86 billion, underpinned by craft chocolate and institutional procurement

Cocoa Beans Market Size and Forecast (2021–2035)

MRFR's estimates combine bottom-up trade flow data (ICCO, FAO), import/export customs records, processor capacity filings, and proprietary demand modeling. Historical values (2021–2024) are triangulated against published grinding statistics, while forecast projections apply a calibrated compound growth rate adjusted for supply disruptions and regulatory phase-in timelines.